Published on March 11th, 2020 by Josh Arnold

Investors that are interested in owning stocks for income can find it easy to be drawn to Real Estate Investment Trusts, or REITs. These stocks offer investors the chance to own a piece of a trust that leases out properties and passes essentially all of its earnings back to shareholders in the form of dividends.

Realty Income (O) has a nearly 4% dividend yield, and an extraordinary dividend history. And, Realty Income pays its shareholders monthly instead of quarterly, which affords investors faster compounding of wealth.

There are only 58 companies that pay monthly dividends. You can download our full Excel spreadsheet of all monthly dividend stocks (along with metrics that matter like dividend yield and payout ratio) by clicking on the link below:

This article will discuss Realty’s business model, its growth prospects, and its dividend in detail.

Business Overview

Realty Income is a retail-focused REIT that has earned a sterling reputation for its dividend growth history. Part of its appeal certainly is not only in its actual payout history, but the fact that these payouts are made monthly instead of quarterly. Indeed, Realty Income has paid 595 consecutive monthly dividends, a track record that is unprecedented among monthly dividend stocks.

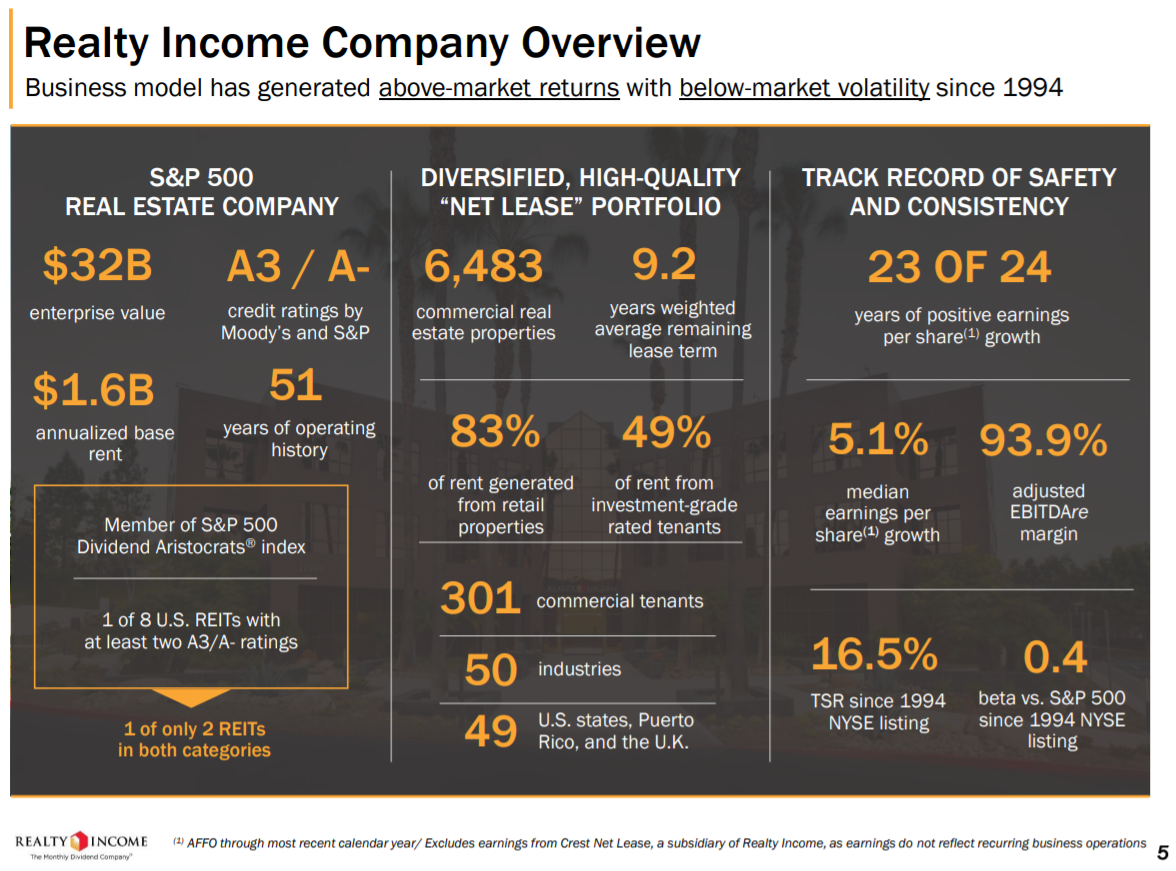

The trust owns almost 6,500 properties and has a market capitalization in excess of $25 billion. Realty Income focuses on standalone properties, rather than ones connected to a mall, for instance. That increases the flexibility of the tenant base, and helps the trust diversify its customer base.

