Updated on May 7th, 2019 by Kay Ng

Kevin O’Leary is Chairman of O’Shares Investments, but you probably know him as “Mr. Wonderful”.

He can be seen on CNBC as well as ABC’s Shark Tank. Investors who have seen him on TV have likely heard him discuss his investment philosophy.

Mr. Wonderful looks for stocks that exhibit three main characteristics. First, they must be quality companies with strong financial performance and solid balance sheets.

Second, he believes a portfolio should be diversified across different market sectors.

Third, and perhaps most important, he demands income—he insists the stocks he invests in pay dividends to shareholders.

The O’Shares FTSE U.S. Quality Dividend ETF (OUSA) owns stocks that display a mix of all three qualities. It is an interesting source of quality dividend growth stocks.

Free Excel Download: Get a free Excel Spreadsheet of all the holdings in the O’Shares FTSE U.S. Quality Dividend ETF, complete with metrics that matter – including P/E ratio and dividend yield. Click here to download Kevin O’Leary’s favorite stocks now.

This article analyzes the fund’s top 10 biggest holdings in detail.

Table Of Contents

The top 10 holdings from the O’Shares FTSE U.S. Quality Dividend ETF are listed in order of their weighting in the fund, from lowest to highest.

PepsiCo (PEP) Philip Morris International (PM) Pfizer (PFE) Chevron (CVX) Home Depot (HD) Intel (INTC) Procter & Gamble (PG) Exxon Mobil (XOM) Johnson & Johnson (JNJ) Cisco Systems (CSCO)No. 10: PepsiCo, Inc. (PEP)

Dividend Yield: 2.9%

Market Capitalization: $178 billion

Forward Price-to-Earnings Ratio: 23.1

Pepsi is a global food and beverages company whose products are available in more than 200 countries and territories. Headquartered in Purchase, New York, Pepsi is one of the largest publicly-traded food and beverage companies. The revenue mix is about 54% food to 46% beverage.

Pepsi’s top brands include Pepsi, Frito-Lay chips, Mountain Dew, Tropicana orange juice, Gatorade, Doritos, and Quaker foods.

Source: Pepsi’s 2018 Annual Report, page 151

Pepsi’s recent performance has been steady. In the most recent quarter, its revenue increased by 2.6% to $12.9 billion, while its diluted earnings per share grew 6.4% to $1.00 per share.

The consumer defensive sector has been one of the stock market’s most stable performers throughout history. The sector is also extraordinarily recession-resistant. With this in mind, it’s unsurprising that Mr. Wonderful has Pepsi as a top 10 holding.

Pepsi is trading at 23.1x expected 2019 earnings. The company appears to be pricey relative to its historical average valuation levels. In the past decade, Pepsi’s average annual price-to-earnings ratio was 18.9.

Although Pepsi is more expensive than the S&P 500 right now, the company offers a dividend yield of 2.9%, which is more favorable than the overall market’s yield of ~1.8%.

In addition, PepsiCo has a highly secure dividend. PepsiCo is a Dividend Aristocrat, an exclusive group of S&P 500 Index companies with 25+ consecutive years of dividend increases.

You can see a video further discussing PepsiCo’s dividend safety below:

Pepsi is an established company. Earnings per share are expected to grow about 5.5% per year over the next 5 years. Earnings growth will be comprised mainly of organic revenue growth, plus share repurchases.

This growth combined with the company’s 2.9% dividend yield gives investors expected total returns of 8% to 9% per year if the company is able to maintain the high price-to-earnings ratio of about 23. From the company’s high valuation, it’s in investors best interest to wait for a pullback before buying.

No. 9: Philip Morris International Inc. (PM)

Dividend Yield: 5.4%

Market Capitalization: $131 billion

Forward Price-to-Earnings Ratio: 16.6

Philip Morris is one of the largest tobacco companies in the world. It consists of the international operations that Altria (MO) spun out. Philip Morris sells cigarettes under the Marlboro brand and others, in the international markets. Its sister company, Altria, sells the Marlboro brand and others in the U.S.

Philip Morris has been holding its ground but has been negatively impacted by a strong U.S. dollar. In the most recent quarter, its revenue declined by 2.1% to $6.8 billion compared to the same quarter in the prior year. Were it not for a strong U.S. dollar against other relevant currencies, the revenue would have grown 3.2%.

