Published on March 11th, 2020 by Josh Arnold

Cruise line operators tend to see immense earnings-per-share growth during times of strong economic growth and as a result, their stocks can do very well during such periods. Of course, the reverse is true, and cruise line stocks can become very risky during times of economic distress, or other external factors, such as the recent coronavirus outbreak.

During the steady economic growth of the past decade, certain cruise line stocks gained the ability to return cash to shareholders through rapid dividend growth, making the group of stocks potentially enticing for income investors as well.

Two of the three major cruise line operators–Royal Caribbean Cruise Lines (RCL) and Carnival Cruise Lines (CCL)–pay dividends to shareholders. You can see our entire list of 664 dividend-paying consumer cyclical stocks here.

You can also download the full list of consumer-cyclical dividend stocks, along with important financial metrics like dividend yield and payout ratio, by clicking on the link below:

The third major cruise line operator, Norwegian Cruise Line Holdings (NCLH), does not pay a dividend.

The past few months have seen tremendous volatility in travel-related stocks. Valuations in travel-related stocks have come down significantly as of late. But this could mean the cruise line operators offer value at current prices, in addition to much higher dividend yields for Carnival and Royal Caribbean.

More information can be found in the Sure Analysis Research Database, which ranks stocks based upon the combination of their dividend yield, earnings-per-share growth potential, and changes in the valuation multiple to compute total returns.

Table Of Contents

The table of contents below provides for easy navigation of the article:

Norwegian Cruise Line Holdings (NCLH) Carnival Cruise Lines (CCL) Royal Caribbean Cruises (RCL) Final ThoughtsIn this article, we’ll take a look at the three cruise line stocks we have in our coverage universe and rank them according to their total return potential. Stocks are listed by five-year expected returns, in order of lowest to highest.

Cruise Line Stock #3 – Norwegian Cruise Line Holdings (NCLH)

Norwegian Cruise Line Holdings was founded more than 50 years ago as an alternative to the more structured cruises that were offered on other carriers. The company’s “freestyle” cruising has resonated well with consumers and today, it operates 28 ships that generate nearly $7 billion in annual revenue. Norwegian went public in 2013, but the recent decline in the share price lowered the market capitalization at less than $4 billion.

Norwegian reported fourth quarter and full-year earnings on February 20th, and results were very strong once again, but also noted some caution based on the coronavirus outbreak which is causing cancellations. Last year was quite good for Norwegian as it reported its sixth consecutive year of record revenue and earnings.

Total revenue was up 6.7% for the year to $6.5 billion, as the company saw stronger volumes and stronger yields. Gross yield rose 4.6% while net yield increased 3.6% on a constant-currency basis. Cruise operating expense increased 8.5% during the year as Norwegian increased its capacity days. Gross cruise costs per capacity day, which is a measure of comparable operating expenses, increased 6.3% in 2019. Fuel costs increased slightly for the year, rising from $483 to $491 per metric ton.

Earnings-per-share for 2019 came to $5.09, or $1.1 billion. The company entered 2020 with a record booked position and better average pricing, but Norwegian has already canceled 40 voyages in Asia, which we see as the just beginning of cancellations. Earnings estimates are moving down rapidly for the sector, and we are currently at $4.00 per share for this year as cruise operators face very strong headwinds from the coronavirus outbreak.

