Published on July 7th, 2022 by Quinn Mohammed

Berkshire Hathaway (BRK.B) has an equity investment portfolio worth over $360 billion, as of the end of the 2022 first quarter.

Berkshire Hathaway’s portfolio is filled with quality stocks. You can follow Warren Buffett stocks to find picks for your portfolio. That’s because Buffett (and other institutional investors) are required to periodically show their holdings in a 13F Filing.

You can see all Warren Buffett stocks (along with relevant financial metrics like dividend yields and price-to-earnings ratios) by clicking on the link below:

Free Excel Download: Get a free Excel Spreadsheet of all Warren Buffett stocks, complete with metrics that matter – including P/E ratio and dividend yield. Click here to download Buffett’s holdings now.

Note: 13F filing performance is different than fund performance. See how we calculate 13F filing performance here.

As of March 31st, 2022, Buffett’s Berkshire Hathaway owned about 59,000 shares of United Parcel Service (UPS) for a market value of $12.7 million. United Parcel Service represents less than 0.01% of Berkshire Hathaway’s investment portfolio. This marks it as the smallest single public stock position in the portfolio.

This article will analyze the integrated freight and logistics company in greater detail.

Business Overview

United Parcel Service is a logistics and package delivery company that offers services including transportation, distribution, ground freight, ocean freight, insurance, and financing. Its operations are split into three segments: U.S. Domestic Package, International Package, and Supply Chain & Freight.

UPS reported first quarter 2022 results on April 26th, 2022. The company generated revenue of $24.4 billion, a 6.4% increase compared to the same prior year period. The U.S. Domestic segment (which made up 62% of sales) saw an 8.0% gain, while the International and Supply Chain & Freight segments posted gains of 5.8% and 2.0% respectively. Adjusted net income equaled $3.05 per share.

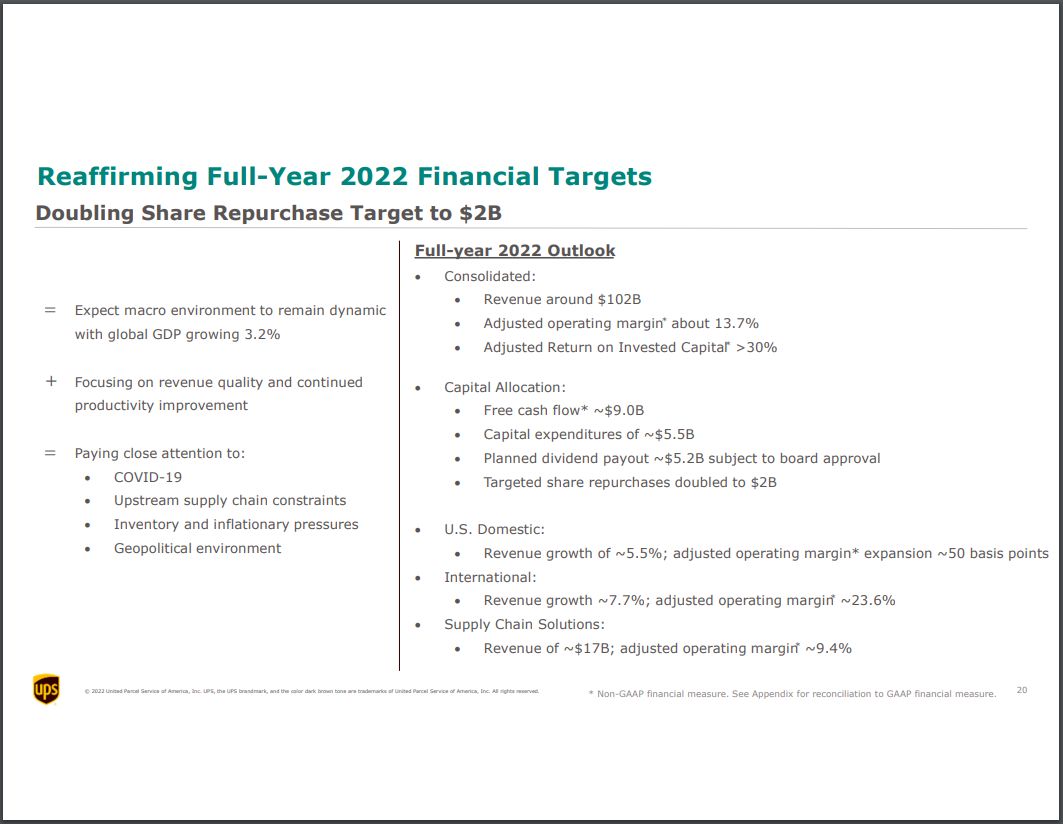

UPS also reaffirmed its 2022 outlook, and expects revenue of around $102 billion, a 13.7% operating margin, $5.5 billion in capital expenditures, and about $5.2 billion in dividend payments. Additionally, UPS announced it expects to double the amount of share repurchases in 2022, to $2 billion in share repurchases.