{kind=link}

Source: Investor presentation, page 5

The trust has annualized base rent revenue of ~$1.6 billion and is one of only three REITs that can say it is a member of the Dividend Aristocrats, a group of 64 stocks in the S&P 500 Index with 25+ consecutive years of dividend increases.

Realty Income also has at least two A3/A- credit ratings. The company has built its impressive track record on sound financials, and that continues today, increasing the relative safety of the stock against other REITs that may have very high leverage.

The trust has 301 different commercial tenants across 50 different industries in nearly every state in the US. Importantly, it also has 23 years out of the last 24 where it generated positive earnings growth, which is not only outstanding, but has afforded it the ability to continually raise its dividend.

Realty Income reported fourth quarter and full-year earnings on February 19th. The trust reported total revenue of $398 million, up 16% year-over-year. Rents at existing properties rose, as they generally do, but acquisitions of new properties made up the majority of the increase. Funds-from-operations rose 29% on a dollar basis, but because the trust issued nearly $600 million in new shares, diluting shareholders, FFO-per-share rose 9% year-over-year.

Guidance for the year came in at FFO-per-share of $3.50 to $3.56, and our initial estimate is for the midpoint of that range at $3.53. That would represent 7% growth over 2019 results, which means 2020 is likely to be yet another year of growth for the REIT.