{kind=link}

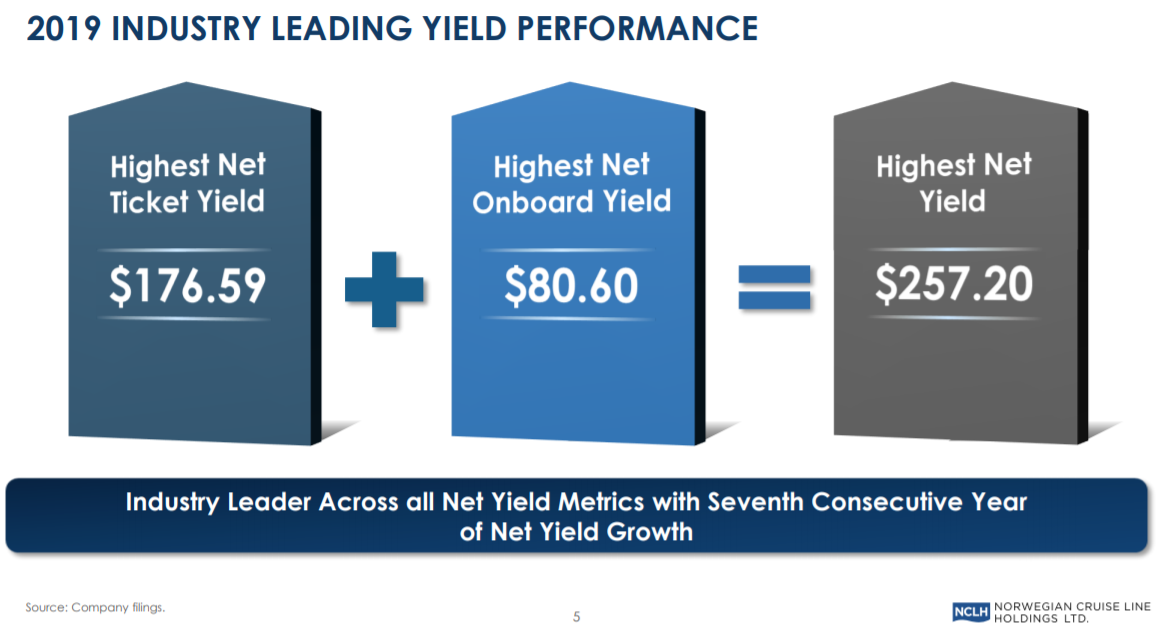

Source: Investor presentation, page 5

The above slide shows how Norwegian has been able to boost its margins over time, as it continues to see strong ticket pricing, as well as onboard spending. The company leads the industry with combined net yield of $257 per available cruise day, which affords it operating leverage on its fixed costs as the top line rises over time. With nine new ships in the pipeline, we expect this will continue to rise once the impact of coronavirus has abated. We note there is no timeline for mitigation of coronavirus, but long-term, Norwegian is a very strong operator.

We see 8% earnings-per-share growth annually over the next five years, as Norwegian should continue to grow its capacity. We see new ships as a driver of revenue and margin growth, as they offer more room capacity and ways to boost onboard spending, but also operate more efficiently, which lowers costs. Fuel costs and currency translations are concerns for Norwegian but given the strong booking volume and pricing we’re seeing, high-single digit earnings-per-share growth is very achievable over the long-term.

Obviously, Norwegian is suffering from coronavirus impacts, and may for quite some time as travelers may be unwilling to return to cruise line operators, even after the threat has passed. We’ve drastically lowered our earnings-per-share estimates for this year as a result, and investors should closely monitor the situation.

Norwegian’s price-to-earnings ratio has varied quite a bit since it came public several years ago but today, we see the stock as offering new investors significant value. Shares trade for just 5.8 times this year’s depressed earnings estimates, comparing extremely favorably against what we see as fair value at 9.5 times earnings. That implies a strong 10.3% tailwind for annual total returns from a rising price-to-earnings over a five-year period. Norwegian has never had a valuation this cheap, so even with the current threat of coronavirus, we find significant value in shares today.

We see Norwegian as the weakest of the three cruise line operators in terms of total returns, but weakness is relative in this case. Because of the extreme undervaluation, Norwegian offers investors 19.2% projected annual total returns, even with depressed earnings and valuation estimates, respectively.

Cruise Line Stock #2 – Carnival Cruise Lines (CCL)

Carnival Cruise Lines was founded in 1972 when it began as a small cruise ship operator. The company has been publicly traded since 1987, starting what has become a long tradition of using shareholder capital to acquire other cruise lines. Today, it has 9 different brands that generate about $21 billion in annual revenue and the stock has a $16 billion market capitalization after a huge selloff in shares due to coronavirus concerns.

Carnival reported fourth quarter and full-year earnings on December 20th and results were well in excess of consensus estimates for 2019. Carnival cut guidance earlier in the year, which subsequently allowed it to exceed that guidance. The company faced weather-related cancellations and weak demand from Europe in 2019, and its operating metrics were weaker than Norwegian and Royal Caribbean in many ways.

Gross revenue yields rose 4% in Q4, but net revenue yields in constant currency declined 1.8%. Guidance was for -2% to -3%, so the company was able to beat that, but results were still somewhat weak compared to peers. Gross cruise costs including fuel per available day were up 6.9%, but the net cost in constant currency rose just 2.6%, more closely matching yield growth. The company also saw a boost in earnings from fuel prices and currency exchange, which is somewhat unusual as those items typically detract from earnings.

Full-year earnings came to $4.40 per share, up from $4.26 in the prior year and exceeding guidance. Carnival was bullish on 2020 at the time of the earnings release, and is set to release Q1 earnings in the coming weeks, where we believe the company will be much more cautious thanks to coronavirus. Booking trends were strong heading into the year and the company forecast 5% revenue growth for 2020, but we believe this number will need to come down significantly.

