Published by Josh Arnold on November 7th, 2022

In the world of investing, the goal is always to compound wealth as efficiently as possible. We think the best way to do that is to buy high-quality dividend stocks, reinvest the dividends, and stay the course over a number of years. However, investors can also infuse their own personal preferences or beliefs into their investing strategy, and still make great returns.

One theme that has captured more of the conscience of investors in recent years is the idea of environmental friendliness. There are many ways for a company to be considered environmentally friendly, with renewable energy and recycling being obvious choices.

Investors can buy high-quality dividend growth stocks such as the Dividend Aristocrats individually, or through exchange-traded funds. ETFs have become much more popular in the past five years, especially when compared to more expensive mutual funds.

With this in mind, we created a downloadable Excel list of dividend ETFs that we believe are the most attractive for income investors. We have also included the dividend yield, expense ratio, and average price-to-earnings ratio of the ETF (if available).

You can download your full list of 20+ dividend-focused ETFs by clicking on the link below:

In this article, we’ll take a look a 10 renewable energy and recycling stocks, all of which pay dividends to shareholders. We rank them below by total expected returns in the coming years for those investors that want to hold companies that have a hand in preserving the environment.

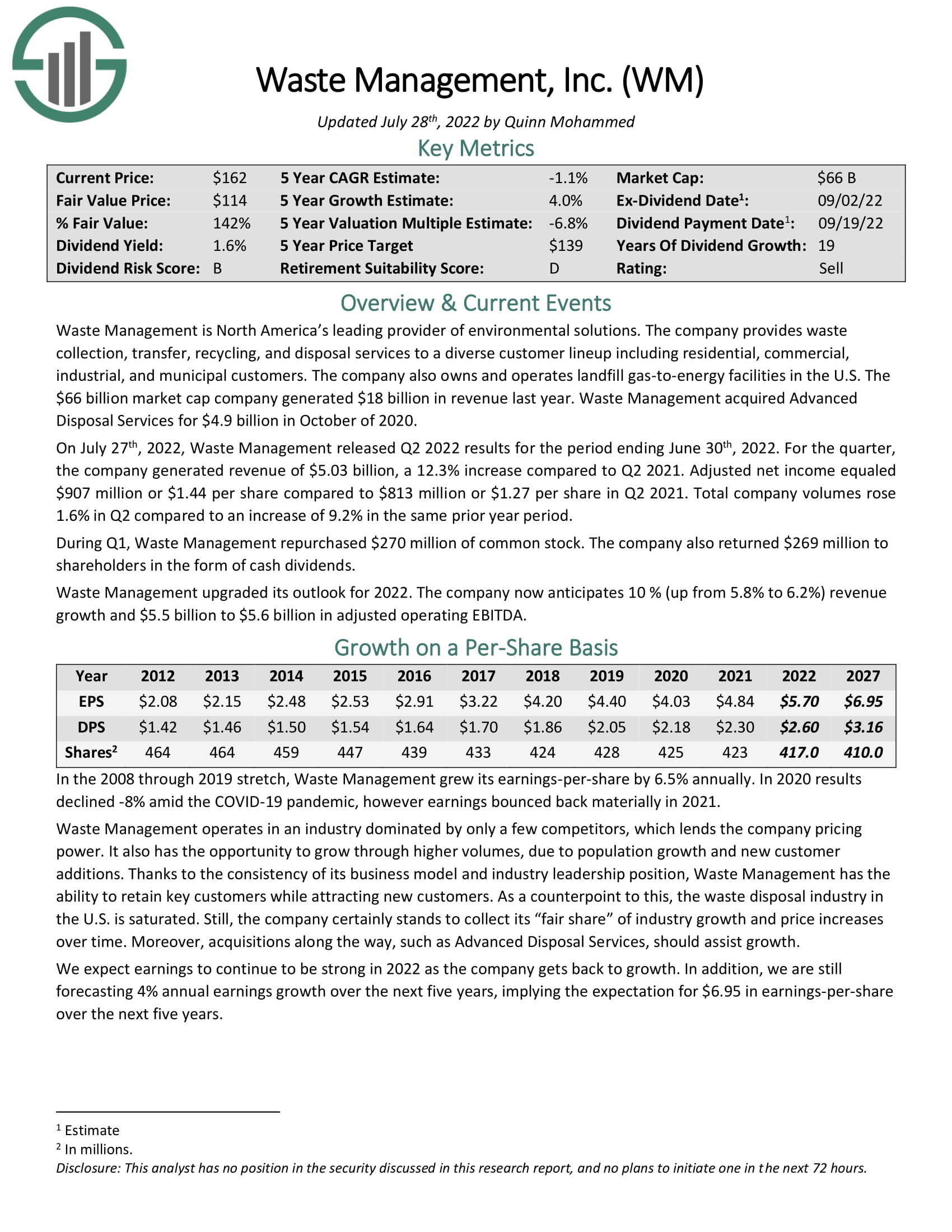

Waste Management (WM)

Our first stock is Waste Management, a company that provides waste management environmental services to residential, commercial, industrial, and municipal customers, mainly in the U.S. The company offers collection and transporting of waste and recyclable materials, owns landfill gas-to-energy facilities, and operates transfer stations.

