Updated on July 18th, 2019 by Bob Ciura

Income investors looking for high-quality dividend growth stocks should take a closer look at the consumer staples sector.

Of all market sectors, consumer staples (along with industrials) hold the highest number of Dividend Aristocrats, a select group of 57 stocks in the S&P 500 Index, with 25+ consecutive years of dividend increases.

There are currently just 57 Dividend Aristocrats. You can download an Excel spreadsheet of all 57 (with metrics that matter) by clicking the link below:

Consumer staples are household essentials—products that people can’t (or won’t) do without, even when the economy enters a recession. Think food, beverages, tobacco, and household products.

These are typically stable businesses that sell products people consume on a daily basis, which gives these companies pricing power and the ability to withstand recessions. Each stock mentioned in this article is on our list of 350 consumer staples stocks that pay dividends to shareholders.

You can download an Excel spreadsheet of all 350 dividend-paying consumer staples stocks by clicking the link below:

Not every stock in this article is a Dividend Aristocrat, but they all have higher dividend yields than the S&P 500 Index average, sustainable dividends, and expected returns of at least 10% per year.

The rankings in this article are derived from our expected total return estimates for every consumer staples dividend stock found in the Sure Analysis Research Database.

We filtered the list by focusing on stocks with a Dividend Risk Score of ‘C’ or higher. Further, we excluded one stock, Kraft Heinz (KHC), as we previously issued a sell recommendation on the stock after its dividend cut.

With that said, this article will discuss the top 7 consumer staples dividend stocks in our research database, ranked by expected annual returns over the next five years.

Table of Contents

The Kellogg Company (K) Kroger Company (KR) Molson Coors (TAP) Altria Group (MO) Walgreens Boots Alliance (WBA) Newell Brands (NWL) Imperial Brands (IMBBY)No. 7: The Kellogg Company (K)

Expected Annual Returns: 10.1%Kellogg was founded in 1906, the beginning of what would become a behemoth in the food processing industry. Kellogg has always focused on breakfast but in recent years, has also expanded to become an enormous snack producer. Its market capitalization is $20 billion, and it is due to produce just over $13 billion in revenue this year.

{kind=link}

Source: Annual Shareholder Meeting

Kellogg reported first-quarter results that showed a 3.5% year-over-year revenue increase. Growth was primarily attributable to the consolidation of the company’s Nigerian distributor, Multipro, which occurred in the same quarter last year. This more than offset the impact of negative currency translation. On an organic basis, revenue increased 0.3%.

Adjusted operating profit fell 7% thanks to higher input and distribution costs, as well as currency translation. Adjusted earnings-per-share fell 18% as the company grappled with the above factors, as well as a higher tax rate.

Kellogg intends to rejuvenate growth with a focus on new products and geographic markets. Kellogg has one of the bigger presences in the emerging markets within the consumer staples industry. Kellogg is selling its Keebler business for $1.3 billion, which should close in July. This will give the company additional resources to invest more aggressively in its growth initiatives.

Kellogg stock trades for a 2019 P/E ratio of 14.3, based on EPS expectations of $3.85 for this year. Our fair value estimate for Kellogg stock is a P/E ratio of 15, a reasonable valuation for a slow-growth consumer staples company. This would boost Kellogg’s annual returns by approximately 1% per year.

In addition to 5% expected EPS growth through 2024 and the current dividend yield of 4.1%, results in expected annual returns of just over 10% per year over the next five years.

No. 6: Kroger Company (KR)

Expected Annual Returns: 12.1%Kroger is the largest supermarket chain in the United States. It has almost 2,800 stores in 35 states and serves more than 60 million households every year. The stock has a market cap of $18 billion.

The industry dynamics are becoming more challenged for Kroger. The grocery industry is fiercely competitive, even more so after Amazon (AMZN) acquired Whole Foods for $14 billion.

Investors are concerned over the potential repercussions of the takeover. Amazon’s long-standing policy of offering lower prices than the established brick-and-mortar operators threatens to lower Kroger’s margins in an already low-margin industry.

However, in nearly two years of operating Whole Foods under Amazon, the actual impact on Kroger has been much less than initially feared. Nevertheless, the competition in the retail sector has heated more than ever. Amazon recently expanded the grocery delivery service of Whole Foods to more key regions in the U.S.

