Published on April 16th, 2020 by Eli Inkrot

The Dividend Aristocrats are an exclusive group of companies that have not only paid but also increased their dividend for at least 25 consecutive years. We believe the Dividend Aristocrats are among the highest-quality dividend growth stocks in the entire market.

With this in mind, we created a downloadable Excel list of all the Dividend Aristocrats, along with relevant financial metrics like dividend yields, price-to-earnings ratios, and payout ratios.

You can download your free copy of the Dividend Aristocrats list (with important financial metrics like dividend yields and price-to-earnings ratios) by clicking on the link below:

Otis Worldwide (OTIS) was recently spun off, following the merger of United Technologies and Raytheon. Since United Technologies had previously qualified as a Dividend Aristocrat, the spin-offs qualify as well.

All three companies – Raytheon Technologies, Carrier Global and Otis Worldwide – take with them a 25+ year dividend increase streak as a result of the United Technologies lineage. This article will discuss Otis Worldwide’s business model, growth potential, recession resilience, and valuation.

Business Overview

Otis has an extensive history, being founded in 1853 and having previously gone public in 1920. Today Otis is the leading company for elevator and escalator manufacturing, installation and service. The company’s products move 2 billion people per day and maintain more than 2 million customer units worldwide.

The $20 billion market cap business, headquartered in Connecticut, generated $13.1 billion in sales in 2019 and employs 69,000 people.

{kind=link}

Source: Otis Investor & Analyst Day

While Otis has not yet posted results as a standalone business, looking at the company’s recent performance when it was part of United Technologies can be useful.

For the quarter ending December 31st, 2020 Otis recorded net sales of $3.36 billion, up 1.9% compared to Q4 2018, while adjusted operating profit equaled $521 million, a 2.2% increase.

For all of 2019 Otis generated $13.11 billion in sales, up 1.6% year-over-year, while adjusted operating profit totaled $2.01 billion, representing a 1.4% increase. Meanwhile, the operation margin remained flat at 15.4%

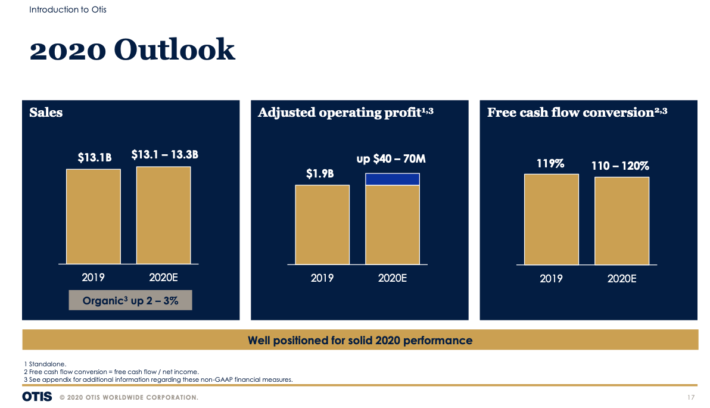

On February 11th, Otis provided a 2020 outlook:

{kind=link}

Source: Otis Investor & Analyst Day

This included $13.1 billion to $13.3 billion in sales, a $40 million to $70 million increase in operating profit and $1.0 billion to $1.1 billion in free cash flow. Of course, the 2020 guidance may not be reliable due to the recent and massive impact of the coronavirus.

Over the medium-term the company expects low-to-mid organic sales growth, mid-single digit operating profit growth and high-single digit EPS growth.

{kind=link}

Source: Otis Investor & Analyst Day

Again, this was prior to the widespread coronavirus outbreak, which could materially influence the business, with demand in the short-term being the main concern. Still, despite the short-term challenge posed by the coronavirus, we maintain a positive long-term outlook for Otis.

Growth Prospects

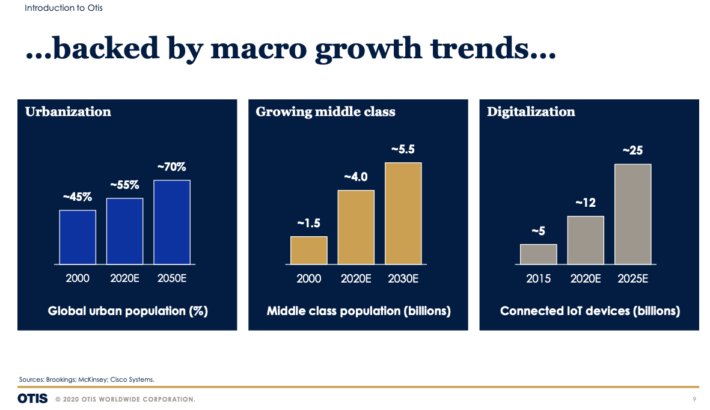

As indicated above, Otis anticipates reasonable growth in sales and earnings over the intermediate term. This result can materialize via a number of trends that have been and will continue to emerge:

{kind=link}

Source: Otis Investor & Analyst Day

Otis has a number of long-term growth drivers available in the way of increased urbanization, a growing middle class and digitalization. All of these factors will continue to spur demand for Otis’ products and should bode well for the category leader. At the very least, Otis stands a very good shot at capturing its “fair share” of growth in the industry.