{kind=link}

Source: Investor presentation, page 13

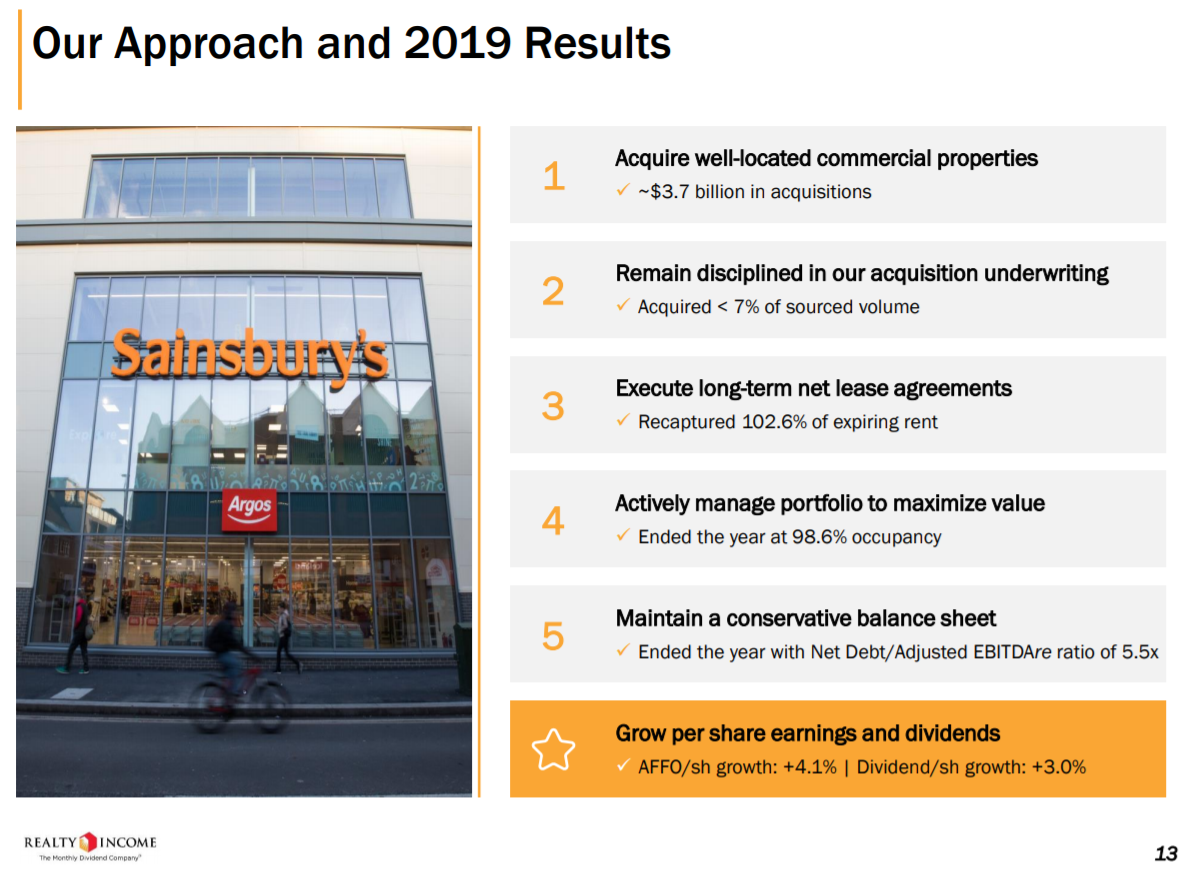

This slide highlights some of the key accomplishments the trust had during 2019, not the least of which was $3.7 billion in new properties, more than double the $1.8 billion of acquisitions made in 2018.

Apart from that, the trust managed to capture 102.6% of expired rent, keeping not only its occupancy rates high, but its average lease per square foot as well. Last year was another one in a very long line of periods with steady, predictable growth from Realty Income.

Growth Prospects

Realty Income’s growth has been quite consistent; the trust has a very long history of growing its asset base and its average rent, which have collectively driven its FFO-per-share growth. We don’t believe this has changed and thus, we see its growth capacity in the mid-single-digits annually, as it has been for many years.

Realty Income will achieve these results by simply continuing to do what it has always done.

{kind=link}

Source: Investor presentation, page 26

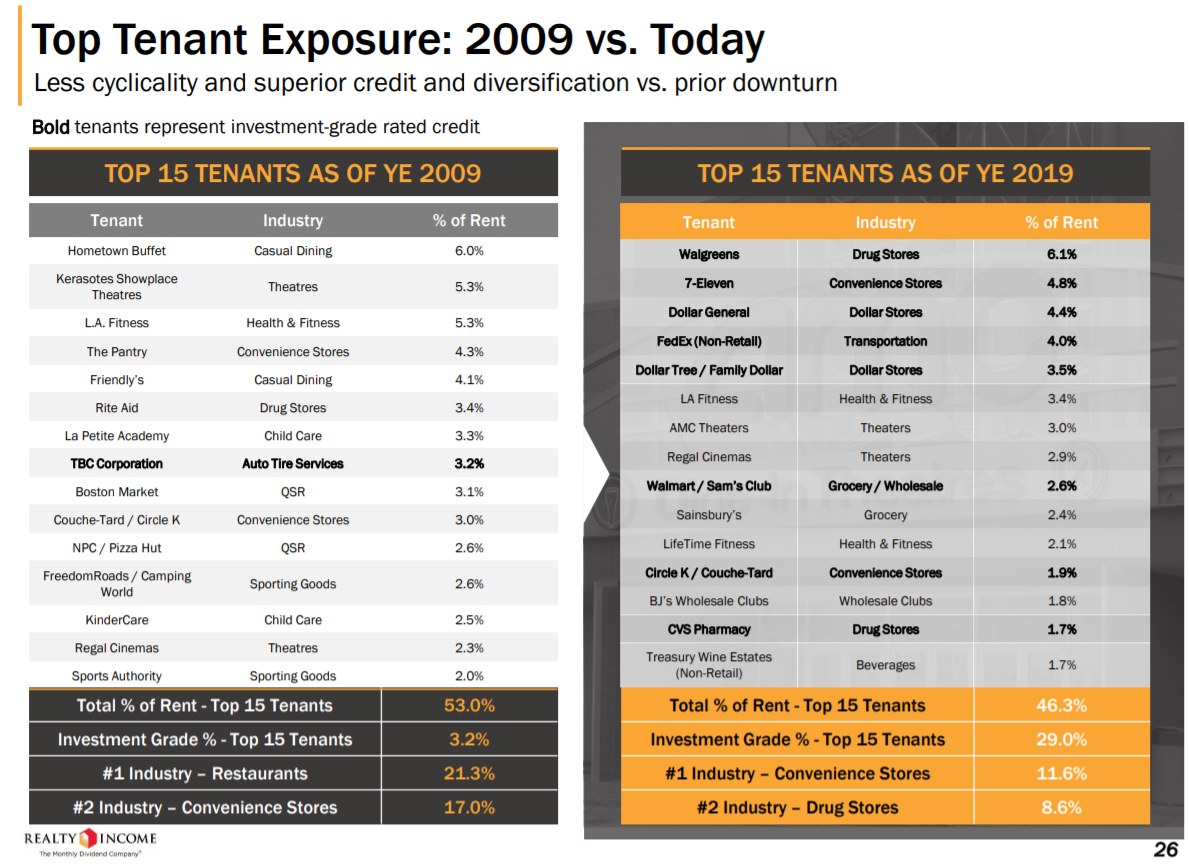

Realty Income has reduced its exposure to lower-quality tenants. In 2009, the trust’s investment grade tenants in the top 15 were just 3.2% of revenue and the trust was highly reliant upon restaurants, which are notoriously cyclical.