Adjusted earnings per share were $1.09 against $1.00 in the same quarter of 2018. The company’s total international market share climbed 1.0% to 28.4%, while its total international heated tobacco unit market share rose 0.5% to 2.0%.

Although the shipment volumes were pretty much flat for cigarettes, we wanted to highlight that the heated tobacco units experienced double-digit growth by climbing 20.2% year-over-year. Still, the heated tobacco units are currently a small part of the business — only making up roughly 6.5% of the shipment volumes for the quarter.

The tobacco industry has historically been a good place for current income. That’s what investors are getting by investing in the stock with Philip Morris currently offering a juicy yield of 5.4% compared to the S&P 500’s yield of ~1.8%.

The following video further discusses Philip Morris from the perspective of dividend safety:

The company expects adjusted EPS to increase again in 2019, which will further boost the sustainability of the dividend. Management guidance calls for approximately 8% adjusted EPS growth for the full year 2019.

Source: Philip Morris Q1 2019 Press Release, page 2

Philip Morris trades at 16.6x expected 2019 earnings. The company appears to be fairly valued relative to its historical average valuation levels. In the past decade, Philip Morris’ average annual price-to-earnings ratio was 16.5.

Adjusting for the deconsolidation of the Canadian RBH subsidiary, management forecasts diluted earnings per share to increase by 5.2% this year. Adjusting further to ignore currency rates, management forecasts diluted earnings per share to climb 8% or higher this year.

No. 8: Pfizer Inc. (PFE)

Dividend Yield: 3.7%

Market Capitalization: $219 billion

Forward Price-to-Earnings Ratio: 13.7

Pharmaceutical companies benefit from the fact that many people cannot go without their medications. This heavily insulates Big Pharma’s bottom line. Further, pharmaceutical companies have the ability to raise prices on key drugs. Because of this, healthcare stocks like Pfizer have proven to be a stable dividend payer.

In 2018, Pfizer’s revenue increased by 2%, while its adjusted earnings-per-share rose 13% to $3.00. Pfizer’s two major segments contributed largely to its performance. For the year, Innovative Health revenue increased by 6%, while Essential Health revenue declined by 5% on an operational basis.

