Updated on March 6th, 2019 by Josh Arnold

AGNC Investment Corp (AGNC) has a sky-high dividend yield of 12.3%, which is something this stock is certainly known for. In terms of dividend yield, AGNC is near the top of our list of high-yield dividend stocks.

It is one of a select few stocks with a 10%+ dividend yield. In addition, AGNC pays its dividend each month, rather than on a quarterly or semi-annual basis.

Monthly dividends give investors the ability to compound dividends even faster. There are not many monthly dividend stocks. We’ve compiled a list of these 41 stocks, which you can access below:

That said, it is also important for investors to assess the sustainability of such a high dividend yield. This article will discuss AGNC’s business model, and whether the stock is appealing to income investors.

Business Overview

AGNC was founded in 2008. It is an internally-managed REIT. Whereas most REITs own physical properties that are leased to tenants, AGNC has a different business model. It operates in a niche of the REIT market: mortgage securities.

AGNC invests in agency mortgage-backed securities. It generates income by collecting interest on its invested assets, minus borrowing costs. It also records gains or losses from its investments and hedging practices.

The trust employs significant amounts of leverage to invest in these securities in order to boost its ability to generate interest income. AGNC borrows primarily on a collateralized basis through securities structured as repurchase agreements.

The trust’s stated goal is to build value via a combination of monthly dividends and net asset value accretion. AGNC has done well with its dividends over time, but net asset value creation has sometimes proven elusive.

Indeed, the trust has paid nearly $40 of total dividends per share since its IPO; the share price today is under $18. Net asset value, however, fell 16% in 2018 from $19.69 to $16.56.

Source: Q4 Investor Presentation, page 6

AGNC’s 2018 was a tough period, as it was for the mortgage REIT industry as a whole. Rising interest rates are highly inversely correlated to a mortgage REIT’s ability to generate higher spreads on its portfolio, so in general, earnings capacity falls.

Indeed, in 2018, AGNC posted a loss of $1.14 per share in comprehensive income. Its net spread and dollar roll income per share was $2.35, and it was able to declare $2.16 per share in total dividends. AGNC cut its monthly dividend from $0.20 per share to $0.18 per share in August of 2016, and it has remained there since.

The trust’s economic return, which is the sum of dividends and change in tangible book value, was -4.9% in 2018, driven by significantly lower tangible book value.

The trust also continued its long tradition of raising funds via preferred and common equity offerings in order to fund portfolio growth, pay the dividend, and for corporate uses.