Today, 29% of its top 15 revenue comes from investment-grade tenants, and it has more than halved its reliance upon restaurants, favoring convenience stores and drug stores instead. Indeed, none of the top seven tenants in 2009 were investment-grade, but all of the top five are today as Realty Income has made an intentional push towards stronger tenants.

{kind=link}

Source: Investor presentation, page 20

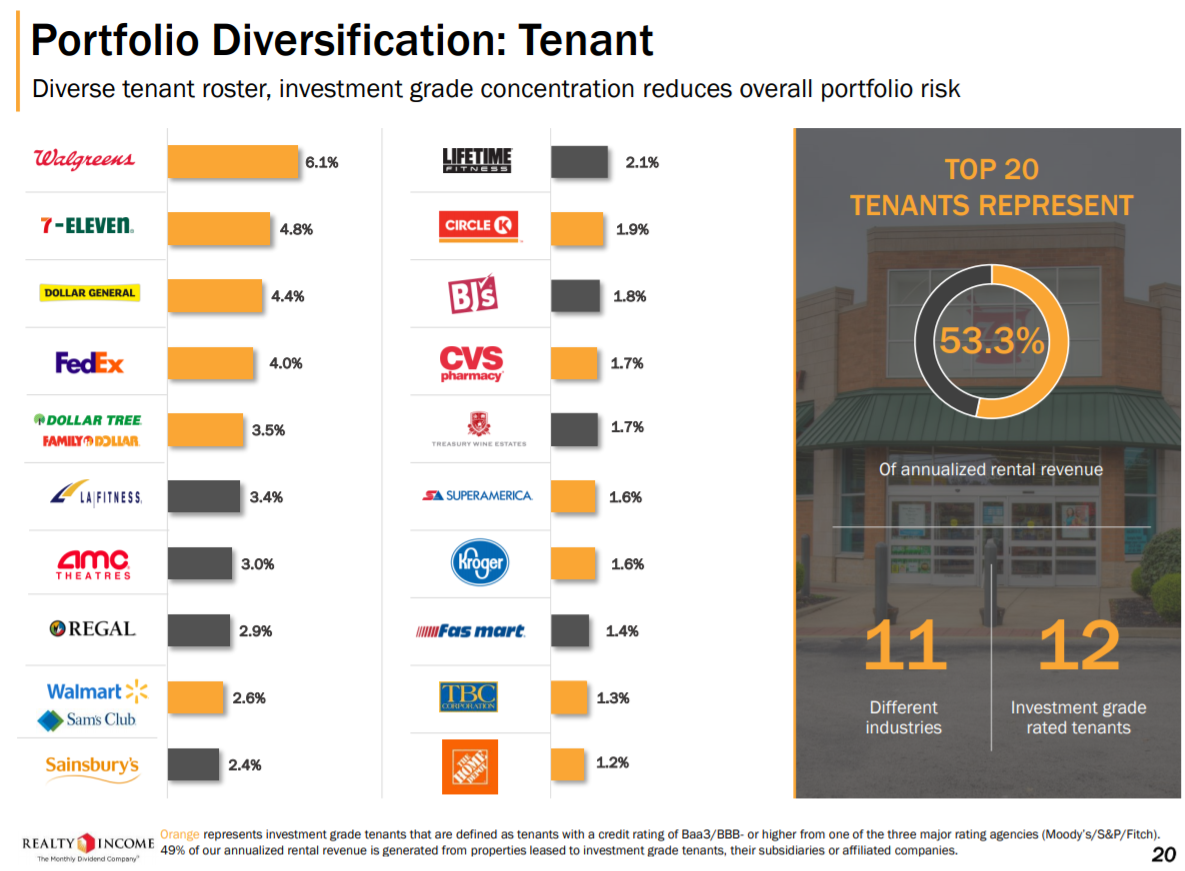

The trust’s list of tenants is a high-quality, diversified group where its highest exposure remains Walgreens (WBA), one of the largest drug retailers in the world. Even then, its largest tenant is just 6.1% of total revenue.