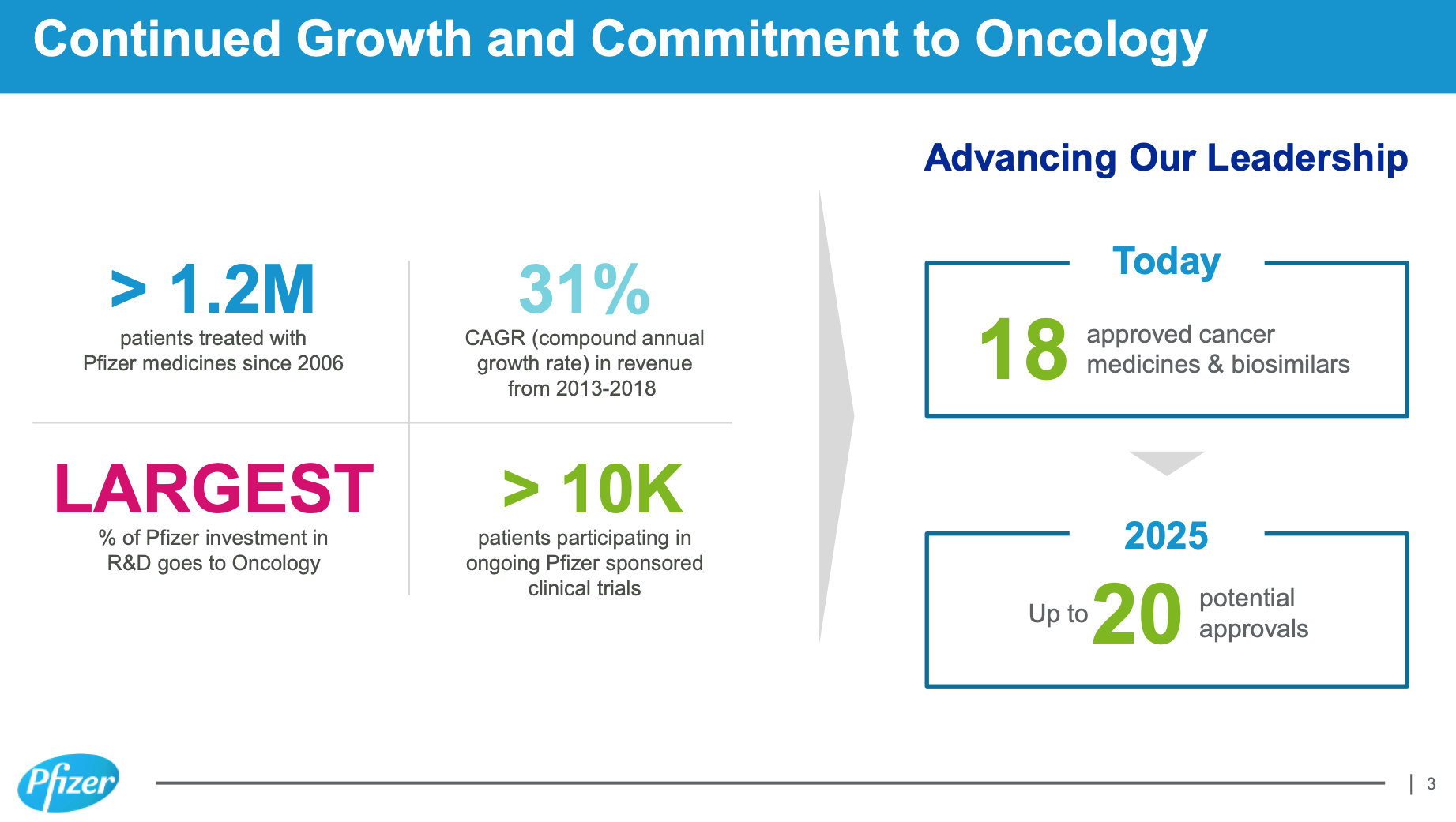

Pfizer has a strong oncology portfolio and has been spending a large portion of its investments in this area. Currently, it has 18 approved cancer medicines and biosimilars and up to 20 potential approvals expected by 2025. Down the road, new drugs should help boost Pfizer’s revenue.

{kind=link}

Source: Cowen and Company 39th Annual Healthcare Conference (March 2019), Slide 3

The drug manufacturer has historically generated pretty stable earnings through economic cycles. Coupled with a very sustainable payout ratio of about 50% this year, investors can continue to expect steady dividend growth that more or less matches with its earnings growth. With this in mind, it’s unsurprising that Mr. Wonderful has Pfizer as a top 10 holding.

Pfizer trades at 13.7x expected 2019 earnings. The company appears to be fairly valued. The stock offers a dividend yield of 3.7%, which is more favorable than the overall market’s yield of ~1.8%. Earnings-per-share growth is estimated to be about 5% per year over the next few years. So, an investment today can deliver total returns of roughly 9% per year.

No. 7: Chevron (CVX)

Dividend Yield: 4%

Market Capitalization: $223 billion

Forward Price-to-Earnings Ratio: 14.1

Along with Exxon Mobil that we’ll discuss further down the article, Chevron is one of the Big Oil Supermajor stocks. Chevron has a $223 billion market cap and has a fabulous dividend track record. The company has paid an increasing dividend every year since 1988. Chevron is a Dividend Aristocrat for having increased its dividend for at least 25 consecutive years.

Despite the oil and gas price collapse in 2014 that left energy companies with a much more challenging environment to operate in, Chevron still managed to increase its dividend at a compound annual growth rate of 2.8% in the last five years.

Investors can watch a video further discussing Chevron’s dividend safety below:

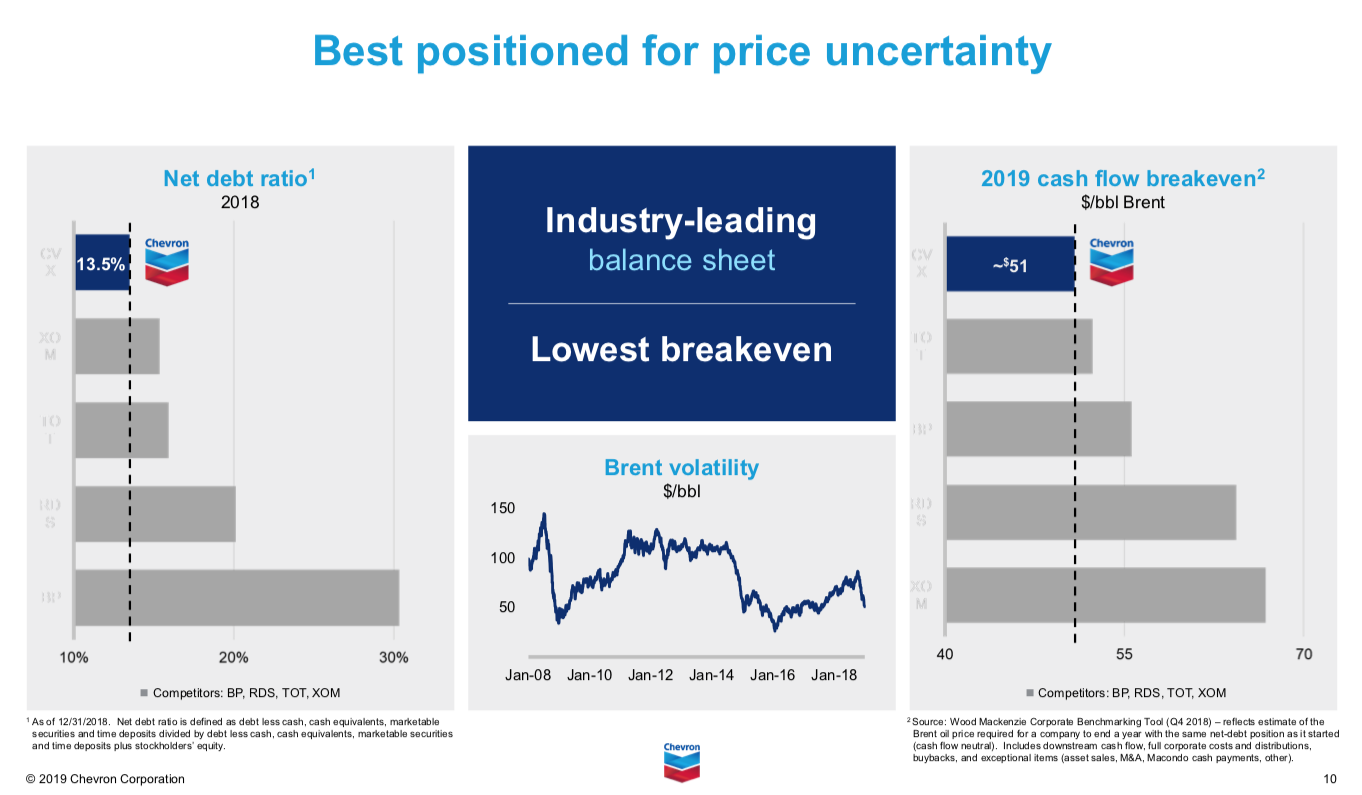

At the start of 2019, Chevron increased its dividend per share by 6.25%, greater than its five-year dividend growth rate of 2.8%, which suggests the operating environment has improved. That’s also thanks to an integrated business model with upstream and downstream operations and a competent management team.

For example, Chevron aims to sell $5-10 billion of assets from 2018-2020 to improve its upstream portfolio. Chevron now enjoys an industry-leading balance sheet and the lowest cash flow breakeven oil price among its competitors, including BP (BP), Royal Dutch Shell (RDS.A)(RDS.B), Total (TOT), and Exxon Mobil (XOM).

{kind=link}

Source: Chevron April 2019 Investor Presentation, Slide 10

The professional management team has helped Chevron remain profitable and maintain dividend increases. Although Chevron enjoys the lowest cash flow breakeven oil price among the Big Oil Majors, it doesn’t change the fact that it will be a major beneficiary if commodity prices continue to rise moving forward.

Additionally, Chevron stock currently offers an attractive 4% dividend yield.

No. 6: Home Depot (HD)

Dividend Yield: 2.7%

Market Capitalization: $225 billion

Forward Price-to-Earnings Ratio: 20.3

Home Depot is the largest home improvement retailer in the United States with a market capitalization of almost $225 billion. Similar to its competitor, Lowe’s (LOW), Home Depot tends to grow at a double-digit rate.

It’s not hard to see why Mr. Wonderful is a fan of Home Depot. The company has long been a leading operator in its industry and passes its financial success onto its shareholders in the form of steadily rising dividend payments.