The company was founded in 1987, employs 48,500 people, produces almost $20 billion in annual revenue, and trades with a market cap of $64 billion.

Waste Management made the list because it is a huge player when it comes to recycling. The company is the largest waste collection and recycling firm in the U.S., so it has unmatched scale. It also focuses on making more efficient use of the recyclables it collects, in addition to its landfill gas-to-energy efforts, which strive to turn otherwise wasted gas into usable energy.

The company’s dividend streak stands at 19 consecutive years of increases, but unfortunately the yield is fairly low at 1.7%. That’s about where the S&P 500 yields today, however, so it’s right at the market average.

Waste Management is first on our list because it has the lowest expected total returns. The stock is trading well in excess of fair value, meaning we see -0.2% total returns moving forward. That would consist of the 1.7% yield, 4% projected earnings-per-share growth, and a 6% headwind from the valuation.

Click here to download our most recent Sure Analysis report on Waste Management (preview of page 1 of 3 shown below):

{kind=link}

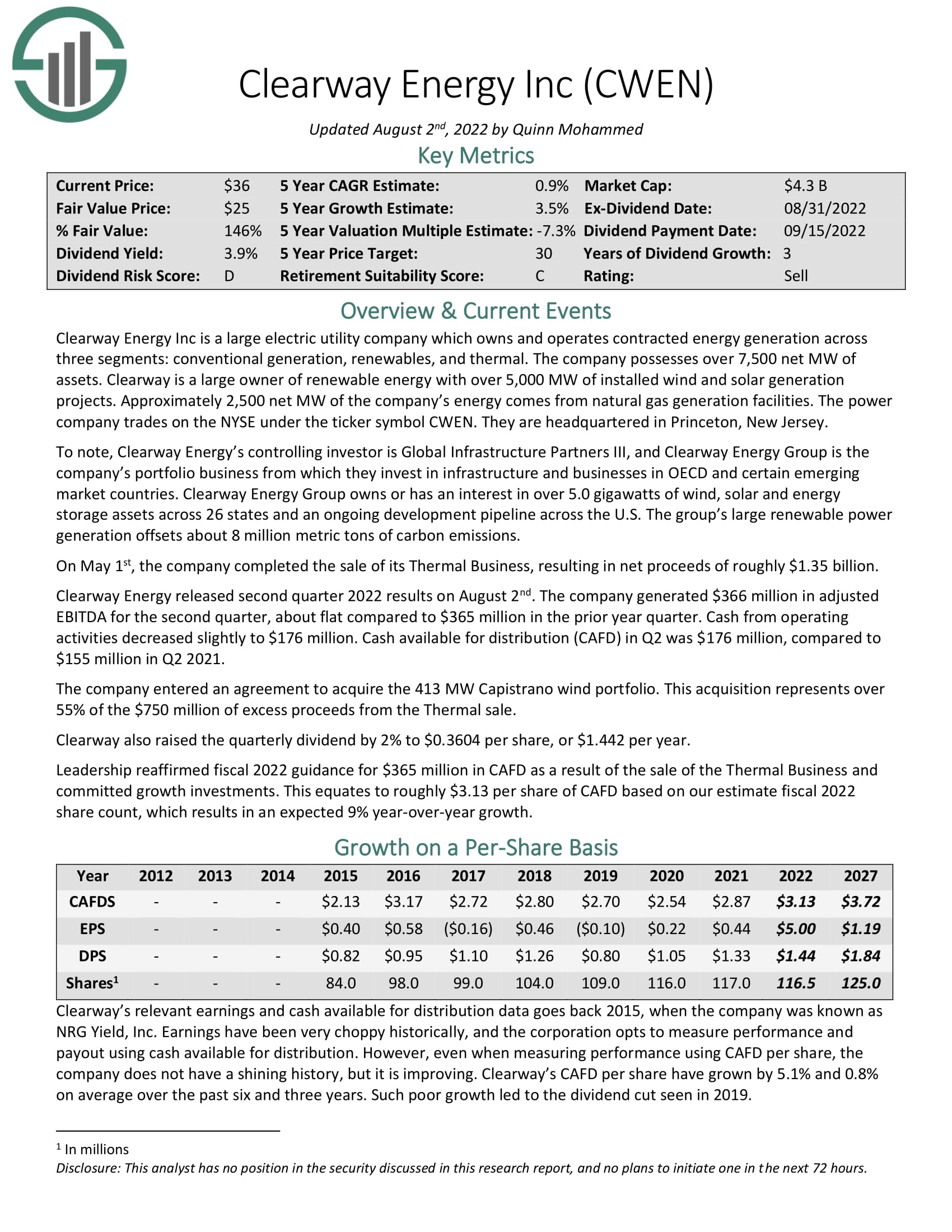

Clearway Energy Inc. (CWEN)

