Updated on February 16th, 2022 by Felix Martinez

The Dividend Aristocrats are some of the best dividend stocks an investor will find. These are companies in the S&P 500 Index, with 25+ consecutive years of dividend increases.

We believe the Dividend Aristocrats are among the highest-quality dividend growth stocks around. For this reason, we created a downloadable spreadsheet of all 66 Dividend Aristocrats, along with important metrics such as price-to-earnings ratios and dividend yields.

You can download the Excel sheet of all 66 Dividend Aristocrats by clicking the link below:

Each year, we review all of the Dividend Aristocrats. The next stock in the series is an insurance broker giant Brown & Brown Inc. (BRO). BRO might not be a familiar stock for most investors, but it has certainly earned its place on the list.

BRO has now increased its dividend for an amazing 28 consecutive years. The company’s dividend is also very safe.

At the same time, BRO stock has experienced a multi-year rally in share price. As an insurance stock, it has benefited from the steady economic growth since the Great Recession ended. The end result is that the stock appears to be overvalued, which is why right now might not be the best time to buy Brown & Brown stock.

Business Overview

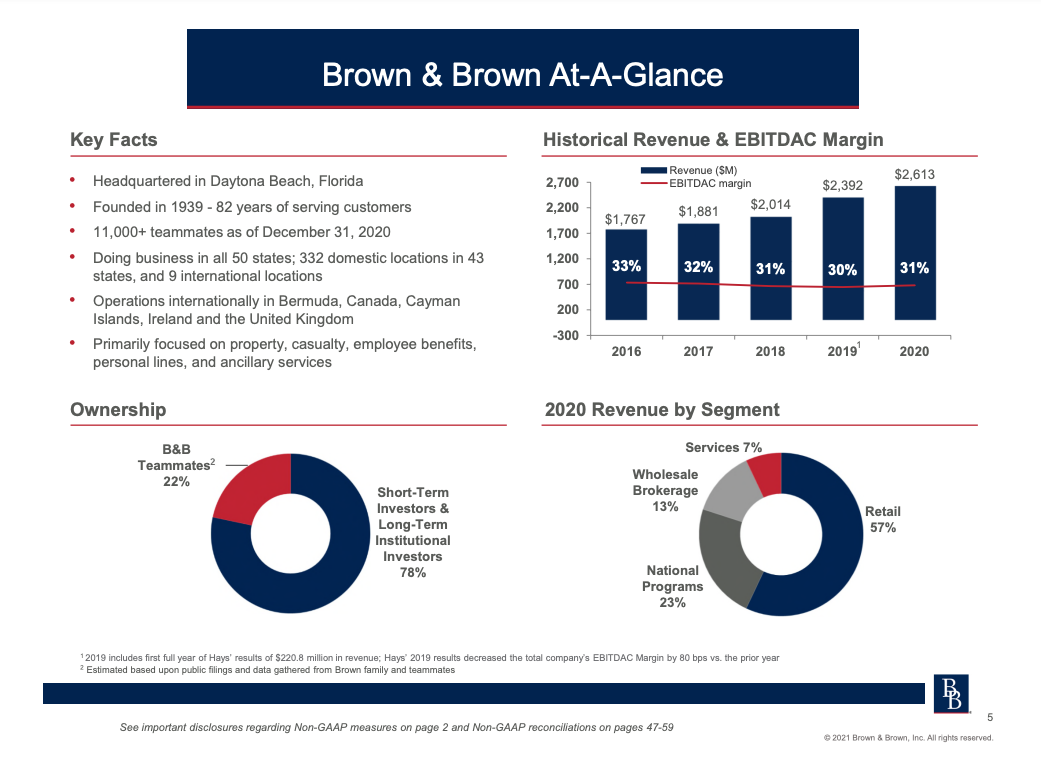

Brown & Brown Inc. is a leading insurance brokerage firm that provides risk management solutions to both individuals and businesses, with a focus on property & casualty insurance. Brown & Brown has a notably high level of insider ownership. Overall, Brown & Brown is a very shareholder-friendly company, as its 28-year streak of consecutive dividend increases qualifies it to be a member of the Dividend Aristocrats list. The company employs about 11,000 people, and produce about $3.1 billion in revenue last year, and trades with an $18.8 billion market capitalization.

Source: Investor Presentation

The company operates through four segments: the Retail Segment, which provides a range of insurance products and services to commercial, public and quasi-public entities, and professional and individual customers; the National Programs Segment, which acts as a general managing agent, provides professional liability and related package products; the Wholesale Brokerage Segment, which markets and sells excess and surplus commercial and personal lines insurance, and the Services Segment, which provides insurance-related services, including third-party claims administration and medical utilization management services.

The company has been diversifying its business segment throughout the years. Doing this allows the company to not be 100% dependent on one business segment. Thus, these segments have performed very well against their peers and have allowed BRO to achieve “best of breed” status in its industry.

Source: Investor Presentation

Growth Prospects

While 2020 was a very difficult year for the global economy, due to the coronavirus pandemic which weighed heavily on economic growth, BRO continued to generate steady profits. In 2021, the company continued to grow its earnings and the stock price continued to run higher with a total return of 48% for the entire year of 2021.

On January 24th, 2022, the company released its fourth-quarter and full-year results for Fiscal Year (FY)2021. Revenues for the quarter were $738.5 million, increasing by $96.4 million, or 15.0%, compared to the fourth quarter of the prior year. Commissions and fees increased by 15.3% and organic revenue increased by 9.0%. Net income was $101.7 million for the quarter, which increased by $4.4 million, or 4.5%. Earning per share increased to $0.42, or 31.3% versus the fourth quarter of the prior year.

