Published on March 30th, 2022 by Aristofanis Papadatos

Exxon Mobil (XOM) went through a perfect storm in 2020 due to the impact of the coronavirus crisis on its business. The oil giant posted its first loss in more than a decade and was expelled from Dow Jones, after 92 years of continuous presence.

However, thanks to the strong recovery of the energy market from the pandemic, Exxon maintained its status as a Dividend Aristocrat and it remains a high-dividend stock with a 4.3% dividend yield.

You can download your free full list of all securities with 5%+ yields (along with important financial metrics such as dividend yield and payout ratio) by clicking on the link below:

In this article, we will analyze the prospects of the oil giant.

Business Overview

Exxon Mobil is the second-largest oil and gas company in the world, behind only Saudi Aramco, with a market capitalization of $361 billion. It produces oil and natural gas at a 60/40 ratio and is one of the most integrated oil majors, with significant contribution from its refining and chemicals segments.

Thanks to its integrated business model, Exxon is more defensive during downturns than most of its peers. When commodity prices are high, the upstream segment thrives. When prices are low, the downstream and chemical segments usually provide a good buffer. As a result, Exxon is more resilient than most oil majors to recessions and downturns of the energy sector, but it rallies less than its peers during boom times.

The defensive nature of Exxon was not evident in the fierce downturn caused by the pandemic in 2020. The unprecedented lockdowns and the severe recession caused by the pandemic formed a perfect storm for the oil giant. Not only did its upstream division suffer from depressed oil prices, but also its refining and chemicals segments suffered from nearly record-low margins due to depressed global demand for oil products and chemicals. Consequently, Exxon incurred its first loss in more than a decade in that year.

However, thanks to the massive distribution of vaccines worldwide and the immense fiscal stimulus packages offered by most governments, global demand for oil has recovered strongly from the pandemic. In the fourth quarter of 2021, Exxon grew its production 2% over the prior year’s quarter and greatly benefited from the sustained rally of the prices of oil and gas. As a result, the oil major grew its adjusted earnings per share from $0.03 in the prior year’s quarter to $2.05, the highest level in more than 5 years.

Even better for Exxon, global oil supply has remained tight this year due to the unwillingness of OPEC to ramp up its production at a faster pace and the recent invasion of Russia in Ukraine, which has limited the outflow of barrels from Russia. As a result, the price of oil has rallied to a nearly 13-year high this year.

In addition, due to the impact of the conflict between Russia and Ukraine on the global supply of refined products, especially diesel, refining margins have skyrocketed lately. As a result, both the upstream and the downstream segments of Exxon currently enjoy the most favorable mix of commodity prices in the last decade.

Of course, the oil industry is infamous for its high cyclicality, which is caused by the dramatic swings of the price of oil. We believe that this time will not prove different, i.e., the price of oil will enter a downtrend at some point in the future.

Nevertheless, the current up-cycle may last more than usual this time, as oil producers are much more reluctant to invest in new growth projects now than they were in the past during boom times. The reason is the secular shift of most countries from fossil fuels to renewable energy sources, which has rendered oil producers much more conservative in their capital expenses than they were in the past.