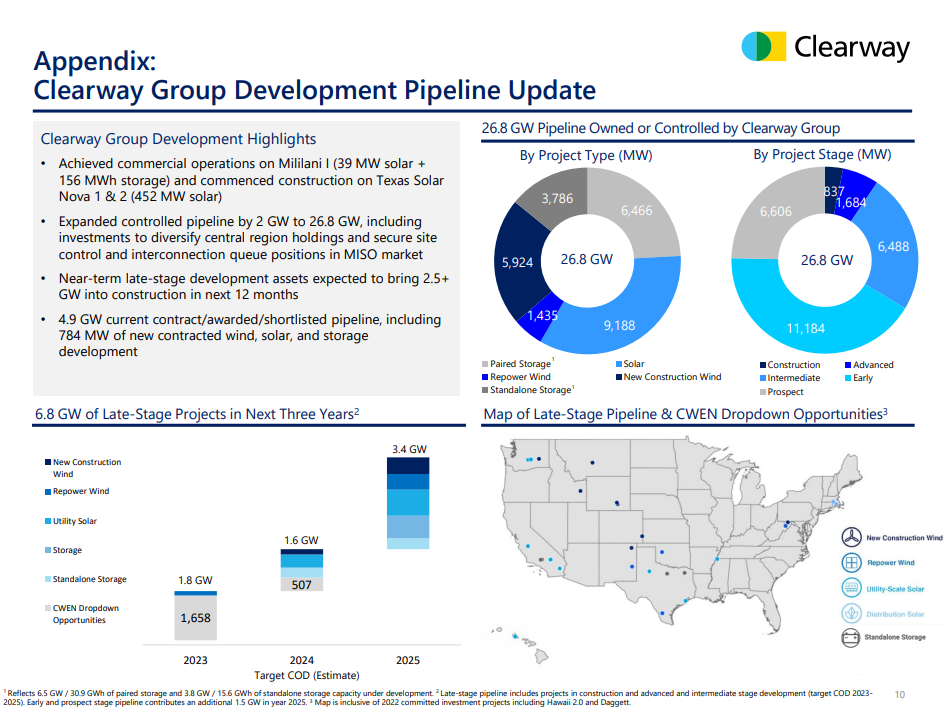

Our next stock is Clearway Energy, which is a renewable energy business based in the U.S. The company has about 5,000 net megawatts, or MW, of installed wind and solar generation projects. In addition, it has 2,500 net MW of natural gas generation facilities. The company was founded in 2012, employs only 300 people, produces about $1.2 billion in annual revenue, and trades with a market cap of $6.7 billion.

Clearway has a very obvious tie-in to the environment as it owns a huge installed base of wind and solar projects that are generating electricity today. In addition to that, the company has a massive amount of incremental power coming online in the next three years.

{kind=link}

Source: Investor presentation

The company is ramping its growth trajectory into 2025, and is diversifying into several different types of renewable power generation and storage.

The dividend streak stands at just three years, but the yield is outstanding at 4.2%. That makes Clearway a terrific income stock, given that’s almost triple the yield of the S&P 500.

Total expected returns are low at 1.8%, despite the 4.2% yield, because forecast growth of 3.5% is more than offset by a 6.5% projected headwind from the valuation, as shares are well ahead of fair value today.

Click here to download our most recent Sure Analysis report on Clearway Energy Inc. (preview of page 1 of 3 shown below):

{kind=link}

Ormat Technologies Inc. (ORA)