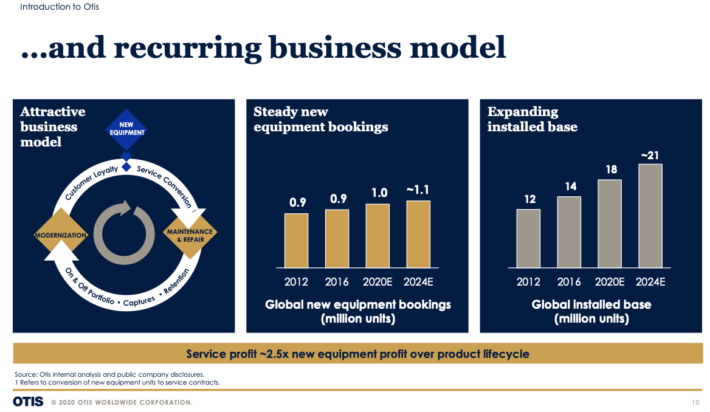

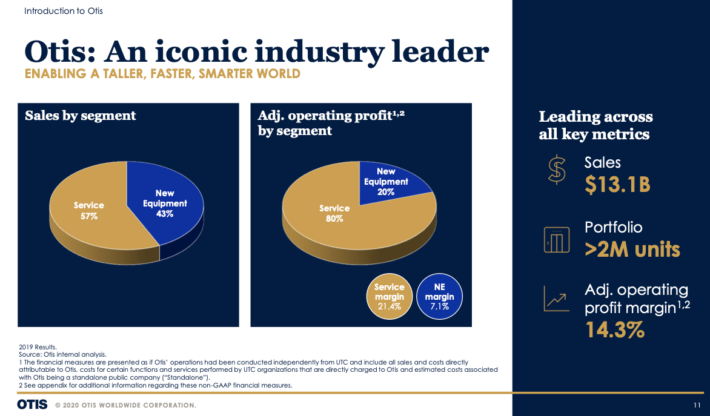

That being said, the current coronavirus pandemic calls into question all demand in the short-term and could very well be a hindrance for some time. Still, with services making up 57% of sales and 80% of operating profit, there is some resiliency to the business.

New sales can be cyclical but servicing an already installed base should prove more resistant in economic downturns. Furthermore, service revenue makes up a much larger portion of profits for Otis.

{kind=link}

Source: Otis Investor & Analyst Day

We are forecasting 6% annual growth for Otis, the short-term demand concerns notwithstanding, which is slightly lower than Otis’ guidance and UTX’s historical record.

Competitive Advantages & Recession Performance

Otis enjoys a competitive advantage in its namesake brand, along with the #1 position in the category the company created.

{kind=link}

Source: Otis Investor & Analyst Day

Additionally, with the largest installed base of elevators and escalators, reoccurring service revenue can smooth out results in less certain times. Although Otis does not yet have a standalone history, during the last recession its parent company United Technologies posted earnings-per-share of $4.90, $4.12, $4.74 and $5.49 during the 2008 through 2011 timeframe.

While some of that ballast is gone with the company splitting up, we still believe Otis should perform reasonably in lesser times. Moreover, the targeted ~40% dividend payout ratio ought to allow for flexibility in the future.

Valuation & Expected Returns

We are forecasting $2.18 in earnings-per-share this year for Otis, based on the expectation of $12 billion in sales and an 8% profit margin. This could be too conservative considering that the company generated over $13 billion in sales last year. However, due to ongoing worldwide uncertainty, we have reduced our expectations for 2020.

If Otis generates $2.18 in earnings-per-share this year and grows that number by 6% annually, this would imply a future earnings-per-share figure of $2.92 after five years, keeping in mind that this is one possibility out of a wide range of potential outcomes.

At 16 times earnings – more or less in-line with UTX’s history and taking into consideration the enhanced risk of being a standalone business paired against strong growth avenues and reoccurring revenue from servicing – this would equate to a future price of ~$47.

While a dividend has not yet been declared, management has indicated the anticipation of a ~40% payout ratio, equating to a ~$0.87 starting dividend payment in the first full year. Using the same 6% growth rate, this could mean collecting ~$5 in cash payments per share for next half decade.

Putting these items together, you come to a collective expected value of ~$52. With shares presently trading hands near $46, this implies the potential for 2.4% annualized total returns.

This is not especially attractive and largely is a result of shares trading in excess of 20 times expected earnings. We believe it is better to be a bit cautious as it pertains to the fair value estimate, rather than anticipating above-average growth or an elevated valuation multiple.

Final Thoughts

Otis has been a very strong business for 167 years. Now that it is once again a standalone company, it offers a “pure-play” on a variety of important and growing trends around the world. While the cyclicality of the firm may have increased, we are encouraged by the ongoing service revenue.

However, in our view, today’s valuation leaves something to be desired. This view could be too conservative if the business performs better than expected, but we are not yet willing to make that speculation at this juncture. It is likely the coronavirus will have a significant impact on Otis, at least in the short-term. With a relatively low expected rate of return, we do not recommend Otis stock as a buy right now.