Its top 20 tenants represent 53.3% of revenue, but that group is from 11 different industries and 12 of them are investment grade rated. That is also a decline of nearly a percentage point from top 20 exposure last year.

In addition, 96% of its revenue is protected against e-commerce threats, meaning the rise of giants like Amazon (AMZN) shouldn’t have an outsize impact on its tenants results.

{kind=link}

Source: Investor presentation, page 23

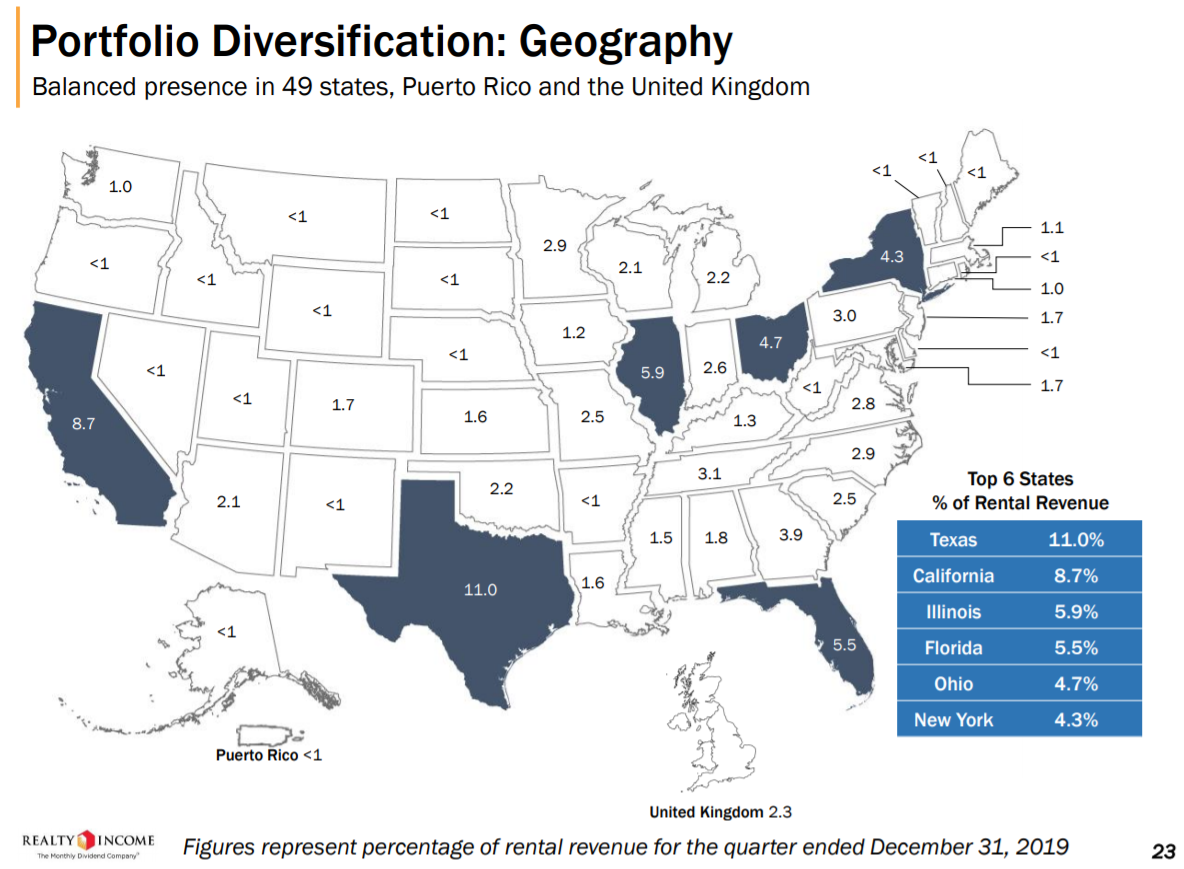

The same is true for its geographic diversification, which is outstanding. Realty Income’s highest concentration is Texas, but it is just 11% of revenue, down from 11.5% in 2018.

This diversification, like the industry composition, helps Realty Income reduce its risk from sector downturns, and allows it to capture growth over the long term.

