Published on August 9th, 2021 by Bob Ciura

Real Estate Investment Trusts, or REITs for short, are a core holding for many income investors due to their high dividend yields. The coronavirus pandemic was devastating for many REITs, but not all struggled in 2020. Agree Realty (ADC) sailed through 2020 with multiple dividend increases, and the company has returned to funds-from-operations growth in 2021.

Agree Realty is also a rarity among REITs in that it pays a monthly dividend. Monthly dividend stocks pay shareholders 12 dividends per year, instead of the more typical quarterly payments.

We created a list of nearly 50 monthly dividend stocks (along with important financial metrics such as dividend yields and payout ratios). You can download the spreadsheet by clicking on the link below:

Agree Realty has a 3.5% dividend yield, which is lower than many other REITs. But extreme high-yielders should generally be avoided because such high-yielding stocks often have unsustainable dividends.

Agree Realty’s dividend yield is well above the S&P 500 average. And it has a high level of dividend safety, along with the potential for high dividend growth in the coming years.

Business Overview

Agree Realty is a retail REIT. As of June 30th, it owned and operated a portfolio of 1,262 properties, located in 46 states covering approximately 26.1 million square feet of gross leasable area. As of the 2021 second quarter, the portfolio was approximately 99.5% leased, and had a weighted-average remaining lease term of approximately 9.7 years. The stock has a market capitalization above $5 billion.

It has a diversified property portfolio, as its top 3 tenants comprise less than 15% of annual base rent. Properties span a number of different industry groups, including grocery stores, home improvement retailers, auto service, and convenience stores.

Source: Investor Presentation

At the same time, Agree Realty has high-graded its portfolio by reducing its exposure to tenant groups most at risk from the current challenges, specifically the coronavirus pandemic. For example, Agree Realty derives just 2% of its annual base rent from health clubs and fitness centers, and just 1% of ABR from movie theaters. In all, Agree Realty generates two-thirds of its ABR from investment-grade tenants.

This portfolio quality is reflected in the company’s strong fundamentals. In an extremely challenging period for many REITs, particularly those operating in the retail industry, Agree Realty continues to post impressive results.

In the most recent quarter, adjusted Funds From Operation increased 41.6% to $57.6 million. FFO-per-share increased 16% to $0.88 for the quarter, compared with the same quarter last year.

In the 2021 first half, core FFO increased 43% to $112 million. Adjusted FFO increased 41% to $110 million, while on a per-share basis adjusted FFO rose 9.2%. Per-share AFFO growth was much lower than overall AFFO growth due to the dilutive impact of share issuances. Still, the company has generated strong growth to begin 2021, even on a per-share basis.

Growth Prospects

Agree Realty grew adjusted funds from operations by an average of just over 6% in the past five years. We estimate they can continue growing AFFO on average at the mid-point, at 5.0% into 2026. We see Agree Realty being able to grow AFFO through their three-pronged growth strategy revolving around acquisitions, development, and partner capital solutions.

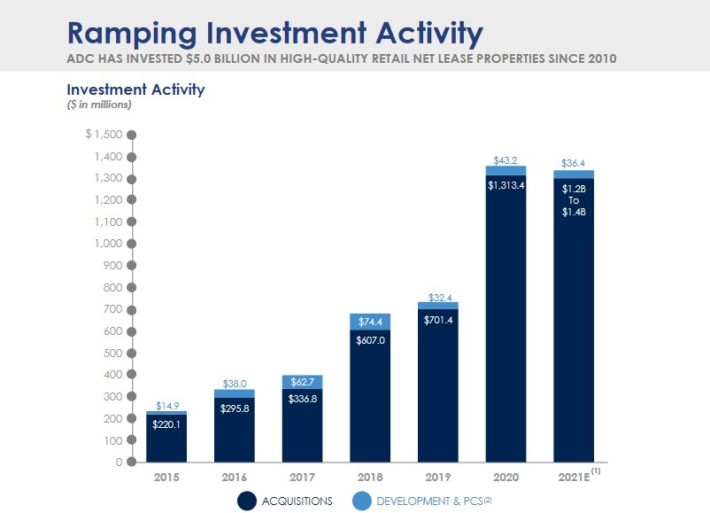

Future growth is likely, as Agree Realty continues to invest in new properties. Agree Realty invested approximately $366 million in 59 retail net lease properties in the second quarter. Looking back further, it has invested $5 billion in properties since 2010.

Source: Investor Presentation

The company recently raised its full-year acquisitions target to $1.2 billion-$1.4 billion. Rent increases will also provide FFO growth.

Agree Realty, like most REITs, is highly reliant on the solvency of its tenants so any headwind or recession within the economy will directly affect it. To combat this, the corporation emphasizes a balanced portfolio with exposure to counter–cyclical sectors and retailers with strong credit profiles.

Additionally, they avoid retailers who rely on private equity sponsors and prefer to partner with leading operators who possess strong balance sheets.

Dividend Analysis

Prior to 2021, Agree Realty had paid a quarterly dividend like the vast majority of dividend stocks. But this year, the company switched to the monthly dividend schedule.

Agree Realty currently pays a monthly dividend of $0.217 per share. On an annual basis, the $2.604 dividend payout represents a 3.5% current yield. Considering the S&P 500 Index currently yields just 1.3%, Agree Realty stock is an attractive option for income investors. And, the company grows its dividend on a regular basis. In the past five years, Agree Realty increased its dividend by approximately 13% per year.

The dividend is also highly secure. Based on expected AFFO of $3.28 in 2021, Agree Realty has a projected dividend payout ratio of 79% for the full year. Agree Realty’s payout ratio has remained extremely consistent in the last decade around the mid–70s, and we see this has very slowly grown to nearly 80%. For a REIT, which must pay out the majority of earnings to shareholders, this is a healthy payout ratio.

The company operates a healthy balance sheet with a net debt-to-EBITDA ratio of 3.6x, which is well below many other REITs. Keeping a manageable level of debt is very important for REITs, to keep the cost of capital down. Its strong balance sheet also features well-laddered maturities, as Agree Realty has just $28 million in maturities through 2024. The company maintains investment-grade credit ratings of Baa2/BBB.

Final Thoughts

Real Estate Investment Trusts are popular for their high dividend yields, but extreme high-yielders should be avoided. Investors should not ignore REITs with somewhat lower yields, as these REITs often have superior fundamentals. Agree Realty is an example of this; although it has a 3.5% yield which trails many other REITs, it makes up for this with high dividend safety and a high dividend growth rate.

Agree Realty is one of the biggest beneficiaries of the reopening of the U.S. economy and the gradual end of the pandemic. As a result, we view it as a solid pick for income investors, particularly those interested in dividend growth.

{kind=link}

{kind=link}

{kind=link}