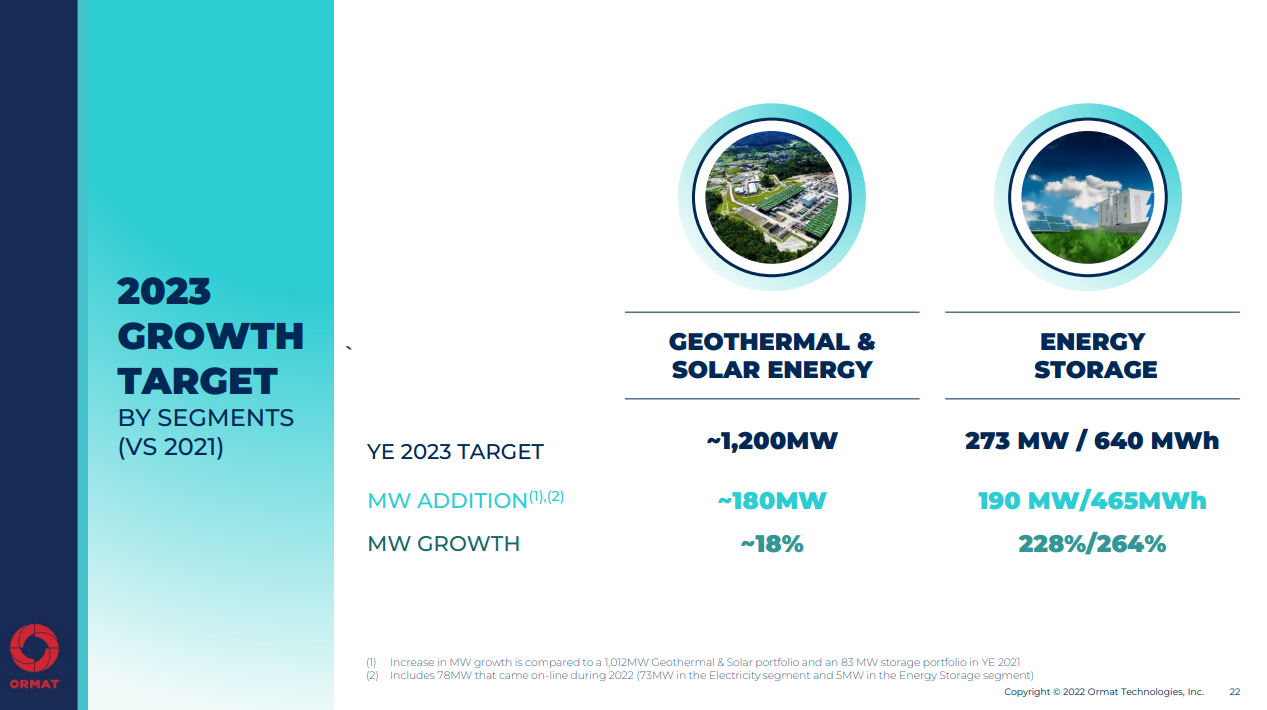

Next up is Ormat Technologies, a company that generates power, as well as selling equipment to others looking to generate renewable power. It operates in the U.S., Indonesia, Kenya, Turkey, Chile, Central America, Ethiopia, New Zealand, and Honduras. Through its segments, Ormat, develops, builds and owns geothermal, solar, and recovered energy facilities and sells its electricity. In addition to selling equipment, the company also operates an energy storage business.

Ormat was founded in 1965, produces about $725 million in annual revenue, and trades with a market cap of $5 billion.

Ormat’s dividend increase streak stands at seven years today, but given very strong recent price action in the stock, the yield is just 0.5%. That makes Ormat unattractive from a pure yield perspective, but we see robust growth potential on the horizon for both the stock and the dividend.

{kind=link}

Source: Investor presentation

The company plans to boost its geothermal and solar energy production by about 18% between 2021 and 2023, while its energy storage business is set to more than triple.

To that end, we expect to see 15% earnings growth but that will be mostly offset by a 10.1% headwind from a contracting valuation. When adding back in the 0.5% yield, we expect 3.9% total returns in the years ahead.

LKQ Corporation (LKQ)

Our next stock is LKQ Corporation, a company that distributes replacement parts, components and systems used in the repair and maintenance of vehicles. LKQ operates in North America and Europe. The company distributes a wide variety of replacement parts, but its tie-in to sustainability and environmental friendliness is its recycling business. The company provides sheet metal and scrap metals to metal recyclers, keeping those products out of landfills and saving the raw material that would otherwise have to be mined and turned into new products.

LKQ was founded in 1998, generates just under $13 billion in annual revenue, and trades with a market cap of $14 billion.

The company’s dividend streak is just one year, as it only began returning cash to shareholders in 2021. However, it has a respectable 1.9% yield today, which is better than the S&P 500.

In addition to that 1.9% yield, we see 5% earnings growth, and a 0.5% headwind from the valuation, as we believe the stock is just slightly over fair value today. That means investors could see 6.2% annual returns for LKQ in the years ahead.