{kind=link}

Source: Investor Presentation

We estimate that UPS can generate $12.75 in earnings-per-share for the fiscal 2022 year.

Growth Prospects

With the insurmountable rise of ecommerce, comes a major increase in the volume of packages which must be transported, across the country and across the globe.

Additionally, a strong economy will lead to more purchasing of goods, which must be delivered. UPS is very likely to continue benefiting strongly from the rise in ecommerce. It also appears that the COVID pandemic has sped up the trend of online shopping tremendously.

UPS has reduced its shares outstanding by nearly 100 million in the trailing decade. Since 2012, the company has reduced its share count by nearly 1% per year. The company remains active in share repurchases and aims to repurchase $2 billion worth of shares in 2022. This should lead to further bottom line growth on a per share basis.

We project that the company can continue to grow earnings by 5.0% annually through 2027.

Competitive Advantages & Recession Performance

UPS is the largest logistics & package delivery company in the US. It operates in a near duopoly, as its only major competitor to date is FedEx (FDX). And while Amazon (AMZN) is expanding its own logistics business in a big way, it is still a customer of UPS as well.

Despite global economic headwinds, the company’s dominant position in the industry affords it continued growth. Competitive pressures aren’t a major concern for UPS as the entire industry is benefiting from the megatrend of online shopping. Volumes are expected to rise, and so are revenue or pricing per piece.

UPS was impacted significantly during the great financial crisis, but the nature of the COVID pandemic saw the company breeze through the situation. In the face of a prolonged recession with significantly reduced economic activity, UPS would likely suffer.

UPS has raised its dividend for thirteen consecutive years so far. United Parcel Service currently boasts a payout ratio below 50% even after a massive dividend increase earlier in the year, due to strong earnings growth during and after the pandemic. We believe that a dividend cut is unlikely, although not impossible during a steep recession.

Valuation & Expected Returns

Shares of United Parcel Service have traded for a 5- and 10-year average price-to-earnings multiple of 16.0 and 17.4, respectively. Shares are now trading below both of these averages, which indicates that shares could be undervalued at the current 14.6 times earnings. As a result, we believe there is a potential for a valuation tailwind in the intermediate term.

Our fair value estimate for UPS stock is 17.0 times earnings. If this proves correct, the stock will benefit from a 3.1% annualized gain in its returns through 2027.

Shares of UPS currently yield 3.3%, which is above its 5- and 10-year average yields of 3.0% and 2.9% as well. On a dividend yield basis, UPS shares seem to be trading slightly below fair value.

Putting it all together, the combination of valuation changes, EPS growth, and dividends produces total expected returns of 10.9% per year over the next five years. This makes UPS a buy.

Final Thoughts

United Parcel Service is the leader in North American freight and logistics and has had an incredible run-up in its share price in the last five and ten years. The stock has performed roughly in-line with the broader market year-to-date, as the stock price is not overly volatile.

UPS sports a higher-than-average yield of 3.3% today, which may indicate now is an opportune time to add at this level.

Other Dividend Lists

Value investing is a valuable process to combine with dividend investing. The following lists contain many more high-quality dividend stocks:

The Dividend Aristocrats List is comprised of 65 stocks in the S&P 500 Index with 25+ years of consecutive dividend increases. The High Yield Dividend Aristocrats List is comprised of the 20 Dividend Aristocrats with the highest current yields. The Dividend Achievers List is comprised of ~350 stocks with 10+ years of consecutive dividend increases. The Dividend Kings List is even more exclusive than the Dividend Aristocrats. It is comprised of 44 stocks with 50+ years of consecutive dividend increases. The High Yield Dividend Kings List is comprised of the 20 Dividend Kings with the highest current yields. The Blue Chip Stocks List: stocks that qualify as Dividend Achievers, Dividend Aristocrats, and/or Dividend Kings The High Dividend Stocks List: stocks that appeal to investors interested in the highest yields of 5% or more. The Monthly Dividend Stocks List: stocks that pay dividends every month, for 12 dividend payments per year. The Dividend Champions List: stocks that have increased their dividends for 25+ consecutive years.Note: Not all Dividend Champions are Dividend Aristocrats because Dividend Aristocrats have additional requirements like being in The S&P 500. The Dividend Contenders List: 10-24 consecutive years of dividend increases. The Dividend Challengers List: 5-9 consecutive years of dividend increases.