{kind=link}

Source: Investor presentation, page 11

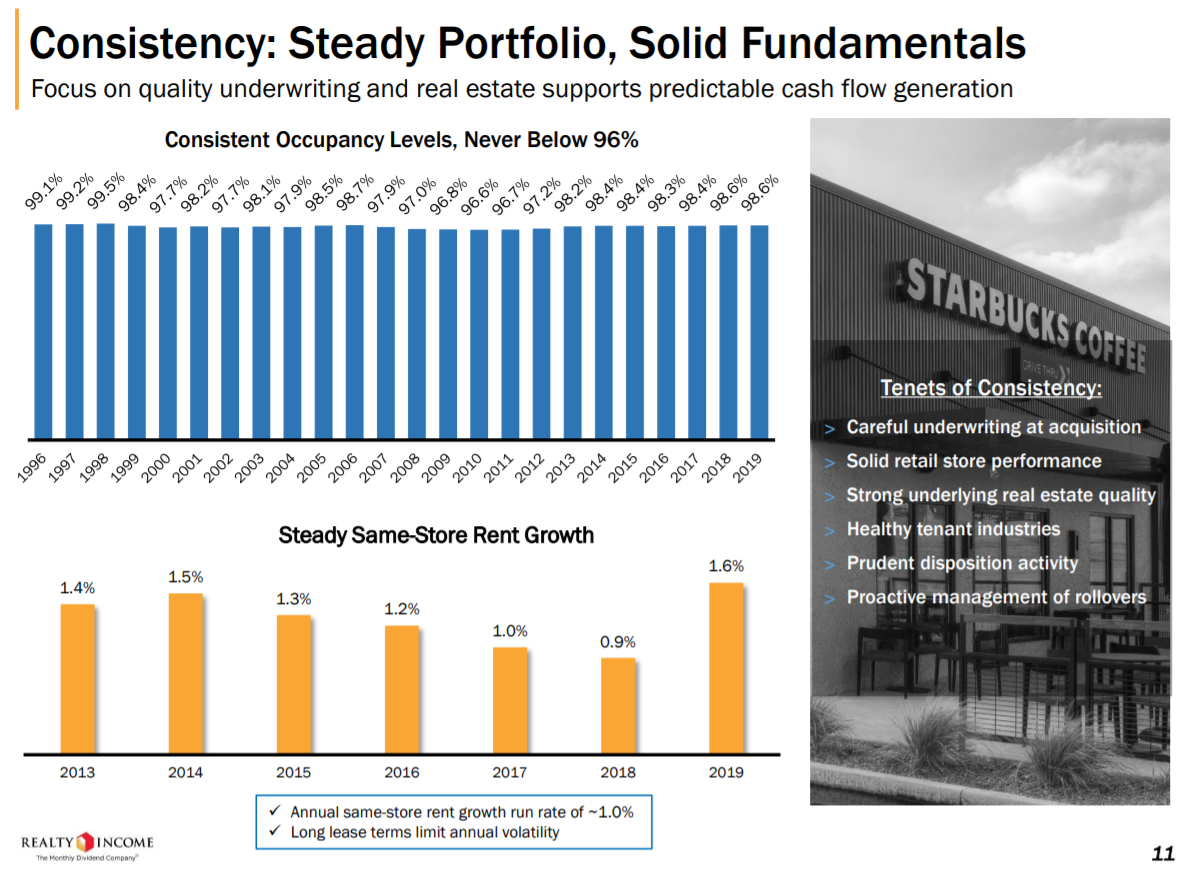

All of this has resulted in Realty Income’s results over time being truly outstanding. Occupancy has never been below 96%, which is an unbelievable track record of consistency as this period contains the dot-com bubble, as well as the financial crisis and the recessions that followed those events. Today, occupancy is nearly 99%, as it has been for two years now.

Same store rent growth has nearly always been positive as well, meaning Realty Income is capturing more revenue on its portfolio over time. Its long-term leases also afford it relatively low annual volatility in its rent terms. This helps with capturing higher base rents, which drives organic top line growth.

Putting all of this together, we see Realty Income as producing mid-single-digit FFO-per-share growth over time, consistent with its recent history.

