The company makes money by raising capital through issuing debt as well as preferred and common equity and then reinvesting the proceeds into higher yielding debt instruments.

The spread (i.e., the delta between the cost of capital and the return on capital) is then largely returned to common shareholders via dividend payments, though the company does often retain a little bit of the profits to reinvest in the business.

For example, last year the company generated cash flows per share of $2.59 but only paid out $2.28 per share in dividends.

In the first quarter management was quite active in capital markets, raising approximately $322 million in the first three months of the year. In the process, the company issued approximately 16.1 million common shares at approximately $20 per share and thereby improved the company’s economies of scale by reducing administrative expense per share by over 20% on a pro forma basis for about $0.05 per quarter running.

Not only did the equity raise improve cost efficiencies, but it also gave the trust the opportunity to capitalize on some of the cheapest mortgage valuations since early 2016 thanks to a significantly more dovish Federal Reserve and oversold risk indicators. The capital raise was also done at a price fairly close to book value and considerably higher than today’s share price.

Growth Prospects

Recent results at ARMOUR have been mostly positive. In the first quarter they reported a total economic return of 4.8% during the quarter and an annualized 13.2% return based on stockholders’ equity at the beginning of the quarter.

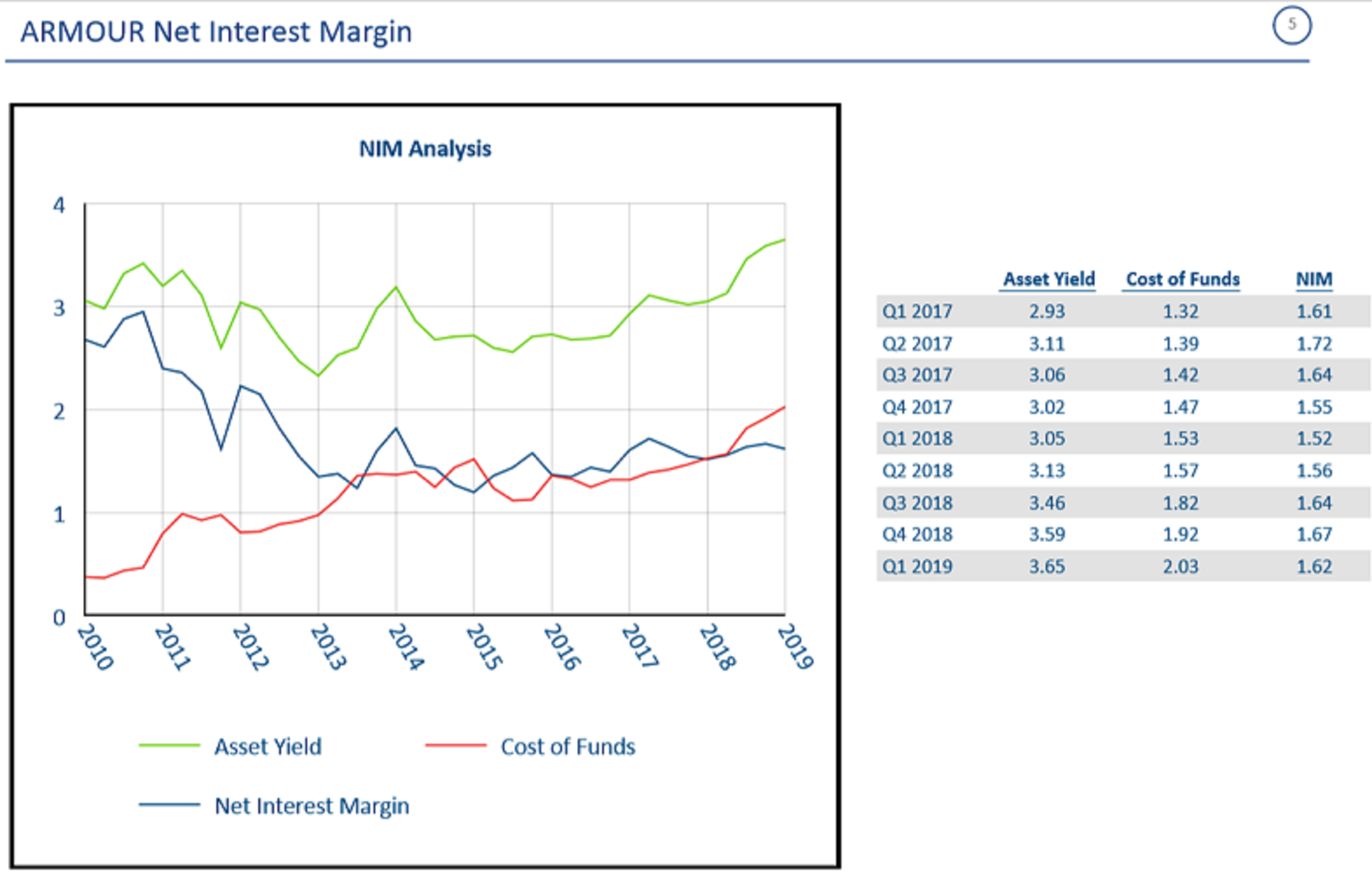

Additionally, core income continued its streak of exceeding dividend payments for the eleventh consecutive quarter. With an average yield on assets of 3.7%, a 3.9% annualized average principal repayment rate, and a 1.6% average net interest margin, the business overall looks healthy.