In addition, according to a recent reports, Amazon intends to open dozens of grocery stores across the U.S., with a lower price point and broader offerings than Whole Foods. Separately, Walmart (WMT) is expanding its online grocery delivery service to 100 metropolitan areas.

To counteract the competition, Kroger has invested heavily in its own growth initiatives, mainly lowering prices and increasing its digital footprint.

{kind=link}

Source: Investor Conference

Last year, it initiated a strategic plan called “Restock Kroger”, which aims to increase its operating income by $400 million until the end of 2020 by maximizing its efficiency and its cost savings.

On June 20th, Kroger reported first-quarter 2019 results. For the quarter Kroger reported $37.3 billion in sales, down from $37.7 billion in Q1 fiscal 2018, as a result of selling the company’s convenience store business. Total sales excluding this impact and fuel would have increased 2.0% compared to the prior year period. Adjusted earnings-per-share came in at $0.72 against $0.73 previously, as a 6% decline in net earnings was offset to a large degree by a much lower share count.

Kroger also raised its dividend by 14% shortly after reporting first-quarter earnings. This was a very strong raise and demonstrates Kroger management’s commitment to rewarding shareholders.

Kroger expects adjusted sales growth of 2.0% to 2.25%, and adjusted EPS of $2.15 to $2.25 for 2019. We expect that the retailer can grow its earnings-per-share by 5.0% per year over the next five years.

Due to the plunge of the stock after its earnings release, Kroger is trading at a very modest price-to-earnings ratio of 9.8, which is much lower than its 10-year average of 13.4. We maintain a fair value estimate of 12, acknowledging the low margins in grocery and the intense competition.

Still, if the P/E ratio expands to 12, shareholders would see a 4.1% annualized gain thanks to the expansion of its earnings multiple over this period.

In addition, Kroger stock has a 3.0% dividend yield after the recent dividend hike. Putting it all together, Kroger stock has expected annual returns of approximately 12.1% per year, a strong projected return for this stock. We also view Kroger as the top grocery stock to buy today.

No. 5: Molson Coors (TAP)

Expected Annual Returns: 13.6%Molson Coors Brewing Company was founded all the way back in 1873. Since then, it has grown into one of the largest U.S. brewers, with a variety of brands including Coors Light, Coors Banquet, Molson Canadian, Carling, Blue Moon, Hop Valley, Crispin Cider, and Miller Lite through a joint venture called MillerCoors.

Molson Coors, a $12 billion company by market capitalization, has a significant presence outside the United States. Its core international markets include Canada, Europe, Latin America, Asia, and Africa.

On May 1st, Molson Coors reported first-quarter financial results. The company advanced many of its strategic initiatives during the quarter.

{kind=link}

Source: Earnings Slides

For the quarter the company reported $2.3 billion in sales, representing a 1.2% decrease compared with the same quarter last year. This was driven by volume declines and foreign currency. Excluding currency, Molson Coors would have reported a 0.6% increase in sales.

Adjusted Net Income came in at $112.7 million, compared to $104.3 million previously, driven by positive net pricing and cost savings. Adjusted earnings-per-share came in at $0.52 compared to $0.48 in the prior year period, an increase of 8.3% year-over-year.

The company also said that it is committed to continuing to deleverage and reinstitute a dividend payout ratio of 20% to 25% of trailing EBITDA.

We expect the company to generate EPS of $4.80 in 2019. Based on this, the stock has a 2019 P/E ratio of 11.4. Our fair value estimate is a P/E ratio of 15, a reasonable starting baseline, taking into account the quality of the business and its potential growth rate.

Multiple expansion could generate 5.6% annual returns. In addition to 5% expected annual EPS growth and the 3% dividend yield, total returns are expected to reach 13.6% per year through 2024.