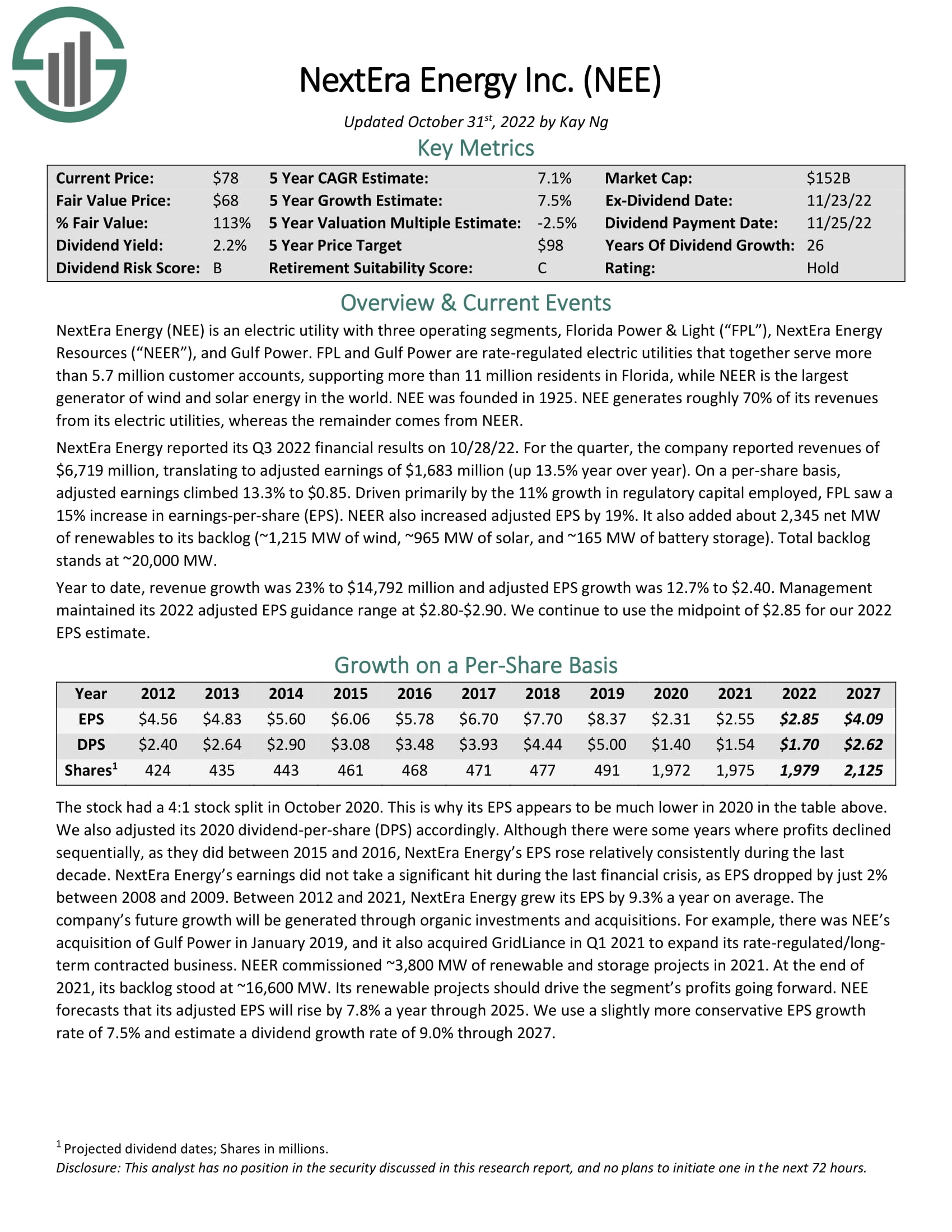

NextEra Energy Inc. (NEE)

Our next stock is NextEra Energy, which is a massive electric utility based in Florida. The company generates, transmits, and sells electric power to retail and wholesale customers in the U.S. Its tie to environmental friendliness is its renewables business, which includes a portfolio of solar and wind electricity facilities. The company also operates coal, nuclear, and natural gas facilities, but is making a push for more renewable energy in the years to come.

NextEra was founded in 1925, generates $21.5 billion in annual revenue, and trades with a market cap of $152 billion.

NextEra’s push to get away from nuclear, coal, and natural gas facilities will take many years, but investors interested in renewable energy will find a willing partner in NextEra.

The company also has an impressive streak of 26 consecutive years of dividend increases, and its current yield is meaningfully ahead of the broader market at 2.2%.

We see 7.1% total expected returns in the years to come, driven by the 2.2% yield, 7.5% projected growth, and a 2.5% headwind from a slightly contracting valuation.

Click here to download our most recent Sure Analysis report on NextEra Energy Inc. (preview of page 1 of 3 shown below):