Looking ahead, the declining short term interest rates could help the business profit margins as they can now borrow funds at cheaper rates and use the proceeds to repurchase preferred and common equity shares at a discount to the prices they were issued at.

We also see in the chart below that – until the recent reversals in interest rates – the cost of funds was increasing much faster than the average asset yield. A decline in borrowing rates will be welcomed by mortgage REITs like ARMOUR.

Source: Investor presentation, page 5

Another positive trend is that, despite the large decline in mortgage rates and the pickup in REIT finance activity from historical lows, the MBA financing index remains muted. In fact, it remains well below average levels in the ultra-low interest rate period of 2010 to 2016.

This means that ARMOUR’s higher yielding assets are not being repaid as quickly as the declining interest rates would otherwise indicate, preserving and even enhancing their profit margins in the short term.

The trust also has a significant proportion of prepayment protected securities that will help it from experiencing any significant hits to profitability from prepayments, should they pick up as expected in the coming months.

Risk Considerations

While there have certainly been some positive developments at work for ARMOUR, there are still several risks to be concerned about.

First, and foremost, declining interest rates and rising prepayments – though hedged to some degree by management – will pose a significant headwind to earnings growth, especially if interest rates continue to fall.

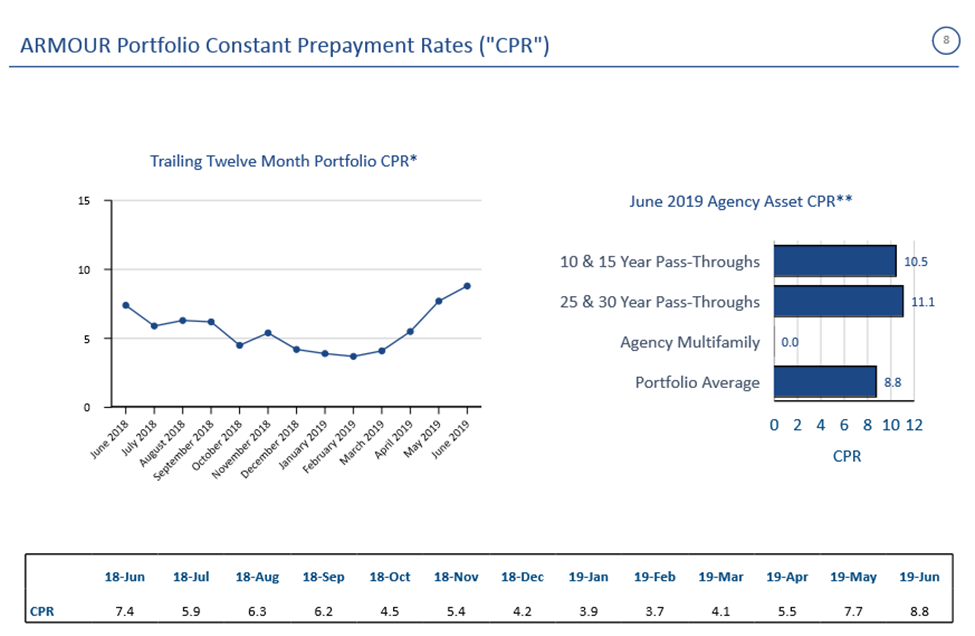

Already this year with interest rates falling, portfolio constant prepayment rates have been on the rise, particularly in the second quarter:

Source: Investor presentation, page 8

This trend has caused management to recently announce an 11% dividend reduction a few weeks ago on June 24th.

Additionally, if the economy were to go into recession, mortgage defaults could surge, leading to steep losses. With the uncertain macroeconomic outlook and declining foreign investment in American real estate, this risk is increasingly relevant.

Final Thoughts

ARMOUR Residential’s high dividend yield and monthly dividend payments make it stand out to high yield dividend investors. However, we remain cautious on the stock.

While the company is covering its dividend currently, the declining interest rates will continue to force the company ever further out on the risk spectrum to maintain its cash flows as its older mortgages roll off the balance sheet. This sets them up for potentially steep losses if the economy slips into recession and defaults rise.

Clearly management views this as a clear and present risk and have cut their dividend as a result. This makes the investment highly speculative right now, especially for income investors. As a result, we encourage investors to look elsewhere for sustainable and growing income.

{kind=link}

{kind=link}

{kind=link}