The Driftwood 22 Disclosure Project

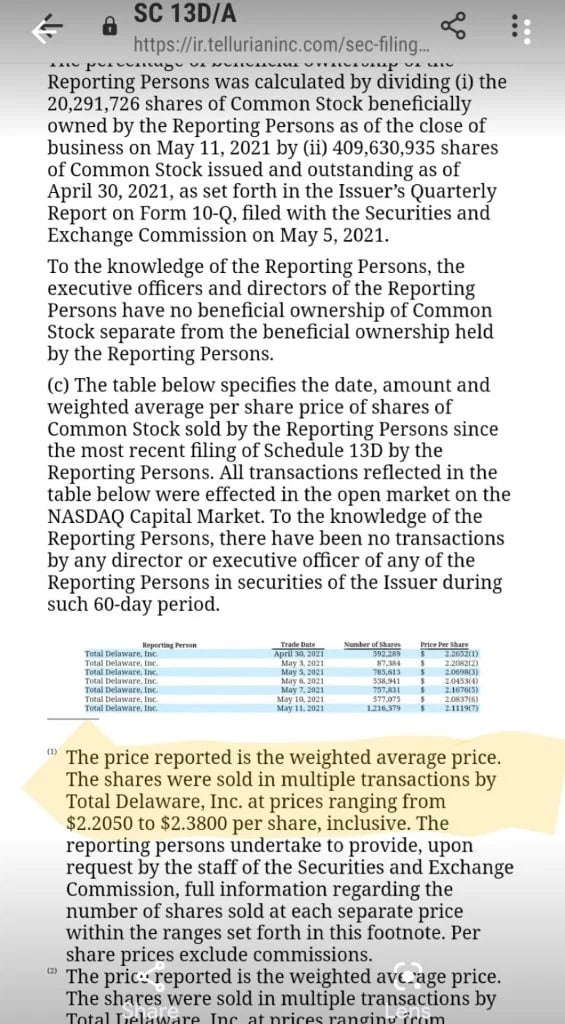

Total S.A (NYSE:TOT) had invested $550M in the Driftwood Tellurian’s sponsored project. Now they are writting it off. What’s now making them believe it was a big mistake, staff who quit and have their version of the story.

Q1 2021 hedge fund letters, conferences and more

WHILE TOTAL IS WRITING OFF TELLURIAN -80%, THE COMPANY TARGETS THE “BOBS OF SEEKINGALPHA” WITH AN OUTSTANDING $14 FUTURE FREE CASH FLOWS PER SHARE.

The Feasibility Of The Driftwood LNG

Tellurian Inc (NASDAQ:TELL) premium reminds us UNG… Investors pill on these things without understanding the risk beneath them.

Haven’t you read the article in the Financial Times – the house in Colorado up for sale. It seems that the sponsor took a margin trade on the project as collateral or Systemic Selling Risk Management Program ?!

Mr. Souki pitches ideas, wraps them up around numbers, raises money then we didn’t hear for 3 years. Then his trade idea and project totally collapsed, commercials and backers exit the deal, Mr. Souki doesn’t seem agitated and it’s fine. He activated himself last summer when the company coincidentally raised $35m “to study the feasibility of the Driftwood LNG”. But then he is on mute for most of 2020H2. However when the company found itself with less than 3 months of cash on hand, he popped up again 5-7 straight weeks during Spring 2021. In his videos, he gives his temperature reading of the LNG market and everything has to be pointing out that they are building driftwood except that they aren’t.

“Even before the Covid, the project had problems. Aside from Tellurian IR, everyone we’ve talked thinks the project is a blunder. Even long before the virus, Driftwood chances of moving forward seemed quite improbable”. -Senior Natural Gas Editor, Houston Texas

Tellurian's Staff Issues

Total’s cash injection into Tellurian made the people believe in the project. Tellurian poached employees with 2X–3X base salary, the staff left Cheniere Marketing in droves to join Tellurian ship. Can Tellurian at point replicate Cheniere, even the more reluctant ones thought it was their best odds. Millions were spent giving everyone the impression that Charif El Souki had the moxy, money showers, and that’s truly the genius of one man.

But the people he hired then realized they came to fix the mistakes. (who does not) In their early weeks at Tellurian they all seized up some of the situation and months after some started to regret the move. Inside nephews or boss connections are hired for unknown or obscure functions creating a malaise… Wife of an executive gets a contract, same for the princeling. Something ain’t right.

The ship has too many sinking holes while they’ve been achieving real things at Chevron/Conoco they can’t objectively say the same about Tellurian. Someone ain’t right with how the contracts and the Driftwood FID (Final investment decision) were conducted, and now they are being told “they are the problem“.

In this situation people with honor do quit. They realized it’s not worth it.

A combination of Somebody/Something is the problem. Let’s explore more of it.

