Updated on April 2nd, 2019 by Josh Arnold

Real estate investment trusts (REITs, for short) give investors a hands-off method to participate in the economic upside of owning and operating real assets.

REITs have grown in popularity over time as yield-starved investors seek alternative strategies to generate portfolio income.

On side effect of the growing popularity of REITs is the emergence of specialized REITs, focusing on only one sub-sector of the real estate industry.

Dream Office REIT (DRETF), (D-UN.TO) is one example of this trend. As the largest pure-play office REIT in the Canadian market, this trust has a dominant position in the office property space.

Note that Dream is listed in Toronto and New York; we’ll use the Toronto listing and Canadian dollars throughout this report, unless otherwise noted.

At the security level, Dream makes a potentially compelling investment proposition for investors seeking high levels of income. There are two reasons for this.

First, the company has a 4% dividend yield. This is about double the average dividend yield in the S&P 500. However, this is down significantly from Dream’s yield in recent years

The second reason why Dream is attractive is that its dividends are paid monthly. Monthly dividends are ideal for retirees and other investors that require stable, predictable income from their investment portfolio. Despite these benefits, monthly payments are rare – there are currently just 41 monthly dividend stocks, which you can access below:

Dream Office REIT’s dividend yield and monthly dividend payments will catch the eye of high income investors.

However, some due diligence reveals that the trust cut its dividend in the summer of 2017, and the payout has been stagnant at a $1.00 annualized payout, down from $1.50.

This article will analyze the investment prospects of Dream Office REIT in detail.

Business Overview

Dream Office REIT is Canada’s largest pure-play office REIT. The trust has a market capitalization of $1.6 billion at current market prices. It is part of the Dream Unlimited family of real estate trusts, which also includes:

- Dream Industrial REIT (DIR.UN.TO)

- Dream Global REIT (DRG.UN.TO)

Dream has a high concentration in office space properties in Toronto specifically, owning more than 7 million square feet downtown and in the greater Toronto area.

This concentration would generally spook investors given that REIT owners typically would seek out a geographically diversified portfolio, but Dream has certainly made it work.

Source: Investor presentation, page 5

Over 60% of Dream’s total portfolio is shown on this fairly small map of Toronto. The trust has found a small area where it likes the fundamentals and has bet big on continued growth.

Toronto has quite favorable fundamentals for office space, which is why Dream continues to concentrate its investments there.

This is a significant change from just a few years ago, when the portfolio was more diversified.

Source: Investor presentation, page 3

Three years ago, Dream had 166 properties and 50% exposure to Toronto. Today, it owns just 34 properties and has 76% exposure to Toronto on a portfolio that is worth just $2.7 billion against its former $7.2 billion.

Dream has taken the bold step of decreasing its geographic diversification, but it has very good reasons for doing so.

Source: Investor presentation, page 6

Toronto has tremendously strong fundamentals for office space, including low – and declining – vacancy rates. This helps drive pricing higher and this is why Dream has bet big on Toronto.

Generally, we don’t like REITs with high geographic concentrations, but Dream has built a very strong portfolio in a terrific market.

Growth Prospects

Dream’s growth prospects depend upon high occupancy rates in Toronto as well as rising rent prices. The trust put in place a strategic plan to capitalize on its new concentration in Toronto and invest for the future.

Source: Investor presentation, page 4

The result has been a substantially smaller portfolio, but one that has a much higher rent base, allowed the trust to deleverage, and afforded it the ability to reduce the trust’s share count.

This has not only improved the balance sheet, but its funds-from-operations per share as well as the share count has dwindled.

Source: Investor presentation, page 7

Looking forward, we see pricing growth as the main catalyst for better earnings for Dream. The trust’s expiring leases in the coming years are on average 23% lower than market rents today in Toronto.

In other words, Dream is locked into prices that are well below market today, but when those rents expire on the schedule shown above, it should be able to achieve much better pricing for the same properties.

That should, in turn, drive earnings higher as Dream should experience some operating leverage from higher base rents.

Source: Investor presentation, page 14

The trust’s tenant list is also quite favorable given that government entities are three of its four largest tenants. The governments of Canada and Ontario, respectively, make up more than 20% of total rent for Dream, with a variety of much smaller tenants comprising the balance.

These tenants are quite stable and should renew leases for the foreseeable future. We don’t see Dream’s very high occupancy rate as at risk at this point given its slate of tenants.

