Published on July 12th, 2019 by Josh Arnold

UnitedHealth Group (UNH) traces its beginnings to 1974, when a group of physicians and other health care professionals founded Charter Med Incorporated.

UnitedHealth went public in 1984 at a split-adjusted price of just 14 cents; shares have thus returned an eye-popping 175,000% to original shareholders.

UnitedHealth has not only been one of the great growth stories in the market in the past thirty years or so, it is also now a constituent of the highly regarded Dow Jones Industrial Average.

UnitedHealth’s share price suffered somewhat at the beginning of 2019 due to some political chatter regarding universal health care in the US. Shares have since rebounded and are trading near the middle of the year-to-date range.

However, we think the company’s growth trajectory and the current share price still represent a compelling combination of growth and value, and we continue to like UnitedHealth for that reason.

This, combined with very strong dividend growth prospects, has us continuing to recommend UnitedHealth as a buy.

Business Overview

UnitedHealth trades for a current market capitalization of $234 billion, and operates in two segments: UnitedHealthCare and Optum. The former is a global health care benefits provider, serving individuals and employers, as well as Medicare and Medicaid beneficiaries.

UnitedHealthCare focuses on improving the quality of care received, as well as reducing costs and simplifying the health care experience. This segment produced $48.9 billion in revenue in the most recent quarter.

Optum is a health services business that serves a global client base, including payers, providers, employers, governments, and individual consumers. Optum has similar goals to UnitedHealthCare in that it seeks to reduce costs and improve the value of health care and the consumer experience. Optum produced $26.4 billion in revenue last quarter.

UnitedHealth reported Q1 earnings on 4/16/19 and results beat expectations. However, cautious commentary from the company’s management team soured investor sentiment, and shares traded sharply lower following the report.

The quarter saw revenue up 9% year-over-year to $60.3 billion as UnitedHealthCare produced a 7.6% gain in revenue, while Optum increased 11.7%. Premiums were up 7.8% to $47.5 billion, while products were up 20.4% to $8.1 billion, and services increased a more modest 5.2% to $4.3 billion.

Overall, UnitedHealth’s revenue in Q1 looked much like it has for years; the company continues to produce very high rates of growth despite its already-massive scale.

Indeed, UnitedHealth has managed to be a growth company over the years, irrespective of how large it has become, which is a natural barrier to further growth for most companies. Q1’s revenue growth, however, showed once again UnitedHealth isn’t slowing down.

Earnings were up 22.4% on a dollar basis and up 22.7% on an adjusted earnings-per-share basis, coming in at $3.73 in Q1. The gain was primarily attributable to higher revenue, but UnitedHealth also saw 60bps of margin expansion due to continued operating leverage gains. The company’s continuously higher revenue has afforded it the ability to leverage down its operating costs over time, and that occurred again in Q1.

The company is guiding for adjusted earnings-per-share this year of $14.50 to $14.75; our estimate is now $14.70.

Comments from the CEO about universal insurance in the US, which hasn’t gained serious legislative traction just yet, sent the stock lower, as mentioned. He said such a policy would cause a “wholesale disruption” in American healthcare, and given UnitedHealth’s entrenched – and very profitable – spot in that healthcare system, comments weren’t received well by investors.

While we see any disruption to the current model as a likely negative for UnitedHealth, we also note that no such proposal has any sort of meaningful chance at becoming law anytime soon. Thus, we believe investors overreacted in essentially ignoring the terrific Q1 report and instead focusing on something that isn’t necessarily even on the horizon.

Apart from terrific earnings growth, UnitedHealth continues to boost its dividend at very high rates. The company recently raised its dividend from $3.60 annually to $4.32 annually, an increase of 20%. UnitedHealth’s outstanding growth in earnings over the years has afforded it the ability to continue to raise its dividend at high rates without undue stress on its financials, and it has done so again.

We expect continued, strong growth in the payout in the years to come as we believe UnitedHealth will continue its run of double-digit dividend increases for the foreseeable future.

Growth Prospects

UnitedHealth has managed to grow its earnings-per-share at an average annual rate of nearly 16% since 2009. That sort of earnings expansion is very difficult to find, particularly in a large cap stock like this. We certainly don’t think UnitedHealth’s run of growth is done by any means, but we do see growth slowing somewhat to 9% annually.

The three main drivers of the company’s earnings-per-share growth will be revenue, margins, and share repurchases.