{kind=link}

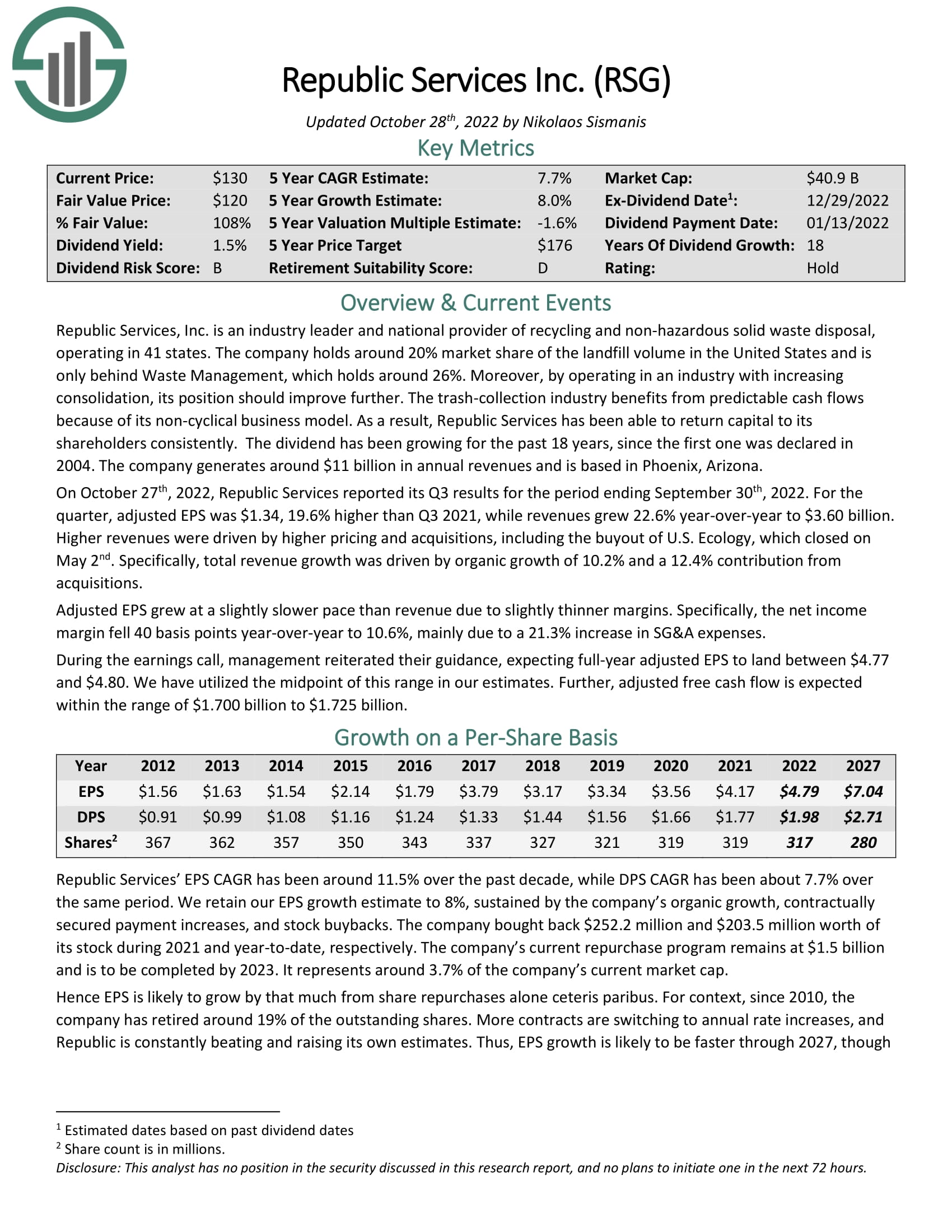

Republic Services Inc. (RSG)

Republic Services is our next stock, a company that offers waste collection and recycling through a sizable network of collection stations and landfills in the U.S. Like Waste Management, Republic Services has a large recycling business, as well as landfill-to-gas energy collection facilities in the U.S.

Republic was founded in 1996, produces about $13.5 billion in annual revenue, and trades with a market cap of $41 billion.

{kind=link}

Source: Investor presentation

Republic has a big focus on sustainability, which is why it ended up in this list. The company has distinct climate goals around recovery of energy, and powering its fleet of trucks in cleaner ways, as examples.

Republic’s dividend increase streak stands at 18 years, but its yield is below-market at 1.5%.

Still, given the yield, robust 8% projected growth, and a 1.6% headwind from the valuation that is slightly over fair value, we see respectable 7.6% annual returns in the years ahead.

Click here to download our most recent Sure Analysis report on Republic Services Inc. (preview of page 1 of 3 shown below):

{kind=link}

Aris Water Solutions Inc. (ARIS)

Our next stock is Aris Water Solutions, an environmental infrastructure and solutions company. Aris provides water handling and recycling solution to customers in the U.S. This includes gathering, transporting, and recycling water from oil and natural gas production facilities. The company helps make the production of energy – and the water it uses – more environmentally friendly by avoiding simply wasting that water.

The company was founded in 2015, and in a short time has grown to $320 million in annual revenue, and a market cap of $930 million.

Aris only began paying dividends to shareholders in early-2022, but it already raised the payout from the initial dividend of seven cents per share. That means its current yield is 2.1%, well ahead of the S&P 500’s average yield today.

With that yield in mind, as well as outstanding 15% annual growth prospects, but an offsetting 7.8% headwind from what we see as overvaluation of the stock, we forecast 7.8% total annual returns in the years to come.

Waste Connections Inc. (WCN)

Waste Connections is a waste collection, transfer, disposal, and resource recovery business in the U.S. and Canada. It offers various recycling services, including solid waste, as well as fluids used in the oil and gas drilling industry, helping to increase the sustainability of those sectors.

The company was founded in 1997 and is based in Canada, with $7.2 billion in annual revenue, and a market cap of $33 billion.

{kind=link}

Source: Investor presentation, September 2022

As we can see, Waste Connections has robust ESG targets for the long-term, as it is looking to increase its own sustainability, as well as those of its customers.

Waste Connections has boosted its dividend for six consecutive years, but the strong performance of the stock means the yield is very low at just 0.7%. However, we see strong dividend growth prospects for the stock in the years to come.

We expect 8.1% total annual returns, accruing from the 0.7% yield, 12% projected growth, and a 4.1% headwind from the valuation.