With the impact of coronavirus still unknown, our current estimate for earnings-per-share for 2020 has declined from $4.50 to $4.00 just since December, and we reiterate that the situation is fluid and may require additional reductions in estimates in the coming months.

To that end, we have cut our annual earnings-per-share growth estimate for the next five years from 8.5% to 4%. Carnival will be able to achieve such growth via a combination of continued higher booking volumes and pricing, as well as margin expansion. We see reason for caution given the coronavirus situation, as well as the fact that operationally, Carnival is the weaker of the three major cruise line operators.

Principal risks include foreign exchange and fuel, which we already mentioned as well as potential overcapacity in the industry as a whole. With global cancellations on health concerns, overcapacity could become a significant problem for Carnival and lead to lower pricing and margins. Forex and fuel costs are always risks for cruise line operators so that is not unique, but it certainly bears watching for shareholders. Overall, however, we believe Carnival still has a bright future, with a very uncertain near-term outlook.

Carnival’s dividend has grown at very high rates since 2014 as the company’s improving profitability has allowed it to increase cash returns to shareholders. This kind of growth in the dividend isn’t realistic to continue moving forward but we do think the payout will rise to about $2.55 per share by 2025, affording investors robust growth in the dividend.

CCL’s price-to-earnings ratio had been reasonably stable in recent years but today, it stands at just 6.1 times earnings due to the selloff related to voyage cancellations. That stands extremely favorably against what we see as fair value of 10 times earnings, implying a huge 10.3% tailwind to total annual returns as the price-to-earnings ratio expands over time. We note 10 times earnings is down significantly from our prior forecast of 16 times earnings, but we feel this level of caution is warranted today.

Carnival stock is also a very strong choice for those seeking income. Today’s yield is in excess of 8%, which is extraordinary. Overall, Carnival looks attractive here for a variety of investors as we see 19.8% total annual returns moving forward. The stock should achieve these returns via a combination of the current 8.2% yield, a 10.3% annual tailwind from a rising price-to-earnings ratio and 4% earnings-per-share growth.

The recent selloff has boosted the current yield of the stock as well as the value it represents, given the lower price-to-earnings ratio. Even accounting for an uncertain growth outlook, Carnival appears to be undervalued.

Cruise Line Stock #1 – Royal Caribbean Cruise Lines (RCL)

Royal Caribbean Cruises was founded in 1969 and since that time, has grown into six different brands that have 40 cruise ships in service. It also has joint venture interests in another 21 ships, with 17 more on order as it continues to modernize its fleet. Royal Caribbean is the second-largest cruise operator in the world and services six different continents. The stock has a $9.2 billion market capitalization after the brutal coronavirus-related selloff.

Royal Caribbean reported fourth quarter and full-year earnings on February 4th, and results were outstanding, as the company produced another year of very strong growth.

{kind=link}

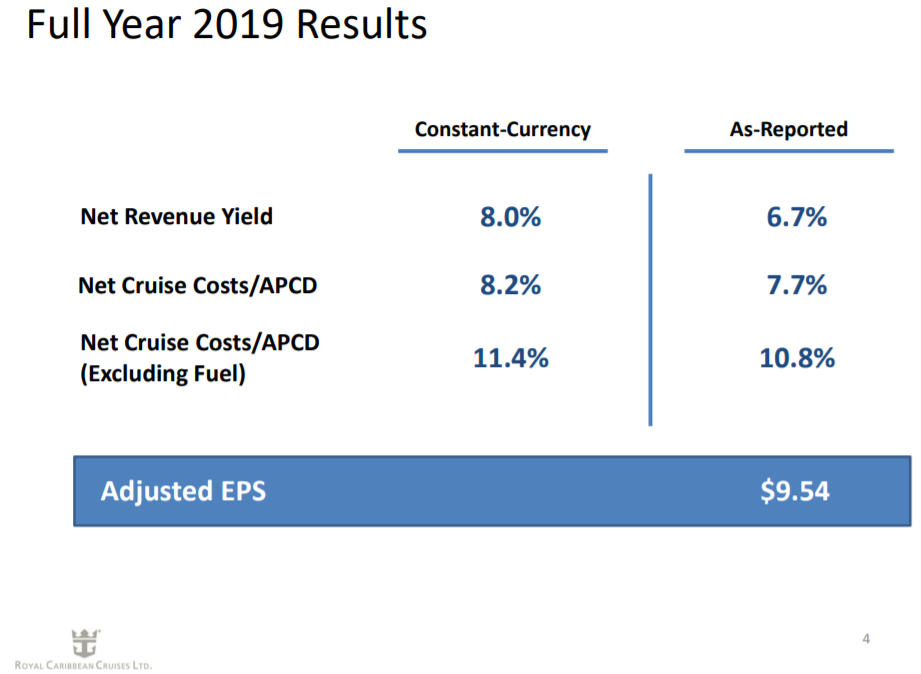

Source: Investor presentation, page 4

Gross yields rose 8.2% in constant currency, while net yields increased 8.0%. Gross cruise costs per available passenger day, which is a way to measure comparable costs year-over-year holding capacity constant, were up 8.7% in constant currency. Excluding fuel, that number rose 11.4%, so Royal Caribbean saw a sizable increase in operating costs in 2019.