Growth Prospects

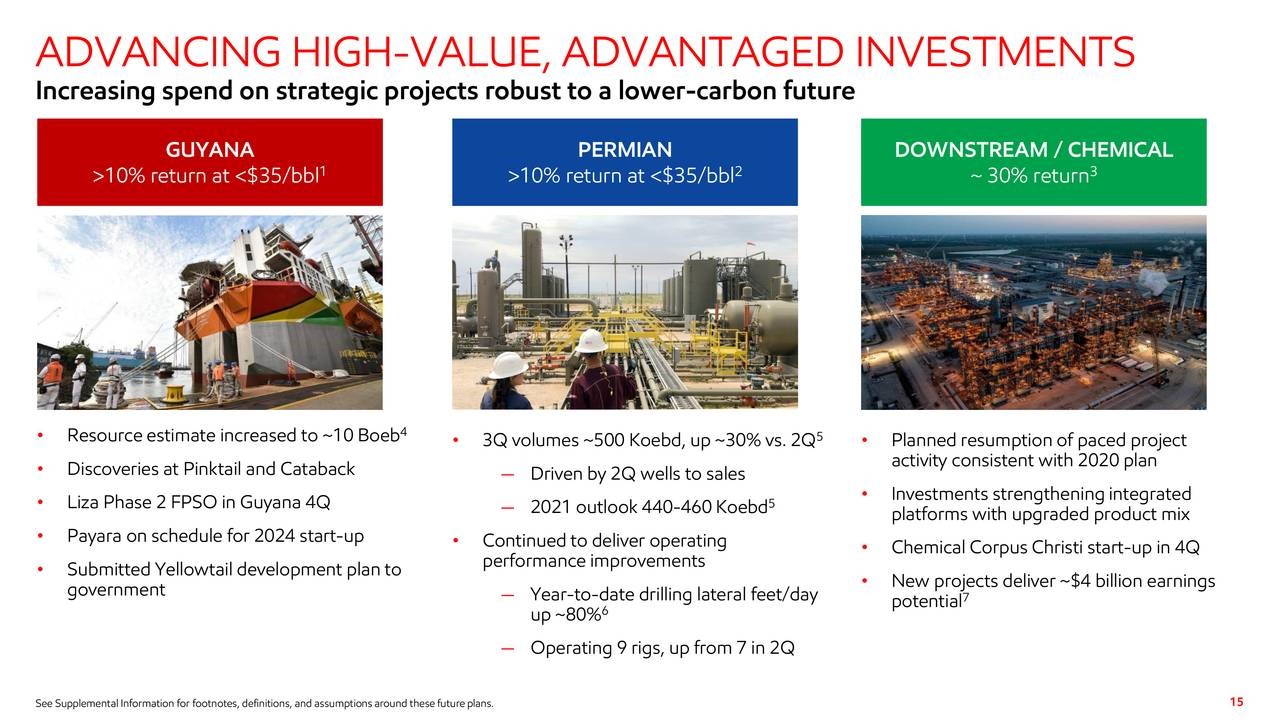

Exxon has two of the most exciting growth projects in the oil industry in its portfolio. The company has approximately 10 billion barrels of oil equivalent in the Permian Basin and expects to reach production of more than 1.0 million barrels per day in the area by 2025. The other major growth project is in Guyana.

Source: Investor Presentation

The oil giant has achieved several discoveries in Guyana and thus it has more than tripled its estimated reserves in the area, from 3.2 billion barrels in 2018 to about 10.0 billion barrels now. Thanks to these growth projects, Exxon expected to grow its production from about 4.0 million barrels per day to 5.0 million barrels per day by 2025.

However, the pandemic led Exxon to revise its strategy. The company decided to curtail some of its growth projects in order to preserve funds and support its generous dividend. As a result, the oil major now expects flat output for many more years. In other words, the production growth expected in Guyana and Permian will be offset by the natural decline of the existing fields of Exxon. It is remarkable that the company has exhibited essentially flat output in the last 15 years, in sharp contrast to its peers, which have grown their output significantly in the last six years.

On the bright side, Exxon has high-graded its asset portfolio at an admirable pace in recent years. Management has stated that 90% of the reserves of the company have a production cost of only $35 per barrel. This means that Exxon has become more profitable than it was in the past at a given price of oil.

Competitive Advantages

The primary competitive advantage of Exxon is its immense scale and its unparalleled expertise in the energy sector. The standard technical procedures followed by most oil companies have been written by Exxon. It is also impressive that other oil companies drilled about 40 dry holes in Guyana whereas Exxon has a nearly 90% success rate in this area. With that said, oil industry is a commodity business and hence all its players are vulnerable to the dramatic cycles of commodity prices.

Dividend Analysis

Exxon is a Dividend Aristocrat, with 39 consecutive years of dividend growth. Due to the high cyclicality of the oil industry, there are only two Dividend Aristocrats in the oil industry, namely Exxon and Chevron (CVX).

Due to the impact of the pandemic on the energy sector, Exxon struggled to defend its dividend in 2020. The oil giant paid the same dividend for 10 consecutive quarters and many analysts were expecting that the company would slash its dividend due to its negative free cash flows back then.

However, the downturn proved short-lived. Exxon maintained its dividend and raised it by 1% in the fourth quarter of 2021. It extended its dividend growth streak to 39 consecutive years and maintained the longest dividend growth streak in the oil industry.

Exxon is currently offering a 4.3% dividend yield. Given the current payout ratio of 50% and the healthy balance sheet of Exxon, its dividend is safe in the absence of a severe downturn.

Management has made it clear that the dividend is its top priority. As mentioned above, the oil major has postponed some growth projects in order to support its generous dividend. In addition, thanks to the high-grading of its reserves, Exxon has stated that its dividend is sustainable even at Brent prices around $41.

Source: Investor Presentation

Even better, management expects to reduce the breakeven price of oil to $35 over the next five years thanks to the continuing high-grading of the asset portfolio and some cost-cutting initiatives. As a result, the dividend of Exxon has a wide margin of safety in the absence of a prolonged downturn in the energy sector.

On the other hand, Exxon is likely to maintain essentially flat production for many more years due to its revised strategy. Consequently, investors should not expect high dividend growth in the upcoming years. Notably the company has raised its dividend at an average annual rate of only 2.8% over the last five years. It is prudent to expect a similar growth rate for the foreseeable future.

Final Thoughts

Exxon is thriving right now thanks to extremely favorable business conditions, including a nearly 13-year high price of oil and nearly all-time high refining margins. Therefore, the 4.3% dividend of the oil giant has a wide margin of safety for the foreseeable future, in the absence of a prolonged downturn. Nevertheless, investors should be aware that the company has lackluster production growth prospects due to its commitment to support its generous dividend. Overall, Exxon is offering a reliable dividend but lackluster growth potential.

{kind=link}

{kind=link}

{kind=link}