Most recently, in February 2019, Home Depot increased its dividend by 32%, equating to an annual payout of $5.44 per share. Its payout ratio is about 55%, indicating there is room to grow the dividend in the future.

Source: Home Depot 2017 Annual Meeting Presentation

Fiscal 2018 was another successful year for Home Depot. The home improvement retailer saw sales increase by 7.2% to $108 billion, net earnings increase by 29% to $11.1 billion, and diluted earnings-per-share increase by 33% (partly boosted by share repurchases) to $9.73.

The company’s stock price reacted accordingly. In fact, over the last five years, Home Depot’s stock has soared past the performance of the U.S. market (the S&P 500). In that time, while the S&P 500 Index returned 11.5% per year–an entirely respectable rate of return–Home Depot generated annual returns of 23%, more than double the performance of the broader market index.

As a result, Mr. Wonderful’s decision to own Home Depot has been rewarding. We think Home Depot will handsomely reward long-term investors who buy the dividend growth stock on meaningful dips.

No. 5: Intel Corp (INTC)

Dividend Yield: 2.5%

Market Capitalization: $227 billion

Forward Price-to-Earnings Ratio: 11.7

The technology sector is a surprisingly good source of dividend stocks such as Intel. The company has a market-beating 2.5% dividend yield and is well-positioned to benefit from trends such as autonomous driving and the Internet of Things.

More broadly, Intel’s products (microchips and semiconductors) will experience increasingly strong demand as the demand for data undoubtedly continues to grow at a torrential rate.

Source: Intel Investor Presentation

Intel has three major focuses that it calls ‘big bets’ and is devoting significant resources to developing.

The first is memory. As an existing leader in this market, Intel is likely to benefit from growth in this fast-growing segment of the technology industry.

The second is autonomous vehicles, which the company expects to be mainstream by 2030 thanks to companies like Tesla (TSLA), General Motors (GM), and Ford (F).

The third is 5G, which is expected to connect 50 billion devices once implemented.

These three growth drivers are explored in more detail below.

Source: Intel Investor Presentation

Intel’s market leadership and robust dividend supported by a payout ratio of about 30% certainly seem like quality to us, and definitely contribute to the company being held in Mr. Wonderful’s investment portfolio.

No. 4: Procter & Gamble (PG)

Dividend Yield: 2.8%

Market Capitalization: $263 billion

Forward Price-to-Earnings Ratio: 23.6

Procter & Gamble is a stalwart among dividend stocks. It has increased its dividend for the past 60 years in a row. This makes the company one of only 25 Dividend Kings, a list of stocks with 50+ years of rising dividends.

It has done this by becoming a global consumer staples behemoth. It sells its products in more than 180 countries around the world with annual sales of more than $65 billion.

The company is organized into five operating segments:

Fabric and Home Care (32% of sales) Baby, Feminine, and Family Care (27% of sales) Beauty (19% of sales) Health Care (12% of sales) Grooming (10% of sales)P&G has a heavy international presence; it generates about 56 of its sales from outside North America.

From fiscal 2014 to 2017, net sales fell 12.5% and adjusted-earnings-per-share fell 7.1% as P&G offloaded about 100 non-core brands. This has allowed P&G to streamline its operations and focus on the remaining 65 core brands, which management believes hold the most growth potential.

{kind=link}

Source: Investor Presentation

The strategy to spur growth has started to bear fruit. In fact, adjusted earnings-per-share bottomed in fiscal 2016. Since then, adjusted earnings-per-share has climbed 7-8% per year.

Focusing on core brands helped with making the company leaner and cutting costs. For example, P&G applied more agile innovation principles and was able to bring Pampers Pure diapers in consumers in about half the time of a typical rollout in the capital-intensive diaper market.

Cost cutting and focusing on core brands helped boost profitability and growth. Earnings growth has led to improving dividend growth. In fiscal 2017, 2018, and 2019, P&G increased its dividend per share by 1.5%, 3.3%, and 4%, respectively.

P&G has a highly secure dividend payout, which is further illustrated in the following video:

Even more impressive is that P&G has increased its dividend for over 60 years in a row, making it a member of the exclusive Dividend Kings, a list of stocks with annual dividend increases for at least 50 consecutive years.

The stock’s yield of 2.8% is a big boost from the market’s 1.8%. However, total returns will likely be below average because the stock appears overvalued at the moment.