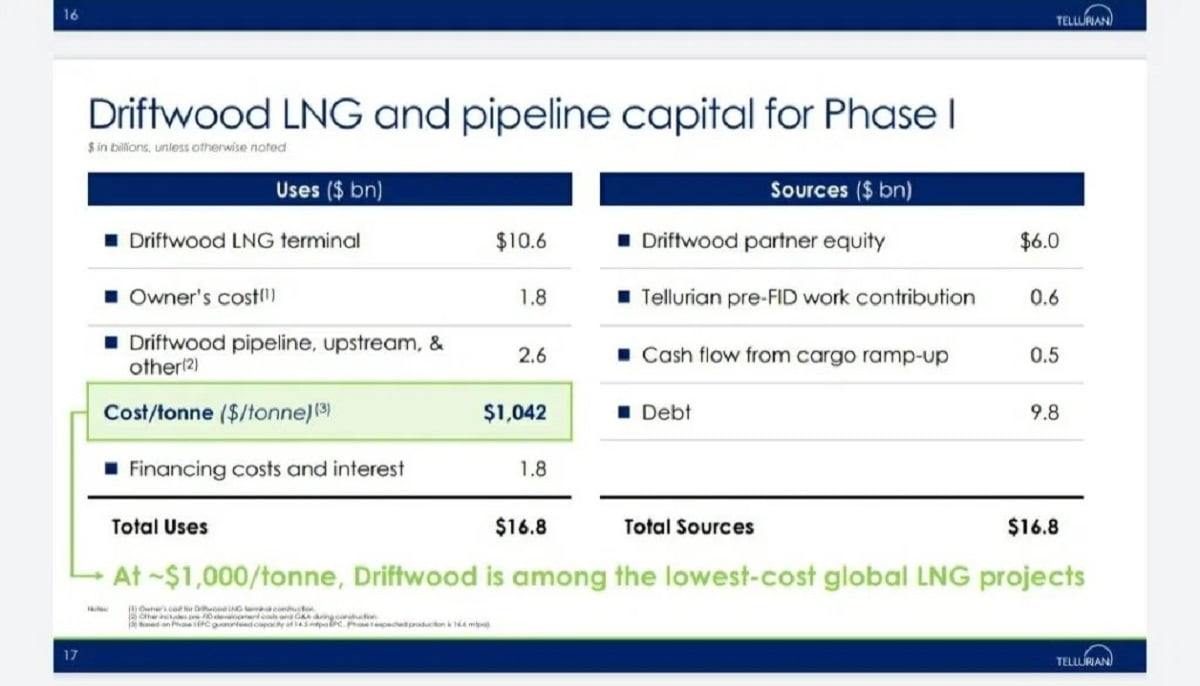

First their FID (2016) was always surfacey from the early beginnings. Tellurian is never, NEVER at $1040/MTPA. Didn’t the metal price construction costs rise since 2016′ ? Everyone should look into the Driftwood 2016 FID for what they budget at what cost. Steel was around $1.45/kg in 2016 and now it’s around $2.5-3.0/kg (> 50%). In a recent presentation update Tellurian thinks the FID cost is up 3% in 2021. If we find discrepancies like this, it means their inputs that they use to sell their project are not good.

For example the $3.50/mmbtu they choose for the investor presentations doesn’t adequately represent their total full cost. The balance of plant cost is 1.5X of Main Plant Cost. BOP includes gas pipeline cost also but their equity model compels to invest on overall project TIC.

Tellurian inc. keeps floating a promising $5.50 del. Asia while Goldman puts them at $8.5-9 total cost per mmbtu in 2019 …

Tellurian May 2021 Presentation, Investor Relations Department

- Numbers, Est. pitched in the company presentations are expressly kept vague. They work only on the non-commercial people world aka ‘investors’ and just raise more questions than answers from the commercials about Tellurian.

Convincing a big company to give $550M, $8.50 a share, no revenues, no nothing is a hat trick The downside risk is commensurate not only by the high expectations placed by Total but also Tellurian is now facing huge scrutiny in the industry.

Total determined that there was no arbitrage (Henry Hub /Asia) after the full capex/variable costs in 2023-2025 the french-giant decided to divest as an equity holder, we also opine that they also didn’t like Driftwood LNG sponsor’s direction or lack thereof.

After they’ve seen the money that they’ve invested and witnessed what came out of it after they decided that they were still better to get some chips back from the House rather than double, triple losing by bailing-out Tellurian out of trouble down the road. It’s a clear signal for the investors. In our next disclosure releases you’ll get a clearer picture.

- The Driftwood 22 DISCLOSURE Project

The post The Driftwood 22 Disclosure Project appeared first on ValueWalk.

Source valuewalk

{kind=link}

{kind=link}

{kind=link}