Updated on March 2nd, 2020 by Nathan Parsh

Business Development Companies – or BDCs, for short – can be a great source of current yield for income investors. You can see our BDC list here.

Main Street Capital Corporation (MAIN) is a great example of this. This BDC has a current annualized dividend yield of 6.7%. With the addition of two semi-annual dividends, the current yield is 8%. Better yet, Main Street Capital Corporation pays monthly dividends.

You can download our full Excel spreadsheet of all monthly dividend stocks (along with metrics that matter like dividend yield and payout ratio) by clicking on the link below:

The stock’s high dividend yield and monthly payments make it a solid choice for income investors at the security level. But what about the strength of the underlying business?

Fortunately for investors, Main Street Capital’s business appears to be performing well. This article will discuss the investment prospects of Main Street Capital Corporation in detail.

Business Overview

Main Street Capital Corporation operates as a debt and equity investor for lower middle market companies (those with $5-$50 million of annual revenues) seeking to transform their capital structures. The BDC has the capability to invest in both debt and equity, which gives it a significant advantage over companies who invest in private debt or private equity alone.

Main Street Capital Corporation also invests in the private debt of middle market companies (not lower middle market companies) and has a budding asset management advisory business.

{kind=link}

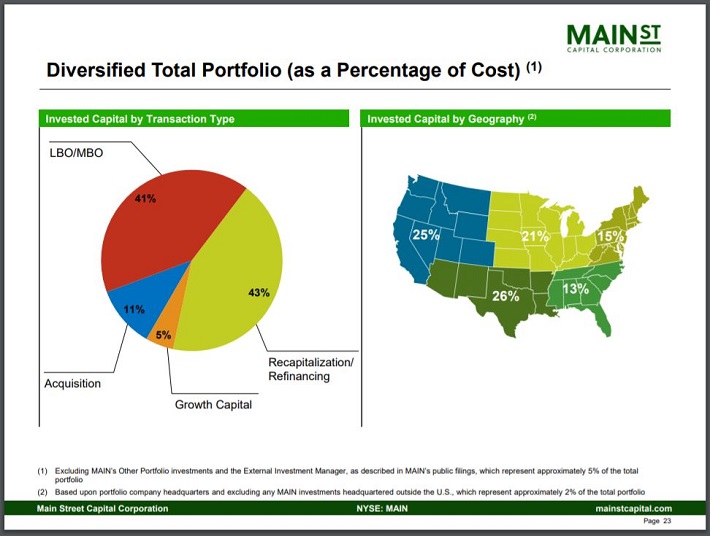

Source: Q4 Investor Presentation, slide 23.

The BDC’s corporate structure is rather simple. Main Street Capital Corporation operates three funds:

The Main Street Mezzanine Fund The Main Street Capital II Fund The Main Street Capital III FundSince Main Street Capital Corporation is the operator of its own investment funds, management fees are kept to a minimum, which gives it a cost-based competitive advantage over its competitors who outsource their fund management.

Main Street Capital Corporation’s holdings are highly diversified by both transaction type and geography. By transaction type, the BDC acquires most of its deals via recapitalization and leveraged buyouts. By geography, only the Southwestern United States (26%) and the Western United States (25%) make up more than a quarter of all invested capital.

Main Street Capital Corporation also has a very high degree of diversification by industry. The largest industry representation in the BDC’s investment portfolio comes from Machinery at 8% followed by Construction & Engineering, Media and IT Services all at 5%.

Growth Prospects

Main Street Capital Corporation’s growth prospects come from its unique strategy to driving investment returns. Investors who own the stock are rewarded in three ways. First, the BDC sustains its high monthly dividend and grows it over time.

Second, the BDC regularly pays supplemental dividends to further reward its investors. MAIN shareholders received an extra $0.24 in dividends in June and an extra $0.25 per share in December. Lastly, Main Street Capital Corporation uses its superior investment returns to grow its net asset value over time, which creates capital gains at the security level for the company’s shareholders.

At the business level, Main Street Capital Corporation’s growth will be driven by its expertise in the lower middle market segment of the economy.

A major catalyst for Main Street Capital Corporation is the growth of its new asset management business. In May of 2012, the BDC’s asset management business was born when MAIN entered into an advisory agreement with the investment advisor to HMS Income Fund – another business development company that is not publicly-traded.

For Main Street Capital Corporation, this is beneficial in two ways. First, the BDC receives a substantial boost in revenues. MAIN receives 50% of the investment advisor’s base management fee and incentive fees. This equates to 1% of total assets.