For the entire year, the company generated $3,051.4 million in revenue, increasing by $438.0 million, or 16.8%, compared to 2020. Net income was $587.1 million for the year, which increased by $106.6 million, or 22.2%. Earning per share for the year increased to $2.19, or 31.1%, compared to 2020.

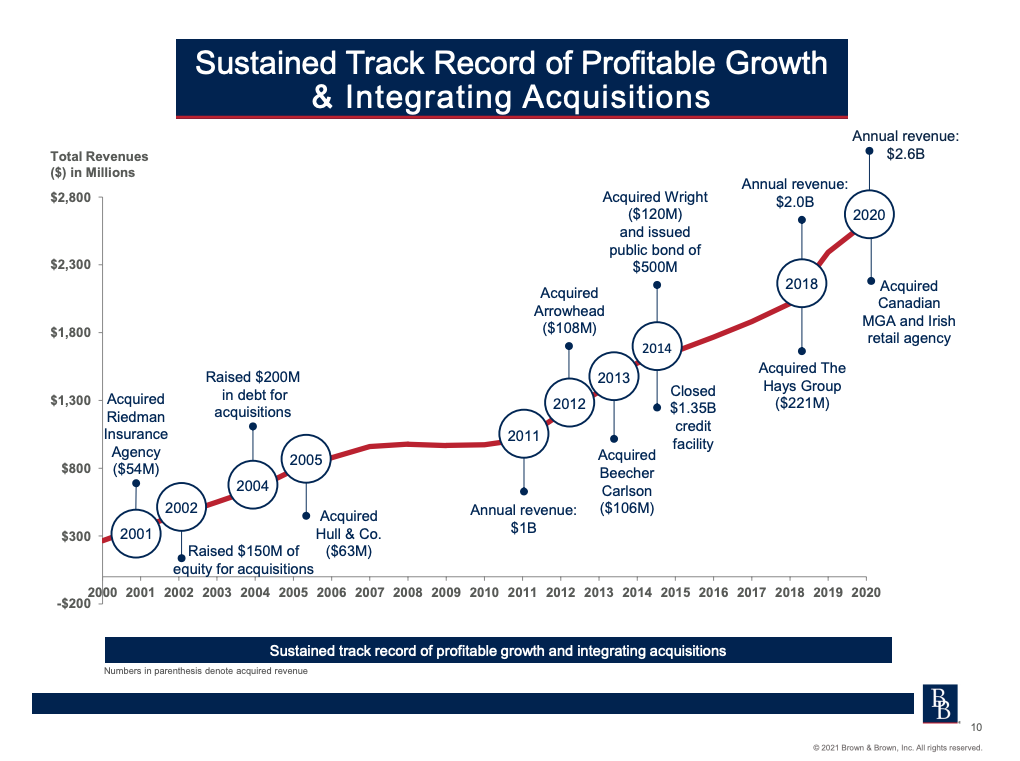

The company growth comes mainly from strategic acquisitions throughout the years. Since 2010, the company has acquired five different companies.

Source: Investor Presentation

We expect BRO to earn for the entire year of 2022 an earnings-per-share of $2.35. Also, we expect a 7% annual EPS growth over the next five years, comprised mainly of revenue growth and share buybacks.

Competitive Advantages & Recession Performance

Brown & Brown’s competitive advantage comes from its willingness to execute small and frequent acquisitions. This growth-by-acquisition strategy gives the company an enduring opportunity to continue growing its business for the foreseeable future. BRO is also modestly recession-resistant. For example, BRO’s competitive advantages allow it to maintain consistent profitability each year, even during recessions.

BRO’s earnings-per-share during the Great Recession are below:

- 2007 earnings-per-share of $0.68

- 2008 earnings-per-share of $0.59 (13% decline)

- 2009 earnings-per-share of $0.54 (8% decline)

- 2010 earnings-per-share of $0.56 (4% increase)

Durning the COVID-19 pandemic earnings grew from $1.40 per share in 2019 to $1.67 per share in 2020. This represents an increase of 19% year-over-year.

Valuation & Expected Returns

Based on expected EPS of $2.35 for 2022, BRO stock trades for a price-to-earnings ratio of 28.4, using today’s stock price of ~$66. BRO held an average price-to-earnings ratio of 22.6 over the past 10 years. However, we think that a fair earning multiple is 24.0. Thus, BRO’s stock appears to be overvalued, based on its average valuation multiples.

If the company stock experiences a decline in the valuation multiple to our fair P/E of 24.0, it would reduce annual shareholder returns by 3.0% annually over the next five years.

Earnings growth and dividends will positively impact future returns. First, we expect the company to grow earnings-per-share by 7% per year through 2027.

Lastly, BRO stock has a dividend yield of 0.6%. Putting it all together, a breakdown of our expected future returns is as follows:

- 7.0% expected earnings-per-share growth

- 0.2% dividend yield

- -3.0% negative return from valuation contraction

In this projection, total shareholder returns could reach 4.0% annualized through 2027. This is a modest expected rate of return for this company.

Final Thoughts

BRO has endured a number of challenges over the past decade, including the Great Recession of 2008-2009 and the coronavirus pandemic of 2020. And yet, it continued to raise its dividend each year. Very few companies have this ability, which makes this company a rare dividend growth stock.

BRO has a leadership position in its insurance industry and durable competitive advantages. These factors have the company positioned for growth in future years, making it highly likely that the company will continue to increase its dividend.

The company is a high-quality business and a dividend growth company, but the stock is simply too overvalued to earn a buy rating from Sure Dividend at this time. Thus, we give this stock a hold at the current price. With that said, on a stock price pullback, we would-be buyers of this quality insurance stock.

{kind=link}

{kind=link}

{kind=link}