Dividend Analysis

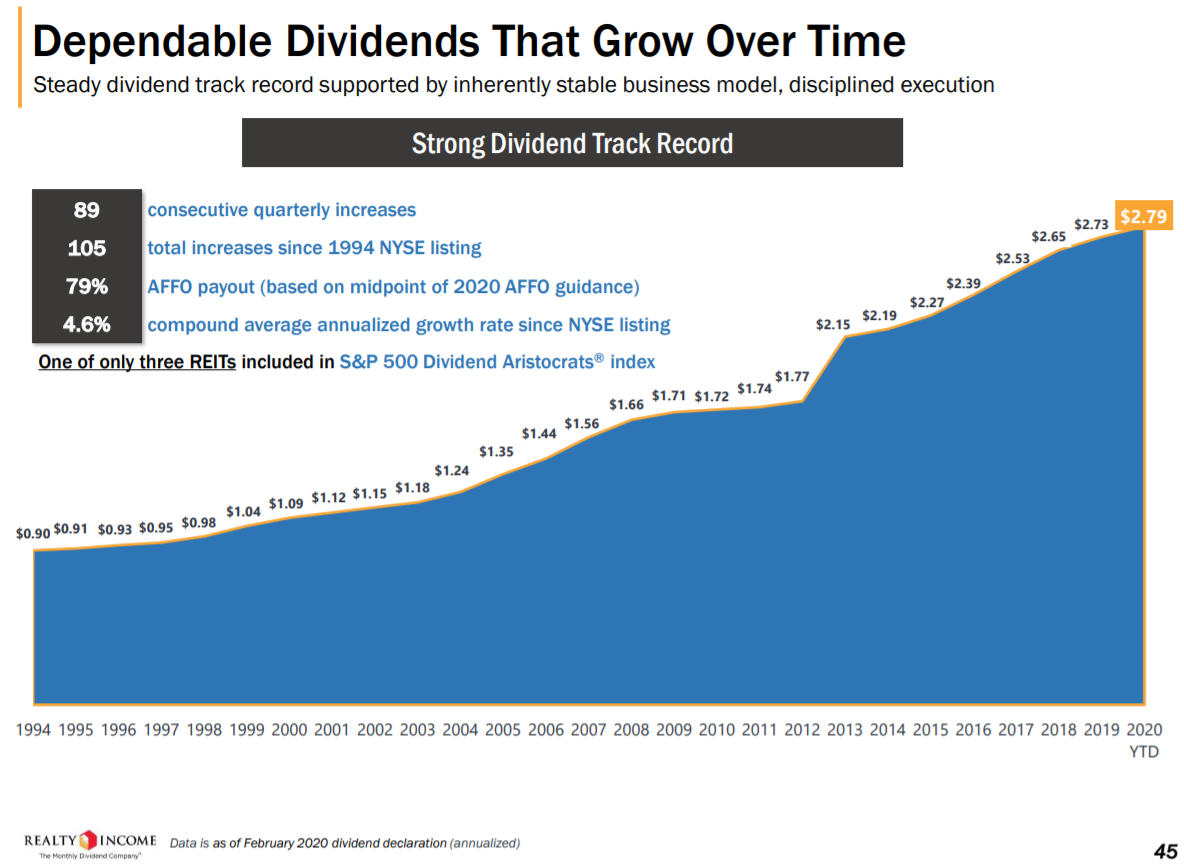

Realty Income’s dividend history is second-to-none in the world of REITs. Its dividend has been increased a total of 105 times since it came public in 1994, and it has been increased for 89 consecutive quarters as of today.

Most dividend stocks strive to increase their payouts annually; such a long streak of increases each quarter is much rarer.

{kind=link}

Source: Investor presentation, page 45

The dividend is also safe considering not only this extraordinary history of boosting the payout throughout all types of economic conditions, but also because the trust pays out just under 80% of adjusted FFO. REITs are required to pay out most of their income in the form of dividends, so Realty Income’s dividend payout ratio will never be low. We see ~80% of FFO as strong for a REIT, particularly for one that is growing FFO-per-share consistently.

That means that even if FFO-per-share were to go flat for some period of time, the dividend is still sustainable. We expect the payout to continue to rise in the low- to mid-single digits annually, as it has for so many years.