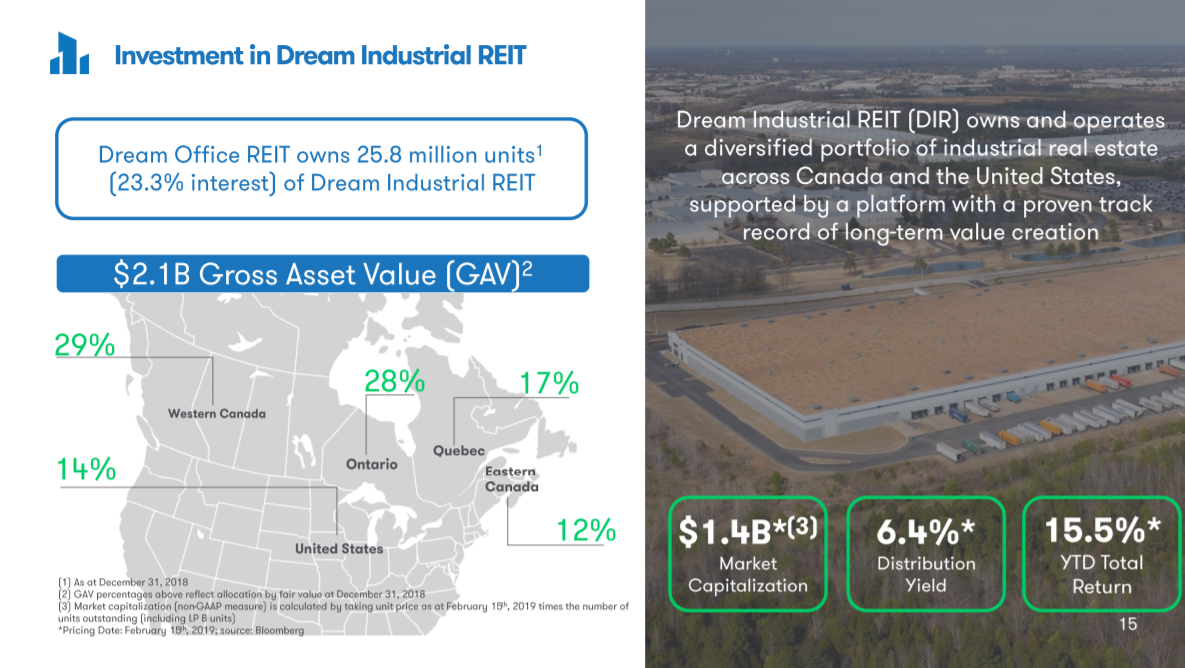

Interestingly, Dream also owns a huge chunk of Dream Industrial REIT.

Source: Investor presentation, page 15

The 23.3% interest the trust has in Dream Industrial is worth about $350 million and pays Dream Office a nearly-6% dividend yield. Dream Industrial has performed well in recent years, driving passive performance for Dream Office.

In short, while we don’t see Dream as producing huge growth numbers in the coming years, it is undoubtedly well positioned to continue to grow organically from higher base rents. Toronto’s office space fundamentals are more than sufficient to support this growth.

Dividend Analysis

In 2018, Dream produced $1.66 in FFO-per-share, which was down significantly from 2017’s $2.03. However, the distribution is just $1.00 per share, meaning coverage is quite good.

As mentioned, Dream cut its distribution nearly two years ago and the payout has been stagnant since then. We certainly don’t see the risk of a further cut today given the low payout ratio and favorable fundamentals, but the fact that the dividend was cut relatively recently means growth may be further out.

In addition, with FFO-per-share declining in 2018, management will likely be keen to keep the payout as it is until earnings begin to move higher.

The 4% dividend yield is much lower than the 7%+ yields Dream produced in the past, but it is still high enough to entice income investors. This is particularly true with the fact that Dream pays shareholders monthly instead of quarterly.

Final Thoughts

Dream Office REIT’s dividend yield and monthly dividend payments make it appealing to income investors. Its fundamental outlook is also quite favorable, and we see moderate levels of growth in the coming years.

The 2017 dividend cut looms large for investors as the yield is much lower than it once was for Dream, but the current payout is well covered and we view it as safe.

We think Dream is a fine pick for those seeking exposure to REITs, but note there are trust’s with much higher yields available for pure income investors.

{kind=link}

{kind=link}

{kind=link}