No. 3: Exxon Mobil (XOM)

Dividend Yield: 4.5%

Market Capitalization: $327 billion

Forward Price-to-Earnings Ratio: 14.7

Exxon Mobil is the largest publicly-traded oil company in the world. It has a $329 billion market cap and an unparalleled dividend track record among its peer group.

The company has paid a dividend for more than 100 years. And, Exxon Mobil is a Dividend Aristocrat, with annual dividend increases for 36 consecutive years.

Exxon Mobil and Chevron are the only two energy-sector stocks on the list of Dividend Aristocrats. You can see a video further discussing Exxon Mobil’s dividend below:

Despite the oil and gas price collapse in 2014 that left energy companies with a much more challenging environment to operate in, Exxon Mobil still increased its dividend at a compound annual growth rate of 5.6% in the last five years — this was double the dividend growth rate of Chevron.

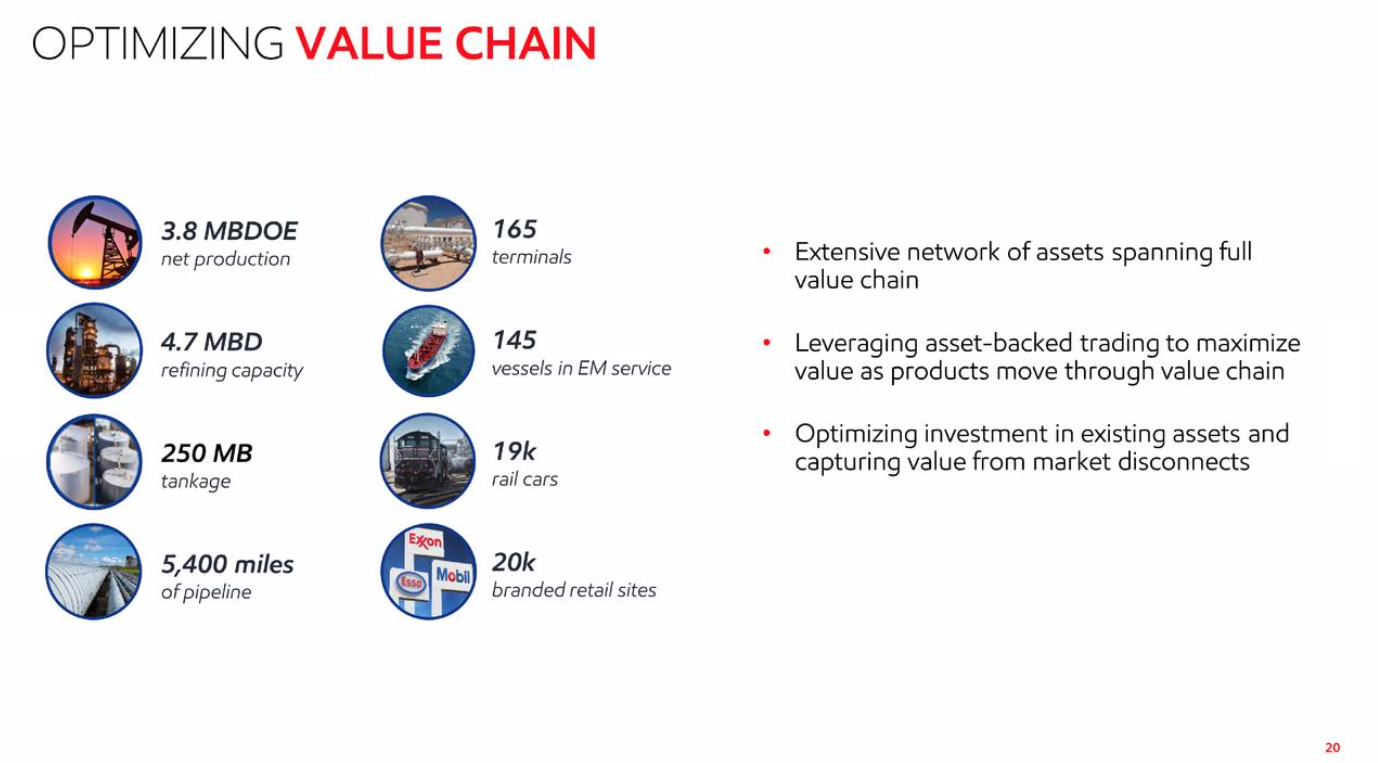

At the start of 2019, Exxon Mobil increased its dividend per share by 6%, which is in line with its five-year dividend growth rate of 6%. The oil giant’s consistent dividend growth is thanks to an integrated business model with upstream and downstream operations and a competent management team that continues to optimize the business that spans the full value chain.