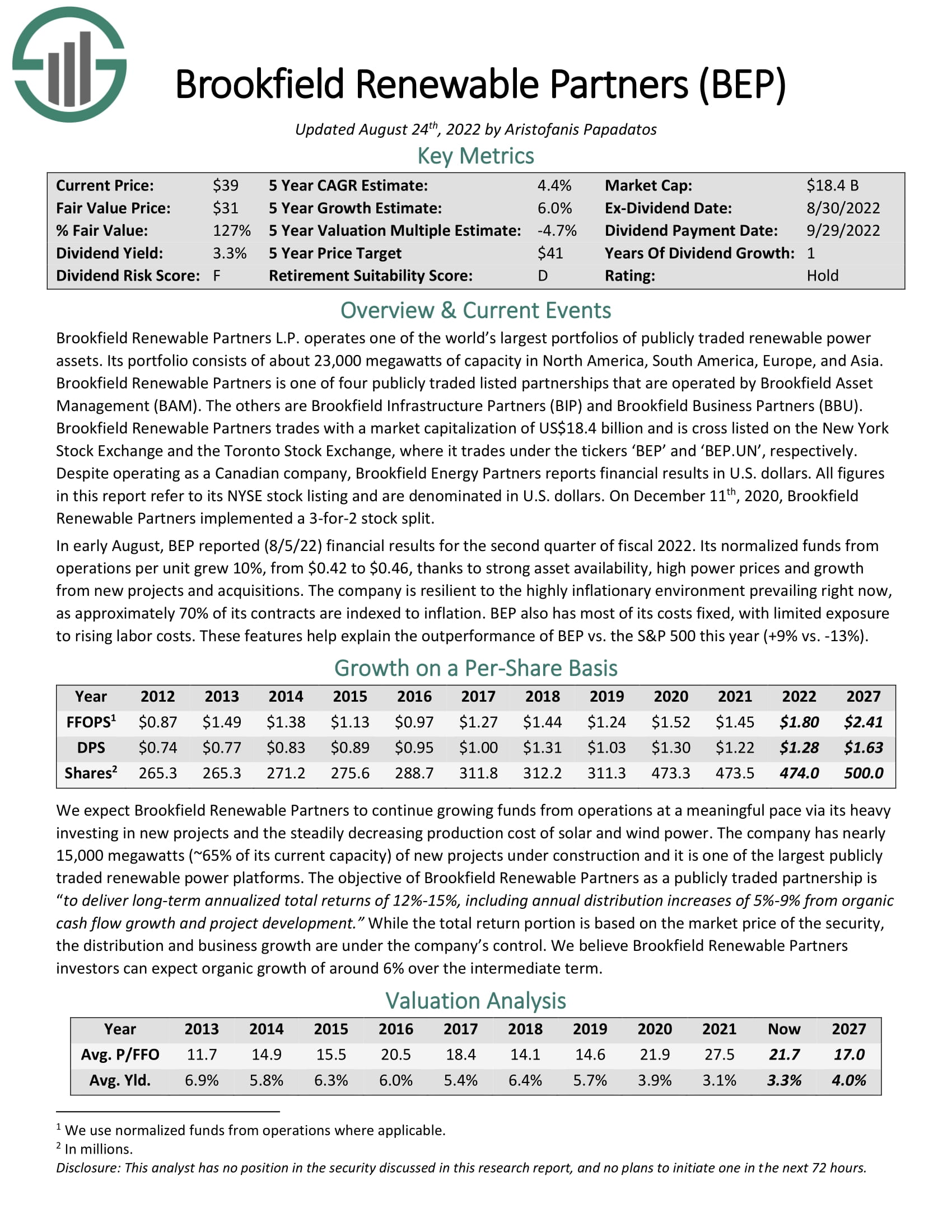

Brookfield Renewable Partners L.P. (BEP)

Our penultimate stock is Brookfield Renewable Partners, a partnership which owns a portfolio of renewable power generating facilities in North America, Colombia, Brazil, China, India, and parts of Europe. It generates electricity through hydroelectric, wind, solar, and biomass sources, so it is a pure renewable energy and sustainability stock. The partnership is one of several operated by Brookfield Asset Management (BAM).

Brookfield was founded in 1999, produces $4.6 billion in annual revenue, and trades with a market cap of $13.8 billion.

Brookfield pays a variable dividend, so its current increase streak is just one year. However, the yield is outstanding at 4.4%. The partnership pays out about two-thirds of its earnings as dividends to shareholders, so we believe future dividend growth will roughly match that of earnings.

When we combine that with 6% expected growth, and a 1.2% tailwind from the valuation, we believe the stock can produce 10.9% total returns in the years ahead.

Click here to download our most recent Sure Analysis report on Brookfield Renewable Partners L.P. (preview of page 1 of 3 shown below):