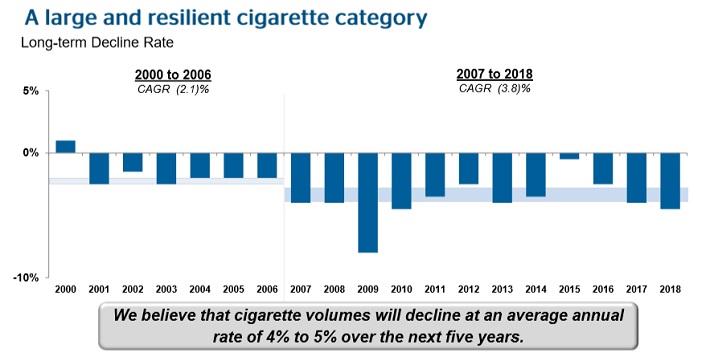

No. 4: Altria Group (MO)

Expected Annual Returns: 15.6%Altria is primarily a tobacco manufacturer. Its core brand is its flagship Marlboro cigarettes, which captures over 40% of U.S. retail market share. Altria has diversified itself in recent years, adding non-smokable brands Skoal and Copenhagen chewing tobacco, Ste. Michelle wine, and it also owns a 10% investment stake in global beer giant Anheuser Busch Inbev (BUD).

Related: The Best Tobacco Stocks Now, Ranked In Order

In late April (4/25/19) Altria reported first-quarter earnings. Revenue, net of excise taxes, declined 6.0% for the quarter, due primarily to falling shipment volumes. Adjusted earnings-per-share declined 5.3% for the first quarter.

Falling volumes pose a major challenge for Altria. U.S. consumers are increasingly quitting cigarettes, which means Altria needs to adapt to these changing consumer preferences. Altria expects the smoking declines to continue over the next several years at a mid-single-digit rate over the next several years.

{kind=link}

Source: 2019 CAGNY Presentation

The good news for investors is that Altria is investing heavily in arguably the two most important growth catalysts for tobacco companies: vaping, and cannabis. First, Altria made a $1.8 billion investment in Canadian marijuana producer Cronos Group. Altria purchased a 45% equity stake in the company, as well as a warrant to acquire an additional 10% ownership interest exercisable over the next four years.

Altria also invested nearly $13 billion in e-vapor manufacturer JUUL Labs for a 35% equity stake in the company, valuing JUUL at $38 billion. This was a huge investment, but JUUL has captured a huge market share lead in an increasingly-important growth category.

Altria remains a highly profitable company with positive EPS growth. Altria expects full-year adjusted diluted EPS to be in a range of $4.15 to $4.27 for 2019, which would be 4% to 7% growth from last year. This will sufficiently cover Altria’s dividend, with room for continued dividend growth.

The video below examines Altria’s dividend safety in detail.

Altria stock trades for a P/E ratio of 11.7, based on the midpoint of 2019 guidance. Our fair value estimate is a P/E ratio of 15, slightly below the 10-year average P/E ratio of 16.2. Still, we believe a mid-teens P/E is fair, given Altria’s high profitability and continued EPS growth.

The combination of multiple expansion (5.1% annual return), 4% annual EPS growth, and the 6.5% dividend yield result in total expected returns of 15.6% per year over the next five years.

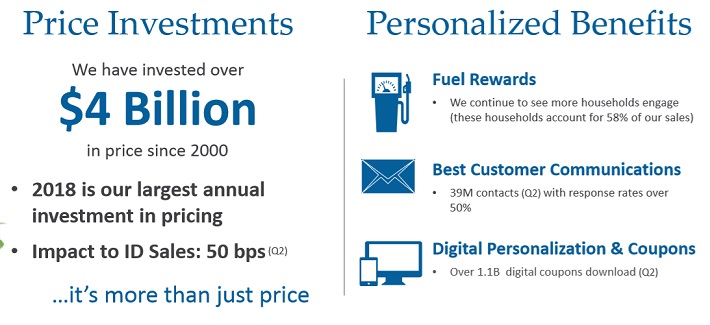

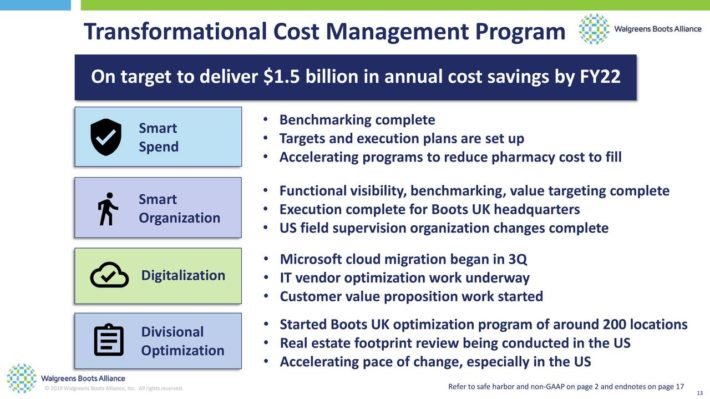

No. 3: Walgreens Boots Alliance (WBA)