Secondly, Main Street Capital Corporation does not see a material increase in its operational costs by taking on outside clients. Increasing revenues while holding expenses fixed will result in higher net income and stronger shareholder returns.

To conclude, Main Street Capital Corporation has expertise in the lower middle market of its industry and has a budding asset management business that enables it to have strong operational leverage. These factors will drive the BDC’s growth for the foreseeable future.

Competitive Advantages & Recession Resiliency

As an investment manager, Main Street Capital Corporation’s main competitive advantage comes from the talent it employs to source and fund deals.

The company’s senior management team has been largely unchanged since inception. The company’s CEO, Vince Foster, has been in place since the 2007 IPO and worked for the predecessor of Main Street Capital Corporation previously.

A similar level of longevity is seen across MAIN’s senior executive team. Main Street Capital Corporation also has a cost-based competitive advantage. As an internally-managed private investor, MAIN generates substantially lower operating expenses than its externally-managed counterparts, which helps improve net income.

As mentioned, Main Street Capital Corporation also has a durable competitive advantage due to its unique expertise in the lower middle market private debt & equity segment. This segment is generally too small for commercial banks to lend to, but too large for the small business representatives of retail banks to lend to.

By putting money to work in this unloved group of private companies, MAIN can realize outsized returns compared to its larger commercial bank counterparts. The lack of competition in the lower middle market means that Main Street Capital Corporation can often invest at valuations unheard of in the public markets (4.5x-6.5x EBITDA is cited by MAIN on their Investor Relations page).

Finance companies and asset managers are often vulnerable to recessions since investors are likely to pull their money to cut losses when financial markets are in distress. With that said, MAIN invests in private deals and lacks the same type of liquidity as, say, a mutual fund. Thus, Main Street Capital Corporation is expected to be moderately recession-resilient.

Although Main Street Capital Corporation came public shortly before the last recession, the company performed well during this difficult operational period:

Net-investment-income-per-share 2007 – $0.76 Net-investment-income-per-share 2008 – $1.15 (51% increase) Net-investment-income-per-share 2009 – $0.92 (20% decrease) Net-investment-income-per-share 2010 – $1.16 (26% increase) Net-investment-income-per-share 2011 – $1.69 (46% increase) Net-investment-income-per-share 2012 – $2.01 (19% increase)The company’s financial results were also impressive from the perspective of distributable net income:

Distributable-net-investment-income 2007 – $1.10 Distributable-net-investment-income 2008 – $1.44 (31% increase) Distributable-net-investment-income 2009 – $1.50 (4% increase) Distributable-net-investment-income 2010 – $1.50 (no change) Distributable-net-investment-income 2011 – $1.56 (4% increase) Distributable-net-investment-income 2012 – $1.71 (10% increase)While Net-investment-income-per-share declined from 2008 to 2009, Main Street Capital returned to growth the following year. More importantly for income investors, distributions have generally increased save for flat distributions in 2010.

Net-investment-income-per-share declined 4% in 2019, but distributions grew 2%. During the next recession, MAIN will benefit from its conservative capital structure. Investors should also note that the company had no debt maturing in 2017 or 2018, which gave the company flexibility during this time. All said, Main Street Capital Corporation appears fairly recession-resistant.

Valuation & Expected Total Returns

Main Street Capital grew net investment income 8% annually from 2009 to 2019. Conservatively, we expect net investment income to grow at 4% annually through 2025.

Over the past decade, Main Street Capital has traded with an average price-to-net-investment-income ratio of 15. Based off of the current share price and expected net-investment income of $2.47, the stock has a valuation of 15x net-investment-income.

Therefore, valuation isn’t expected to be factor in total returns over the next five years. The high dividend yield is expected to account for the bulk of Main Street’s total returns, with a smaller contribution from NII-per-share growth.

Expected total annual returns are as follow:

7.9% dividend yield (includes supplemental dividends) 4% net-investment-income growthWe expect that shares of Main Street Capital can offer a total annual return of 11.9% through 2025.

Final Thoughts

Although Main Street Capital Corporation is off-the-radar for most dividend growth investors, this BDC has a strong history of delivering substantial shareholder returns.

The firm’s strong track record of superior investment management and expertise in the lower middle market segment give it a strong competitive advantage in the private equity and debt industry.

Further, Main Street Capital Corporation is exceptionally shareholder-friendly. The stock’s high yield and monthly dividend payments might be suitable income investors.