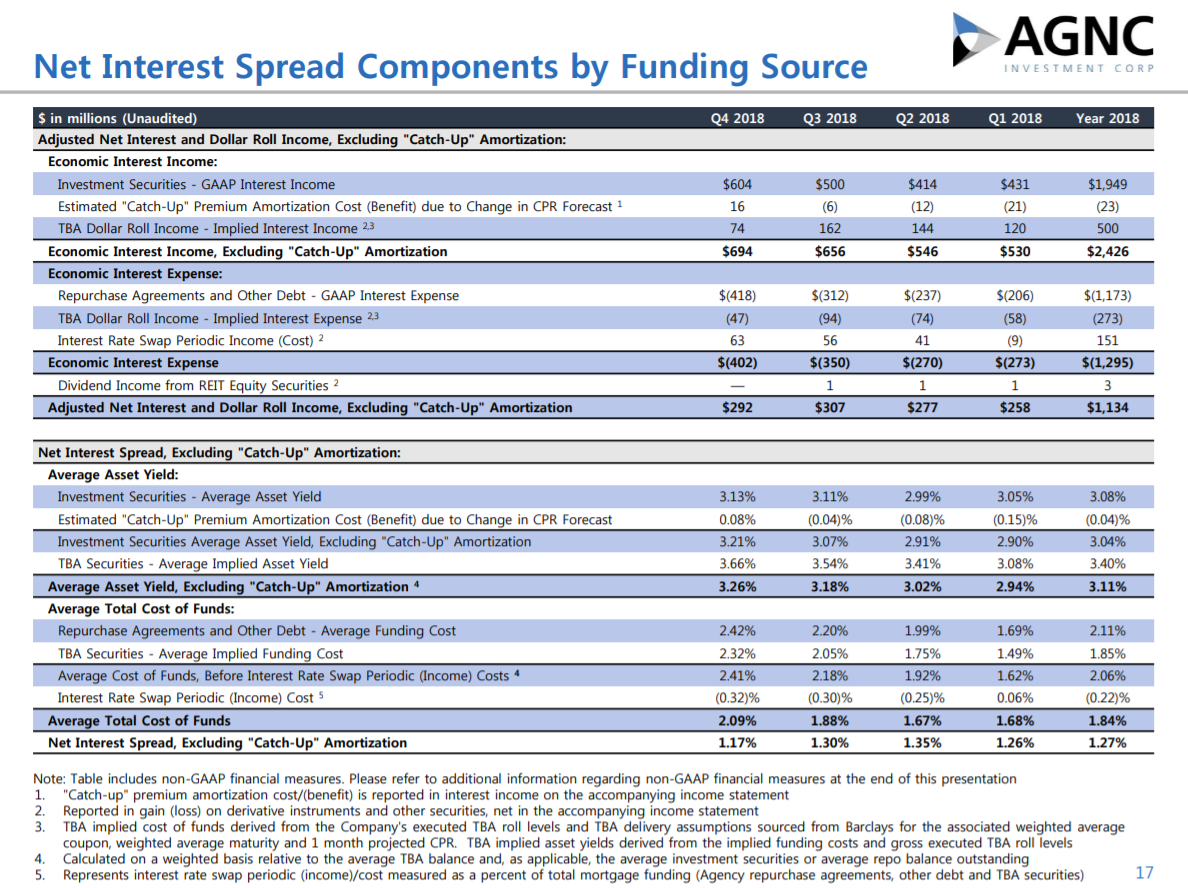

Source: Q4 Investor Presentation, page 17

AGNC’s net interest spread, which is the manor in which it generates revenue, fell during 2018 from 1.27% to 1.17%. This was due to a 25bps rise in its cost of funds, from 1.84% to 2.09%.

That increase was partially offset by a 15bps gain in average asset yield, but it wasn’t enough and AGNC’s profitability suffered for it.