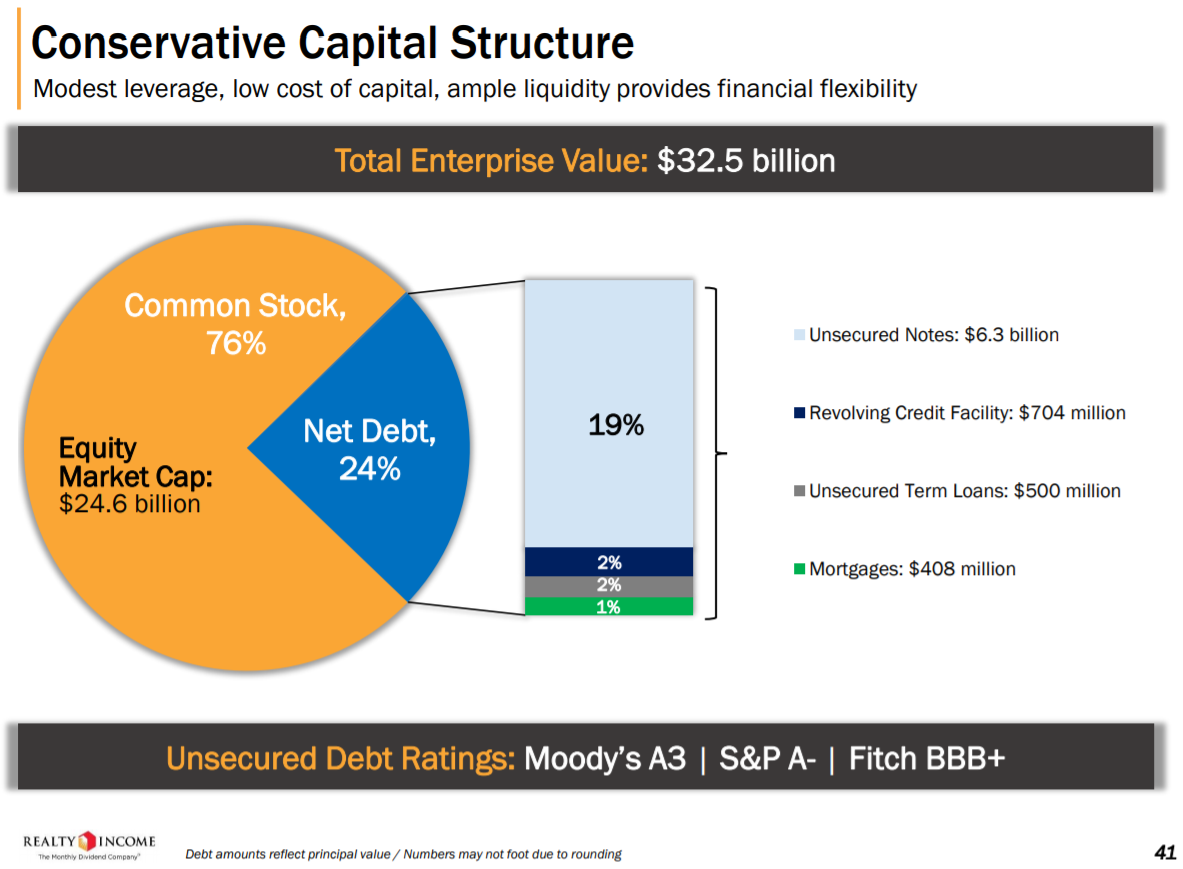

Realty Income is able to maintain this record not only because its business is fundamentally superior, but also because its capital structure is very conservative.

{kind=link}

Source: Investor presentation, page 41

The trust has strong, investment-grade ratings on its credit and it gets more than three-quarters of its financing from its common equity. This means that the trust spends relatively less on servicing debt and while dilution has been a minor headwind over time, the formula clearly works.

Realty Income doesn’t have major debt due until 2022 and 2023, when it will almost certainly refinance its obligations. In other words, liquidity and leverage aren’t concerns for Realty Income, adding to the allure of the stock for income investors.

In addition, the recent, sharp move lower in interest rates gives Realty Income and others the chance to refinance that debt before it becomes due at much lower rates. We see lower interest rates as a sizable positive for Realty Income, as it could lower its cost of funding over time.

Final Thoughts

REITs are favorites among dividend investors because they pay out the vast majority of their earnings to shareholders via dividends, which generally leads to high yields.

Realty Income’s 3.6% current yield is fairly low among REITs, but that is because the trust has a track record of success that is unrivaled. This leads to investors paying a premium for the stock, driving the yield lower.

However, for income investors looking for a yield that is twice the broader market and a secure payout, Realty Income fits the bill. This is not a growth stock, but from a pure current income and dividend growth perspective, Realty Income is difficult to beat.

The valuation is a bit high at ~22 times this year’s FFO-per-share, while we assess fair value at 18 times FFO. As a result, Realty Income’s elevated valuation could limit its total returns over the next several years. Even so, Realty Income is arguably the top monthly dividend stock in terms of business quality and dividend safety.