{kind=link}

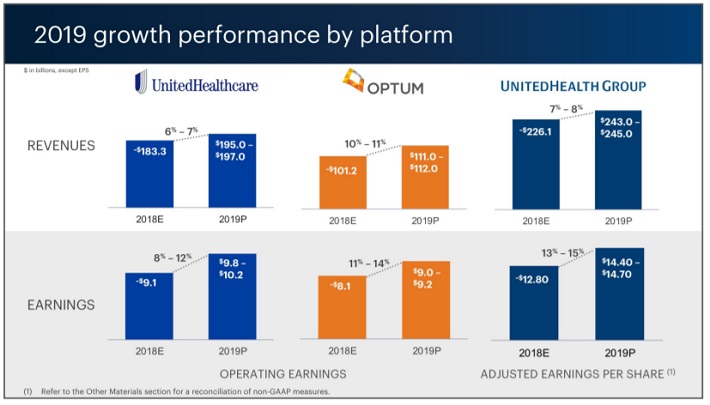

Source: Investor presentation, page 3

Indeed, those factors combined to produce the very strong growth outlook pictured above as both of the company’s segments are expected to perform very well again this year. Revenue alone is projected to be in the 7% to 8% growth range, assuming 6% to 7% for UnitedHealthCare and 10% to 11% for Optum.

Given the company’s ever-growing customer base and strong pricing, we see revenue growth as the primary driver of earnings expansion in the years to come, as it has been in past years.

Margin expansion should continue to accrue as well given that rising revenue provides the company operating leverage. UnitedHealth’s expenses don’t necessarily rise at the rate of revenue and thus, higher revenue totals are spread over a relatively smaller expense base. This improves margins over time and is incrementally positive to earnings-per-share.

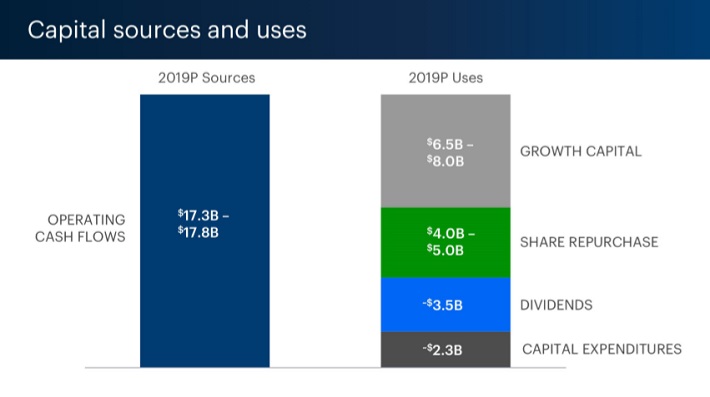

Finally, UnitedHealth has been a serious capital return story for some time, not only with its dividend, but buybacks as well.

{kind=link}

Source: Investor Presentation

Given the much higher share price, the company’s buyback will not be as effective as it was in past years in terms of reducing the float.

However, we think it can add a low single digit tailwind over time to the company’s earnings-per-share growth, over and above revenue and margins.

In short, while UnitedHealth has experienced tremendous earnings growth over its long history, the factors that produced that growth are still very much in place, and we see the future as bright.

Valuation & Expected Returns

Our estimate of $14.70 in earnings-per-share for this year implies a current price-to-earnings ratio of 16.7. That’s somewhat lower than what UnitedHealth has seen in recent years, and below our conservative estimate of fair value at 17.5 times earnings.

Together, these factors imply that UnitedHealth is reasonably priced at worst, and relatively cheap at best. Either way, we see the valuation as attractive today.

Combined with 9% estimated earnings-per-share growth, the 1.8% current dividend yield, and a 0.9% tailwind from a valuation that should drift higher over time, we see UnitedHealth producing nearly 12% total annual returns in the next five years.

This puts UnitedHealth near the top in terms of large cap total return prospects and we note that the risk to our growth forecast is to the upside more so than the downside. UnitedHealth’s business model is exceptional and we think it has a very long runway of continued growth ahead.

UnitedHealth not only grows earnings well over time, but it is fairly resistant to recessions as well. Its earnings-per-share before, during and after the Great Recession are below:

2007 earnings-per-share of $3.42 2008 earnings-per-share of $2.95 (14% decrease) 2009 earnings-per-share of $3.24 (10% increase) 2010 earnings-per-share of $4.10 (27% increase)UnitedHealth experienced one move down in earnings in 2008, during the height of the Great Recession, but immediately picked back up where it left off in 2009. We see this company’s recession resistance as yet another positive factor in owning the stock.

We expect UnitedHealth to perform well during the next downturn, and that any move down in the share price due to such an event would be an attractive buying opportunity.

Final Thoughts

UnitedHealth has been nothing short of outstanding in terms of earnings growth over the long-term. The company’s ability to continue to grow revenues without undue expense increases has served it well over time, and we see no reason that will cease anytime soon. We therefore continue to forecast robust earnings growth in the years ahead.

This, coupled with UnitedHealth’s strong dividend growth prospects and its reasonable valuation paints a compelling picture of one of the best large cap stocks in the market today. Universal insurance, or some form of it, could certainly be a game-changer for UnitedHealth and others in the field.

However, should something like that come to fruition, it would be many years down the road. Today, it is just a rumor without meaningful legislative backing. We assess the current risk of this to be low.

With double-digit annual total returns projected and strong recession resilience, we rate UnitedHealth as a buy. We like the company’s growth prospects, its valuation, and its dividend growth prospects over the long-term.