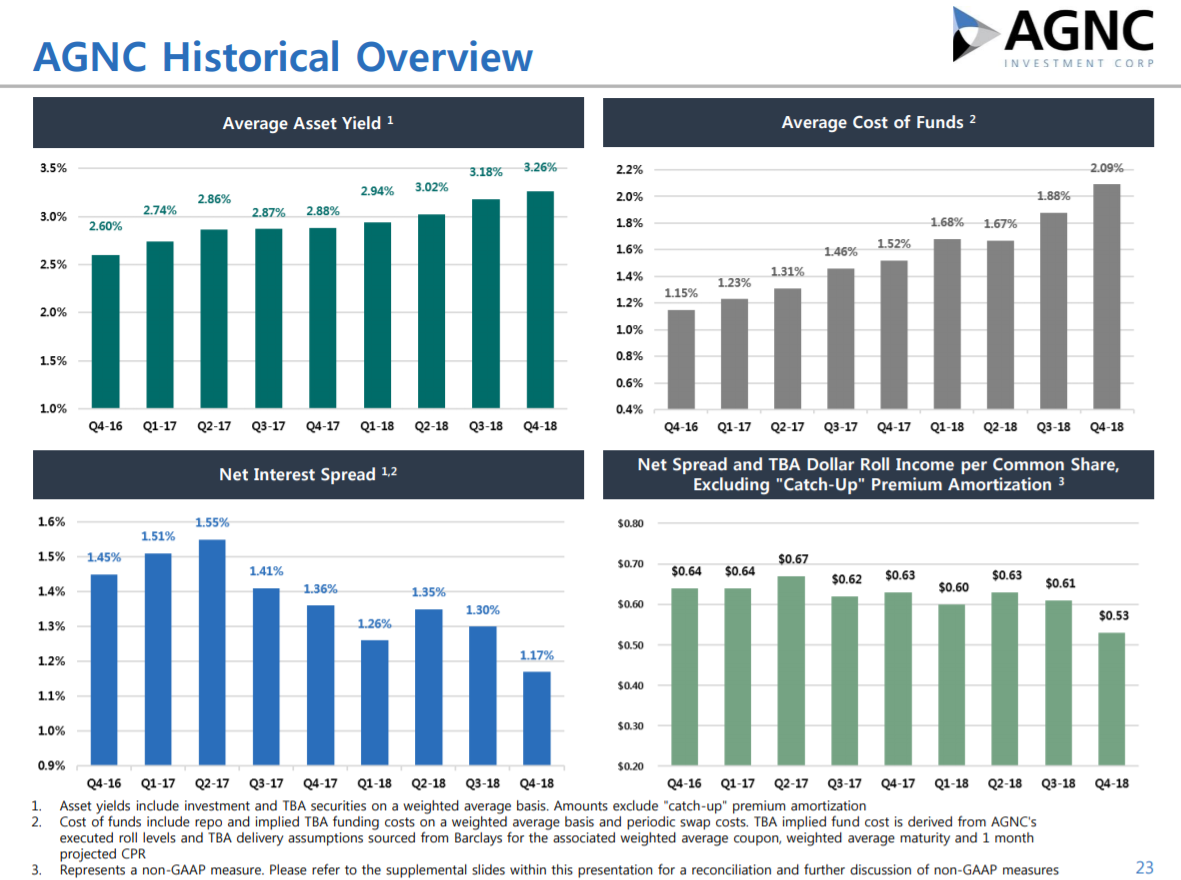

Source: Q4 Investor Presentation, page 23

This slide shows that declining spreads aren’t a new problem for AGNC, as rising interest rates have taken their toll on the trust’s ability to generate income, as well as its book value, for several quarters.

So long as AGNC’s cost of funds is rising at rates in excess of its asset yields, it will continue to have a difficult time growing earnings.

As interest rates continue to normalize around the world, mortgage REITs like AGNC will likely continue to face headwinds to interest spreads and book value.

Growth Prospects

The major drawback to mortgage REITs is that the business model is negatively impacted by rising interest rates.

AGNC makes money by borrowing at short-term rates, lending at long-term rates, and pocketing the difference. To amplify returns, mortgage REITs are also highly leveraged.

In a rising interest rate environment, mortgage REITs typically see the value of their investments reduced. And, higher rates usually cause their interest margins to contract. This double-impact is what investors experienced in 2018 as spreads contracted and book value fell.

This has negatively impacted AGNC over the past year. To offset this, AGNC has employed hedges to mitigate this interest rate risk.

The trust has 94% of its portfolio hedged as of the end of 2018, which is quite high compared to historical norms. The trust recognizes that interest rates likely aren’t done rising, and it has therefore attempted to hedge against that upside risk, which is a negative for its portfolio value.