Earnings came to $2 billion, or $9.54 per share on an adjusted basis. These were gains from 2018 levels of $1.9 billion and $8.86, respectively, as Royal Caribbean produced another record year. Early guidance from the company suggested $10.40 to $10.70 in earnings-per-share for 2020, noting that guidance didn’t include any coronavirus impacts.

However, the company subsequently withdrew guidance for this year as it is grappling with the negative impacts of coronavirus-related cancellations and costs. Our estimate at this point is for $8.75 in earnings-per-share, but we note that earnings estimates for any travel-related stock are subject to immense volatility at this point. Management itself is not able to provide a reliable earnings estimate at this time.

Separately, Royal Caribbean announced recently its 20>25 by 2025 plan, which includes reducing its carbon footprint by 25%, as well as producing adjusted earnings-per-share of $20 in five years’ time. Obviously, we see the latter as quite challenging given the setbacks the company is facing from coronavirus, but management is obviously positive on its long-term future. While we also believe Royal Caribbean has a bright future, investors should note that the short-term will see strong headwinds from coronavirus.

Royal Caribbean’s earnings-per-share have more than quadrupled since 2012 – even with the expected decline for this year – a very impressive growth rate. There is a significant risk associated with cruise line operators when recessions strike and Royal Caribbean certainly isn’t immune to that threat, but we see the industry – and Royal Caribbean – as having a bright outlook for the foreseeable future.

We are forecasting 8% earnings-per-share growth for Royal Caribbean over the next five years, as it has meaningful tailwinds. Fuel costs and currency exposure are common risks for cruise line operators and Royal Caribbean carries those risks. Royal Caribbean hedges about 50% of its fuel costs so volatility will be lower from that factor, but currency swings can impact results positively or negatively at any given time depending upon where the US Dollar trades.

Separately, Royal Caribbean is positioned for growth ahead as it has more than a dozen new ships coming into service over the next several years. This will afford the company not only increased capacity, but also the higher yields that new ships bring as well. New ships are more efficient to operate than older ships, and customers will pay more per room, meaning margins should rise over time in addition to rising revenue.

The dividend has grown at very high rates in recent years and while we cannot expect the same rates of growth going forward, we do see the payout at $4.58 in five years, keeping the payout ratio around 30% of earnings on a normalized basis. The payout ratio will be higher this year as earnings decline. This gives Royal Caribbean an element of dividend growth in addition to its robust earnings-per-share growth potential.

Royal Caribbean’s price-to-earnings ratio has fallen significantly recently, along with the rest of the industry. This has resulted in the stock being tremendously undervalued at present, providing what we believe is an opportunity for longer-term investors that can handle the inherent risk of owning a travel-related stock at this point. The current price-to-earnings ratio of 5.9 compares quite favorably to our fair value estimate of 12 times earnings. That could produce an enormous 15.2% tailwind to annual total returns over a five-year period, due to the rising valuation multiple.

In our view, the coronavirus selloff has created a stock that is significantly undervalued with an enormous dividend yield as well. We note the coronavirus situation may cause Royal Caribbean to slow or stop its dividend growth temporarily depending upon how deep the impact ends up being, but the dividend appears secure due to sufficient underlying earnings-per-share.

Overall, Royal Caribbean looks best-positioned for strong total returns in the coming years. We are forecasting total annual returns of 27.5%, consisting of the current 6% yield, 8% earnings-per-share growth and a 15.2% tailwind from a rising price-to-earnings ratio.

Final Thoughts

The extremely high projected rate of return for the three major cruise line stocks assumes a return to normalized operations over the long-term. Future returns are also based on their depressed valuation multiples, which could see upside if the coronavirus outbreak is contained sooner rather than later.

Of course, there is no guarantee that this will happen in the near-term. As a result, investors should expect continued volatility in the major cruise line stocks. These cruise line stocks could be strong investments based on their discounted valuations if they can return to growth, but investors will need to exercise patience.

We recommend investors hold a long-term view when considering cruise line stocks. Given all of these factors, we think Royal Caribbean is the best cruise line operator stock today for long-term income investors.