{kind=link}

Source: Q1 2019 Earnings Call, Slide 20

Exxon Mobil’s strong business model has allowed the company to generate industry-leading returns on capital. Its five-year return on capital is 9.8%, which was greater than Chevron’s 5.5%.

Maintaining profitability is crucial for a company in order to continue raising its dividend. Exxon Mobil has been doing a good job in that respect, and it will be a major beneficiary if commodity prices rise.

Exxon Mobil stock has an attractive 4.5% dividend yield.

No. 2: Johnson & Johnson (JNJ)

Dividend Yield: 2.7%

Market Capitalization: $378 billion

Forward Price-to-Earnings Ratio: 16.6

J&J is one of the best dividend stocks investors can buy, so it is not surprising to see it in Mr. Wonderful’s portfolio.

This year marks the company’s 57th consecutive year of dividend growth, an incredible dividend history which makes J&J a member of the Dividend Kings.

J&J has one of the safest dividends in the entire stock market. We further discuss J&J’s strong dividend safety in the following video:

Its long history of dividend growth is thanks to J&J’s excellent business model. J&J has a very strong brand—approximately 70% of the company’s sales come from products that have either the number one or number two positions in their respective categories.

This brand strength has led to consistent growth for decades. According to J&J, it has achieved positive growth of adjusted earnings for 35 consecutive years.

J&J is organized into three business segments:

Pharmaceutical (40.7% of sales) Medical Devices (27% of sales) Consumer (13.9% of sales)It is seeing strong results in each of its businesses. 2018 was a highly successful year for J&J, with steady growth across its various businesses.

{kind=link}

Source: Earnings Presentation

The pharmaceutical business is performing the best so far this year, with 4.1% revenue growth to $10.2 billion through the first quarter. However, sales of the consumer and medical devices segments declined 2.4% and 4.6%, respectively, to $3.3 billion and $6.5 billion.

That said, J&J’s consumer business is still very valuable to the company because it has many strong brands that provide a great deal of stability. Additionally, for 2019, management estimates total revenue to stay more or less flat and earnings-per-share growth to be roughly 5%.

J&J stock has a price-to-earnings ratio of 16.6. The company is trading above its historical average valuation multiple of about 16. With that said, J&J is among the safest investments around for long-term dividend growth.

It is extremely likely the diversified healthcare giant will continue its steady growth for decades to come. This high degree of safety helps to offset the company’s high valuation relative to its historical average.

While J&J’s valuation is high relative to its historical average, it is not particularly pricey compared to other stocks in the S&P 500. A rising tide lifts all valuations – and J&J is no exception. J&J makes a great core long-term holding for risk-averse dividend-growth investors.

No. 1: Cisco Systems, Inc. (CSCO)

Dividend Yield: 2.5%

Market Capitalization: $242 billion

Forward Price-to-Earnings Ratio: 18.3

Cisco is a global technology leader. Its routers and switches are work makes networks, the largest being the internet, work.

The strong run-up of more than 60% in the stock over the last two years or so has made Cisco the largest holding in Mr. Wonderful’s portfolio.

The tech company is a relatively young dividend-growth stock. Cisco only started paying a dividend in 2011, but proceeded with a dividend hike every year since. Incredibly, its dividend is 11x what it was eight years ago. Therefore, Cisco has made it as a Dividend Challenger with a dividend-growth track record of at least five years.

With a payout ratio of about 46% this year, Cisco will likely continue growing its dividend closer to its earnings growth rate.

Cisco brings in annual revenues of about $49 billion and enjoys high margins. Its five-year operating margin is north of 24%.

{kind=link}

Source: Cisco 2018 Annual Report, Page 4

Cisco stock has a forward price-to-earnings ratio of 18.3. This is higher than its decade’s average of about 15. The company has experienced multiples expansions due to having an increasing subscription-based revenue that leads to higher predictability. Therefore, the expansion of the valuation multiple appears to be warranted in this case.

With that said, the stock does look moderately overvalued today based on our estimated earnings-per-share growth rate of about 6% over the next few years. Interested investors should look for a better entry point.