Expected Annual Returns: 16.6%Walgreens Boots Alliance is a global pharmacy retailer and distributor. It operates over 18,500 stores in 11 countries. It also operates one of the largest global pharmaceutical wholesale and distribution networks in the world, with more than 390 centers that deliver to nearly 230,000 pharmacies, doctors, health centers and hospitals each year.

Walgreens is an especially attractive dividend growth company, as it has increased its dividend for over 40 years in a row. Walgreens is a member of the Dividend Aristocrats Index.

You can view a longer discussion of Walgreens’ dividend safety in the following video:

In late June, Walgreens reported financial results for its fiscal third quarter. Total sales increased 0.7% to $34.6 billion, while adjusted EPS declined 4%. Still, both metrics beat analyst expectations. Prescriptions increased 2% and revenue increased 1% for the quarter. In the core Retail Pharmacy USA business, organic sales increased 2.9%, thanks largely to a 6% increase in comparable pharmacy sales.

Outside the pharmacy business, Walgreens continues to struggle. Comparable retail sales fell 1.1% for the quarter, as the company continues to struggle in a broadly difficult environment for retailers. Investors are also concerned that the looming entry of Amazon into the healthcare industry could make trends deteriorate further.

However, Walgreens retains a significant competitive advantage. Consumers continue to demonstrate a desire for a brick-and-mortar store when it comes to health care, particularly since the U.S. is an aging population. Health care spending in the U.S. continues to increase faster than GDP, indicating strong demand for health care over the next several years.

Walgreens is investing in new digital capabilities, and to do so the company is aggressively cutting costs to keep profitability intact.

{kind=link}

Source: Investor Presentation

Walgreens should continue to pay, and even raise, its dividend each year going forward even if a recession occurs. Prescriptions and other health care supplies are a necessity, meaning consumers will still purchase these products even in an economic downturn. For evidence of this, consider that Walgreens increased its adjusted EPS from 2007 through 2010, during the Great Recession.

Based on expected EPS of $6.02, Walgreens stock has a 2019 P/E ratio of 9.1, which is significantly below our fair value estimate of 13.0. Expansion of the valuation multiple could fuel 7.4% annual returns, as will expected EPS growth of 6% and the 3.2% dividend yield. In all, we expect total returns of 16.6% per year through 2024.

No. 2: Newell Brands (NWL)

Expected Annual Returns: 19.2%Newell is a diversified consumer products manufacturer with brands across a wide variety of product categories. Its core brands include Rubbermaid, Oster, Sunbeam, Mr. Coffee, Ball, Sharpie, Paper Mate, Elmer’s, Yankee Candle, and Coleman.

The company is involved in a major turnaround, characterized by getting rid of legacy product categories that no longer offer satisfactory growth potential. There are many product categories that either have too low profit margins or are broadly seeing sales declines due to changing trends.

Newell’s turnaround strategy is to sell brands that are no longer deemed to be an important part of the company’s future direction, and reinvest the proceeds in new growth categories, paying down debt, and repurchasing stock.

For example, Newell sold the Waddington and Rawlings brands, as well as Goody Products. More recently, Newell sold its Pure Fishing and Jostens brands for $2.5 billion of after-tax proceeds. It also sold its Rexair and Process Solutions businesses for over $730 million. And, Newell recently sold its United States Playing Card Co., for an undisclosed sum.

Instead, Newell is focusing on its core brands in which it retains a leadership position.

{kind=link}

Source: Investor Presentation

The impact of these divestitures will reduce sales, but Newell can use the proceeds of the asset sales to reduce debt, buy back stock, and invest in new growth areas.

The company has made notable progress in these efforts. Newell reported Q1 earnings on 5/3/19 and results were stronger than expected. Total sales were $1.7 billion, down only slightly from the $1.8 billion from the year-ago period, due to a 3% decline in core sales.