{kind=link}

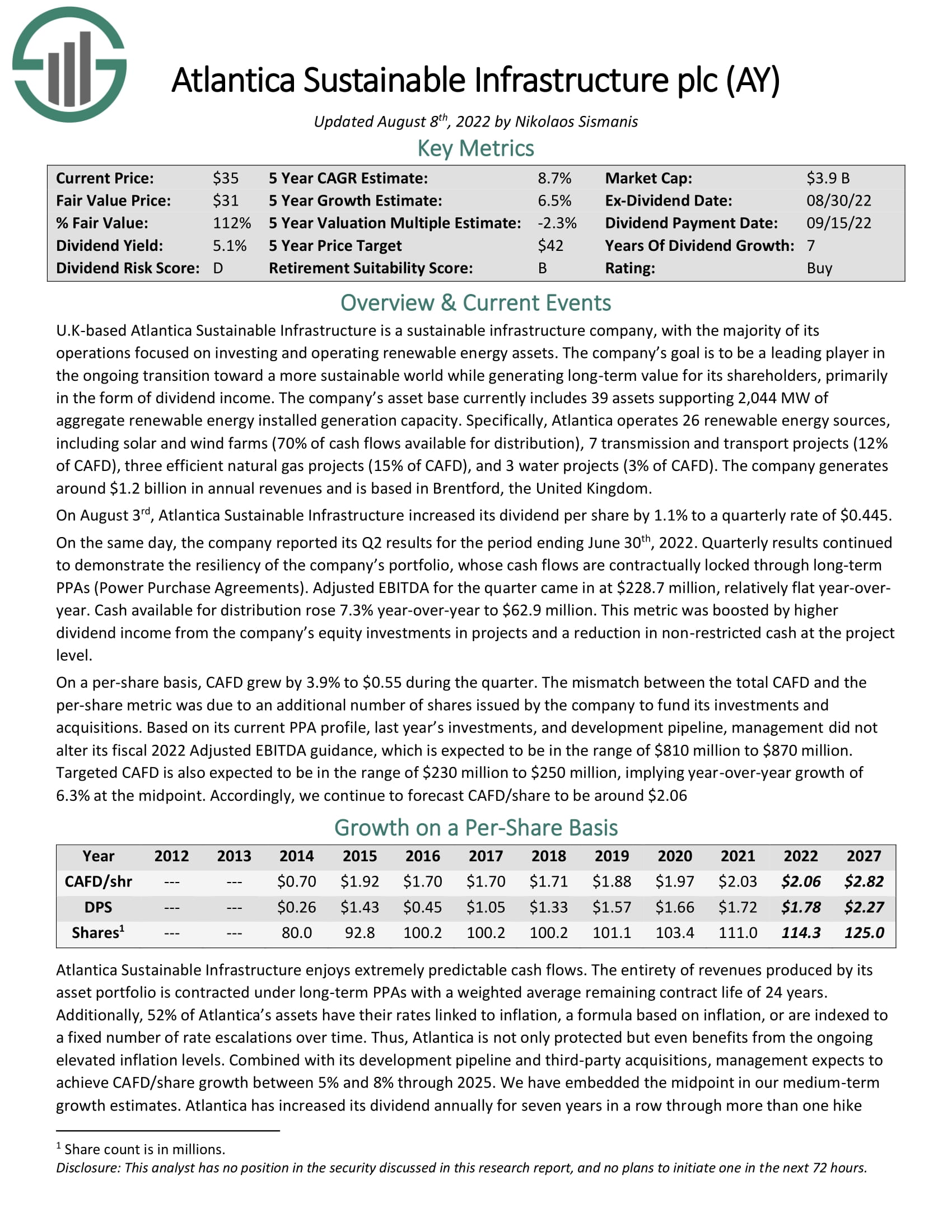

Atlantica Sustainable Infrastructure plc (AY)

Our final stock is Atlantica Sustainable Infrastructure, a company based in the United Kingdom that owns, manages, and invests in renewable energy, storage, natural gas, electric transmission lines, and water assets globally. The company makes the list for its wide variety of renewable energy assets, including more than 2,000 megawatts of renewable sources.

The company was founded in 2013, generates $1.2 billion in annual revenue, and trades with a market cap of $3.2 billion.

While Atlantica isn’t a pure play on renewable energy assets, given it has a large natural gas business, it has a focus on generating power through geothermal and other sustainable methods for the future. The company also has water desalinization assets that can process 17.5 million cubic feet per day, adding another sustainability dimension to the company’s portfolio.

The dividend streak stands at seven years, and the yield is the best of the group at 6.4%, meaning in terms of a pure income stock, Atlantica has little competition.

The stock is also below fair value, meaning we see total returns of 13.7%. These could accrue from 6.5% annual growth, a 2.2% tailwind from the valuation, and that robust 6.4% yield.

Click here to download our most recent Sure Analysis report on Atlantica Sustainable Infrastructure plc (preview of page 1 of 3 shown below):

{kind=link}

Final Thoughts

Investing for long-term returns can also include doing right by the planet. Above, we identified 10 sustainability stocks, all offering varying levels of dividend longevity, current yield, growth prospects, and total returns.

While we like Atlantica Infrastructure best due to its massive yield and total return prospects, we think all 10 have something to offer investors interested in sustainability and dividends.

The following articles contain stocks with very long dividend or corporate histories, ripe for selection for dividend growth investors:

The High Yield Dividend Aristocrats List is comprised of the 20 Dividend Aristocrats with the highest current yields. The Dividend Achievers List is comprised of ~350 stocks with 10+ years of consecutive dividend increases. The High Yield Dividend Kings List is comprised of the 20 Dividend Kings with the highest current yields. The Blue Chip Stocks List: stocks that qualify as Dividend Achievers, Dividend Aristocrats, and/or Dividend Kings The High Dividend Stocks List: stocks that appeal to investors interested in the highest yields of 5% or more. The Monthly Dividend Stocks List: stocks that pay dividends every month, for 12 dividend payments per year. The Dividend Champions List: stocks that have increased their dividends for 25+ consecutive years.Note: Not all Dividend Champions are Dividend Aristocrats because Dividend Aristocrats have additional requirements like being in The S&P 500. The Dividend Contenders List: 10-24 consecutive years of dividend increases. The Dividend Challengers List: 5-9 consecutive years of dividend increases. The Best DRIP Stocks: The top 15 Dividend Aristocrats with no-fee dividend reinvestment plans. The 2022 High ROIC Stocks List: The top 10 stocks with high returns on invested capital. The 2022 High Beta Stocks List: The 100 stocks in the S&P 500 Index with the highest beta. The 2022 Low Beta Stocks List: The 100 stocks in the S&P 500 Index with the lowest beta. The Complete List of Russell 2000 Stocks The Complete List of NASDAQ-100 Stocks