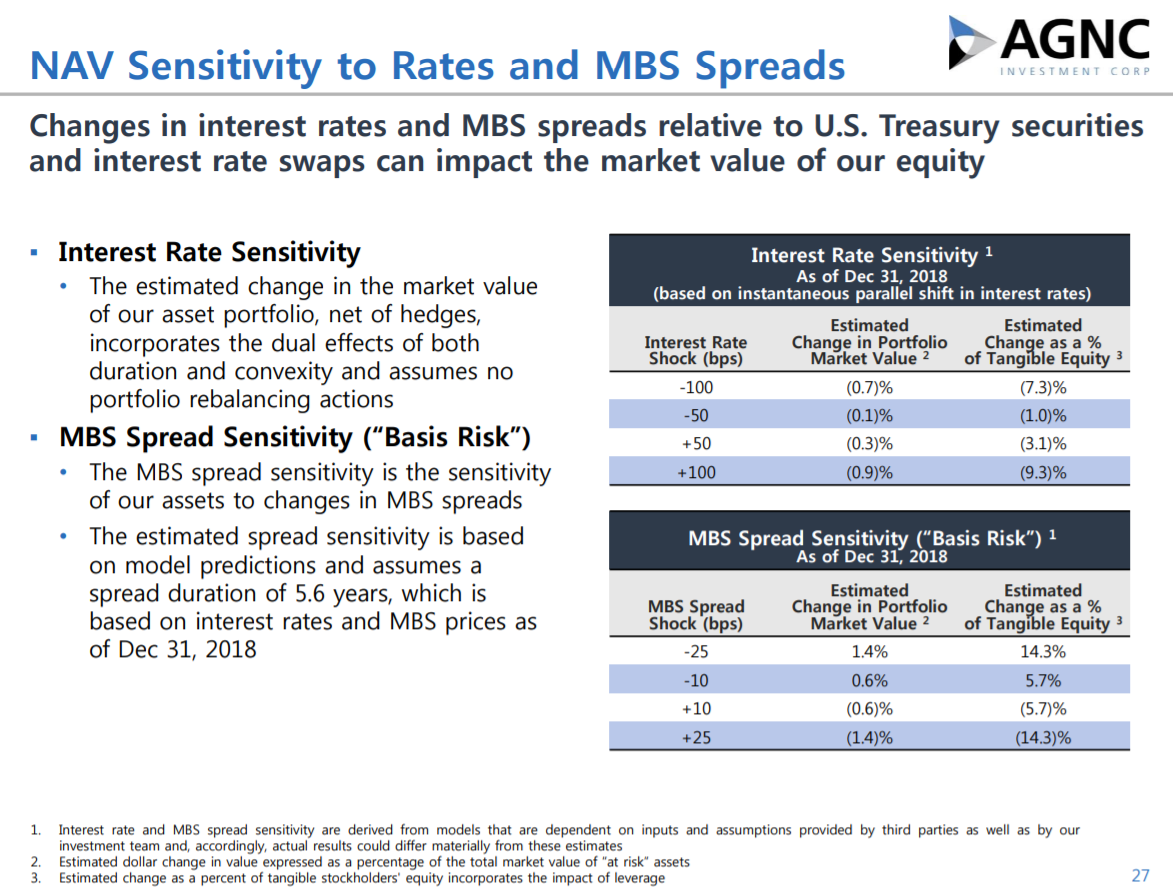

AGNC is highly sensitive to fluctuations in interest rates. For every 100-basis point increase in interest rates, AGNC will see a 1.6% change in portfolio market value.

Source: Q4 Investor Presentation, page 27

A parallel 100bps shift upwards in interest rates would cause a 90bps decline in the value of the portfolio but thanks to high leverage, tangible book value would fall more than 9%. More specifically, if mortgage-backed securities spreads rose just 25bps, AGNC’s tangible book value would fall more than 14%.

This speaks to the tremendous leverage the trust has and its reliance upon a favorable rate environment to reach its stated goal of higher net asset value.

AGNC has paid a monthly dividend of $0.18 since 2016 despite these challenges, and it doesn’t appear the dividend is at risk today. The trust has been willing to do whatever it takes to continue paying it, and there is no reason to believe that practice will cease.

That said, dividend increases are likely a long way away. Therefore, AGNC should be thought of more as a high-risk income stock than a dividend growth stock.

Dividend Analysis

AGNC declared a monthly dividend of $0.18 per share for February, as it has since the summer of 2016. On an annualized basis, its dividend payout remains $2.16. This means AGNC has a 12.3% dividend yield with the share price at $17.61.

A double-digit dividend yield is often a sign of elevated risk. And, AGNC’s dividend does carry significant risk. AGNC has reduced its dividend several times over the past decade.

However, as the dividend has been the same since August of 2016, it would appear the trust has found a level it is comfortable with, assuming no interest rate spread shocks befall it.

We do not see a dividend cut as an imminent risk at this point given that the payout has been stable for more than two years and that AGNC’s net asset value appears to be stabilizing. Management has taken the necessary steps to protect its interest income, so we don’t see a dividend cut in the near term.

However, with any mortgage REIT, there is always significant risk to the payout, and that is something investors should keep in mind.

Final Thoughts

Mortgage REITs have had a tough time since the world’s central banks began tightening monetary policy several years ago. However, AGNC has managed to pay a hefty dividend throughout that period, offsetting a weak performance in net asset value and the share price.

The yield is in excess of 12%, which is very high, even for AGNC and mortgage REITs in general. We believe the yield to be safe for the foreseeable future, but this is hardly a low-risk situation.

While AGNC should continue to pay a dividend yield many times higher than the S&P 500 average, it is not an attractive option for risk-averse income investors.

{kind=link}

{kind=link}

{kind=link}