Newell continues to expect a decline in sales in 2019, due to its various divestitures. Earnings-per-share came in at $0.14 on an adjusted basis, compared with $0.28 in the year-ago period. That said, the company reiterated its guidance for this year and as a result, we’ve kept our estimate at $1.60 in earnings-per-share for 2019. We expect 5% annual EPS growth for Newell over the next five years.

With a projected dividend payout ratio of 58% for 2019, we expect Newell to maintain its dividend, making it an attractive stock for income investors.

We believe Newell is also significantly undervalued. Using expected EPS of $1.60 for 2019, the stock trades for a P/E ratio of 9.5. Our fair value estimate is a P/E ratio of 14. Expansion of the stock valuation could fuel 8.1% annual returns for Newell stock through 2024.

In addition, Newell has a 6.1% dividend yield, resulting in total expected returns of 19.2% per year over the next five years.

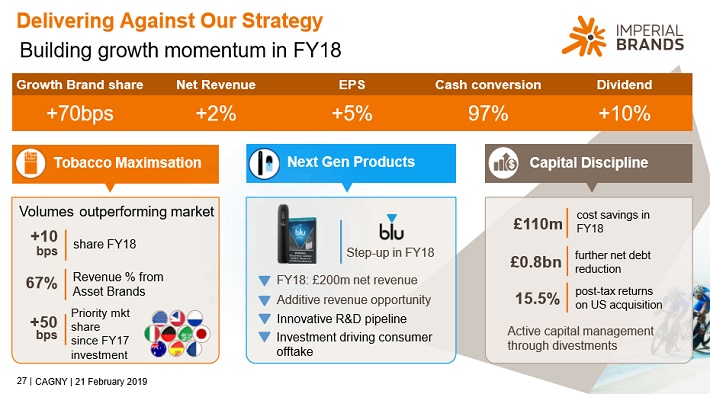

No. 1: Imperial Brands (IMBBY)

Expected Annual Returns: 20%+Imperial Brands is an international tobacco company with a market capitalization of $24 billion.

The company manufactures and sells a variety of tobacco products, including cigarettes, tobaccos, cigars, rolling papers, and tubes. Some of its core brands include Winston, Davidoff, Gauloises, L&B, Bastos, Fine, Gitanes, Kool, Jade, and others.

Imperial Brands reported first half of fiscal 2019 results on May 8th. Net revenue increased 2.3% as tobacco revenue grew 2.5% in constant currency. Imperial Brands was able to increase tobacco product prices by over 6%, which more than offset the impact of falling volumes.

Adjusted earnings-per-share declined 1.3% in constant currency as market loss in the e-cigarette category in the U.S. partially offset by cost cuts. Imperial Brands expects revenue growth of as much as 4% for this fiscal year.

The company’s over-arching strategy going forward is to maximize profitability in its core tobacco business, while achieving growth through its new products.

{kind=link}

Source: 2019 CAGNY Presentation

As a tobacco company, Imperial Brands is also fighting against changing consumer trends, specifically the falling smoking rate in many countries. Imperial Brands’ shipment volumes fell nearly 4% in 2018, and by 4.5% in the first half of the current fiscal year.

Like Altria, Imperial Brands is investing in new growth products as the industry shifts away from traditional cigarettes. Imperial Brands’ next-generation products include vapor and heated tobacco, such as blu. Thanks to price increases, share repurchases, and new products, we expect 3% annual EPS growth through 2024.

Imperial Brands is expected to maintain a dividend payout of $2.45 per share for 2019, which equals a high dividend yield of 9.4%. The dividend appears secure, with a projected payout ratio of 67% for 2019.

Imperial Brands stock trades for a P/E ratio of 7.1, based on expected EPS of $3.66 for 2019. Our fair value estimate is a P/E ratio of 11, which we believe to be fair value for a slow-growth company. Expansion of the P/E ratio could fuel 9.2% annual returns for shareholders, indicating that the stock is significantly undervalued.

In addition, the 9.4% dividend yield and expected EPS growth of 3% provides total expected returns of 21.6% per year. This makes Imperial Brands our top-ranked consumer staples stock in terms of expected return through 2024.